Savings

Moving Back Home After Uni: How I Save £1,000 a Month

Table of Contents

- The Boomerang Generation: Why So Many Graduates Are Moving Back Home

- The Core Financial Logic: Why Rent vs. Bills-Only Makes Such a Dramatic Difference

- What Separates a Productive Arrangement From a Directionless One

- 1. Agreeing a Clear, Fair Bills Contribution From Day One

- 2. Treating the Savings Contribution as Non-Negotiable

- 3. Having a Specific Financial Goal, Not Just 'Saving in General'

- 4. Setting an Honest Time Horizon With Parents

- Building Your Own Savings Plan While Living at Home

- Beyond the Numbers: The Emotional Reality of Moving Back Home

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Two years after leaving for university with the standard mixture of excitement and independence every fresher feels, one 25-year-old marketing coordinator found herself moving straight back into her childhood bedroom. It wasn't the plan. But what started as a temporary, slightly deflating arrangement has quietly become one of the smartest financial decisions of her working life so far.

"It would have been impossible to save anything close to that had I lived by myself, given the cost of living right now," she says. "I pay towards the bills, but I don't pay rent — and that one difference means I can put aside £1,000 a month into savings."

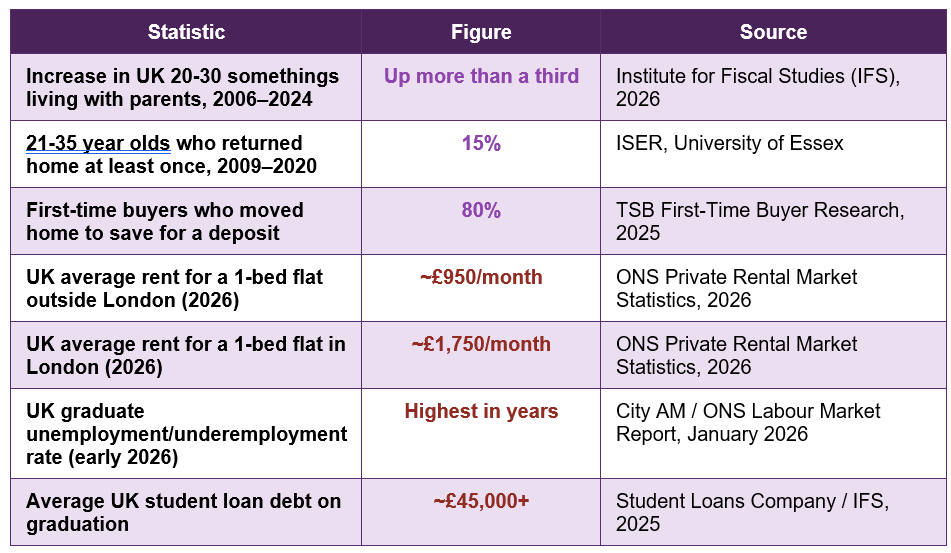

Her story is not unusual. It is, in fact, increasingly the norm. Across the UK, the proportion of young adults in their twenties and thirties living with their parents has risen by more than a third since 2006, according to the Institute for Fiscal Studies, with rents, graduate underemployment, and student debt all combining to make independent living a genuinely difficult financial proposition for a growing share of the so-called 'boomerang generation.' This article unpacks exactly how the maths behind moving back home works, what makes the difference between a financially productive arrangement and a directionless one, and how to structure your own version of this setup if you're considering it, or already living it.

The Boomerang Generation: Why So Many Graduates Are Moving Back Home

This is not a story about a lack of ambition or independence among young adults — it is a story about arithmetic. The table below sets out the current UK data behind the trend:

First-time buyers who moved home to save a deposit: 80% — TSB's 2025 research found four in five hopeful first-time buyers had moved back in with parents specifically to accelerate their house deposit savings — making this arrangement less an exception and more the emerging default route onto the property ladder

- This isn't just a UK pattern. Research from the University of Essex's Institute for Social and Economic Research found 15% of 21-35 year olds returned to their parental home at least once between 2009 and 2020, and similar patterns are well documented in the US and across much of Western Europe, driven by remarkably similar combinations of rising rents, stagnant graduate wages, and growing student debt burdens.

The Core Financial Logic: Why Rent vs. Bills-Only Makes Such a Dramatic Difference

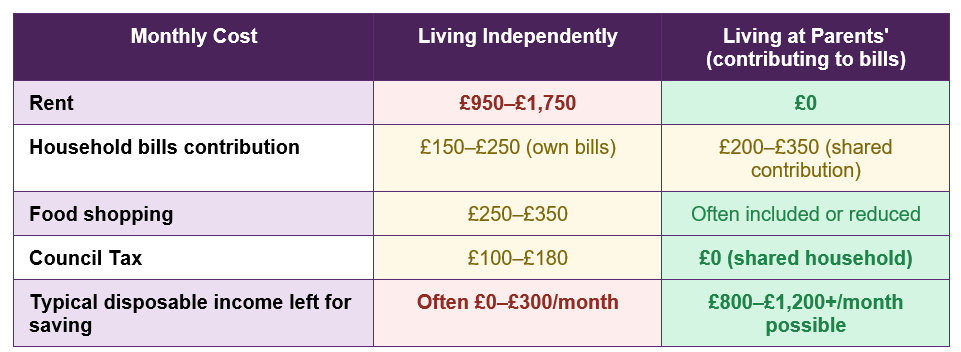

The detail that makes the marketing coordinator's situation work so effectively is a specific and important distinction: she contributes toward household bills, but she does not pay rent. This is not a minor technicality — it is the single factor that transforms a modest, manageable contribution into a genuinely transformative monthly savings rate.Rent in the UK's private rental market typically represents the single largest line item in any independent renter's monthly budget, frequently consuming 35-50% of take-home pay for graduates in their twenties, particularly in and around major cities. Contributing toward household bills — energy, broadband, council tax, groceries — while living at a family home removes this single largest cost entirely, while still meaningfully sharing the financial load of the household rather than living there for free.

The comparison illustrates why the gap is so large: it isn't simply that living at home is 'cheaper' in a vague sense — it is that one specific, dominant cost (rent) disappears almost entirely, while a much smaller, shared cost (a bills contribution) replaces it. The difference between those two numbers is, in effect, the £1,000 a month the marketing coordinator is able to save.

What Separates a Productive Arrangement From a Directionless One

Moving back home is not, by itself, a financial strategy — it is an opportunity that can be used well or squandered. The difference between graduates who use this period to build genuine financial momentum and those who simply drift through it tends to come down to a small number of deliberate choices.1. Agreeing a Clear, Fair Bills Contribution From Day One

The most financially successful arrangements tend to involve an explicit, agreed monthly contribution toward household costs — not an indefinite, undefined 'help out when you can' understanding. A specific number, discussed openly with parents and reviewed periodically as income changes, removes ambiguity and avoids the awkwardness of either under-contributing or over-contributing without realising it.2. Treating the Savings Contribution as Non-Negotiable

The single biggest risk of a low-cost living arrangement is that the money simply gets absorbed into everyday discretionary spending rather than genuinely saved. Setting up an automatic transfer of a fixed savings amount on payday — before any discretionary spending happens — is what converts the theoretical advantage of living at home into an actual, growing balance.3. Having a Specific Financial Goal, Not Just 'Saving in General'

Graduates who treat this period as working toward a specific target — a house deposit, a fixed savings milestone, a planned date for moving into independent living — tend to maintain motivation and discipline far more consistently than those saving without a defined endpoint. A vague intention to 'save some money' is far easier to abandon than a concrete goal with a number and, ideally, a rough timeline attached.4. Setting an Honest Time Horizon With Parents

Open conversations about how long the arrangement is expected to last — whether that's six months, two years, or until a specific savings target is hit — tend to produce healthier outcomes for both generations than an open-ended, undiscussed arrangement. This is as much about family dynamics as finances, but the two are closely linked: financial clarity tends to reduce tension on both sides.Building Your Own Savings Plan While Living at Home

If you are in this situation, or considering it, the following framework can help convert the financial advantage of living at home into genuine, structured progress:- Calculate your real disposable income honestly: Take your take-home pay, subtract your agreed bills contribution, subtract any debt repayments (including student loan deductions, which happen automatically for most UK graduates above the repayment threshold), and subtract a reasonable discretionary spending allowance. What remains is your genuine savings capacity — be honest about this number rather than optimistic.

- Automate your savings transfer on payday: Set up a standing order that moves your target savings amount to a separate account the day you are paid, before you have the chance to spend it. This single structural change is consistently the most effective habit for converting intention into an actual growing balance.

- Choose the right account for your goal and timeline: If you are saving toward a first home and you are aged 18-39, a Lifetime ISA offers a 25% government bonus on contributions up to £4,000 a year — a meaningful boost specifically designed for situations like this. If your goal is shorter-term or more general, a competitive easy-access or fixed-term savings account may suit better.

- Track your progress visibly: Whether through a simple spreadsheet, a savings app, or a basic notes file, seeing your balance grow month by month reinforces the habit and provides motivation during the periods when living at home feels socially or emotionally harder than the financial upside makes up for.

- Review and adjust your contribution as your income changes: If you receive a pay rise, a bonus, or take on freelance work, revisit both your household contribution (to keep it fair) and your savings rate (to make the most of increased capacity), rather than letting additional income simply disappear into lifestyle creep.

Beyond the Numbers: The Emotional Reality of Moving Back Home

It would be incomplete to discuss this trend purely in financial terms, since the emotional and social dimension is real and frequently raised by graduates navigating this transition. Returning to a childhood bedroom after several years of independence can feel, for many, like a step backward — a disruption to the sense of adult autonomy that moving out in the first place was meant to represent.Interestingly, the research on this point is more reassuring than the popular narrative often suggests. A study examining the mental wellbeing impact of 'boomerang' moves in the UK found no evidence that returning home was associated with a deterioration in young adults' mental health, and some evidence of a slight improvement in wellbeing among those who returned — likely reflecting the genuine relief of reduced financial stress and pressure, even alongside the adjustment challenges of renegotiating household dynamics with parents.

The reframe that helps most graduates make peace with this stage: living at home temporarily, with a clear financial goal and a defined timeline, is not a step backward from independence — it is frequently the single fastest route toward genuine, lasting independence, whether that means a house deposit, a debt-free start, or simply a meaningful financial cushion most renting graduates never get the chance to build.

Conclusion

The marketing coordinator's £1,000 a month in savings is not an unusual stroke of luck — it is the predictable outcome of a specific, well-understood piece of financial arithmetic: removing the single largest cost in most young adults' budgets (rent) while still meaningfully contributing to household costs through bills. With UK rents continuing to outpace wage growth, graduate underemployment sitting at multi-year highs, and average student debt now exceeding £45,000, it is little wonder that the proportion of young adults living with parents has risen by more than a third over the past two decades, and that four in five first-time buyers are now using this exact strategy to save toward a deposit.What separates a productive version of this arrangement from a directionless one is not the living situation itself, but the structure placed around it: a clear and fair bills contribution agreed openly with parents, an automated and non-negotiable savings habit, a specific financial goal with a realistic timeline, and honest, ongoing communication about how long the arrangement is expected to last. Approached this way, moving back home after university is not a retreat from independence — it is frequently the most direct and financially efficient path toward it.

If you find yourself back in your childhood bedroom, or considering the move, the data suggests you are in good company, and the financial logic behind it is sound. The question worth asking is not whether this is an acceptable choice — the statistics make clear it increasingly is the choice an entire generation is making — but whether you are using the financial breathing room it creates with the same intentionality the marketing coordinator in this story has shown.

Frequently Asked Questions (FAQ)

How much should I contribute toward bills if I move back in with my parents?

There is no universal rule, but a common and fair approach is to calculate a proportional share of the household's actual recurring bills — energy, broadband, council tax, and a contribution to food — divided by the number of people in the household, then adjusted based on your income relative to other household members. Many families settle on a flat monthly figure somewhere between £200 and £400, depending on location and household size, agreed openly rather than left undefined.Is it better to save in a Lifetime ISA or a regular savings account while living at home?

If you are aged 18 to 39 and saving specifically toward a first home costing £450,000 or less, a Lifetime ISA is generally the more efficient choice, since the government adds a 25% bonus on contributions up to £4,000 per year — effectively free money that a standard savings account cannot match. If your goal is different, shorter-term, or you might need penalty-free access to the funds for something other than a first home, a competitive easy-access or fixed-term savings account may be more appropriate, since Lifetime ISA withdrawals for any other purpose incur a 25% government penalty.Will moving back home affect my credit score or mortgage application later?

Living with parents does not itself negatively affect your credit score. What matters for both your credit score and future mortgage applications is maintaining a track record of responsible financial behaviour — paying any credit commitments on time, keeping credit utilisation low, and registering on the electoral roll at your current address. In fact, the larger deposit you are able to build by living at home rent-free often improves your mortgage options later, since a bigger deposit typically unlocks better interest rates and a wider choice of lenders.How long do most people stay living with their parents after graduating?

This varies enormously by individual circumstances, but research suggests many graduates treat it as a multi-year, goal-oriented phase rather than a brief stopgap, particularly those saving toward a house deposit. TSB's 2025 research found the large majority of first-time buyers who returned home did so specifically to save for a deposit, suggesting many treat the arrangement as lasting until a clear financial milestone is reached, rather than for a fixed, predetermined period.Is it normal to feel like moving back home is a step backward, even if it makes financial sense?

Yes, this is an extremely common feeling, and research confirms the emotional adjustment is real even when the financial logic is sound. Encouragingly, studies examining the mental wellbeing impact of returning to the parental home have found no evidence of a deterioration in young adults' mental health, and some evidence of a slight improvement, likely linked to reduced financial stress. Reframing the arrangement around a specific goal and timeline, rather than viewing it as an open-ended retreat, tends to help most graduates feel more in control of the situation rather than less.External References

The following sources informed this article and are recommended for further reading:1. Institute for Fiscal Studies (IFS) — Young Adults Living With Parents, 2026 Research

https://ifs.org.uk/

2. Institute for Social and Economic Research (ISER), University of Essex — Boomerang Moves Research

https://www.iser.essex.ac.uk/

3. TSB — First-Time Buyer Research 2025: Moving Home to Save a Deposit

https://www.tsb.co.uk/news-releases/

4. Office for National Statistics — Private Rental Market Summary Statistics, UK

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/privaterentandhousepricesuk/latest

5. ScienceDirect — 'Boomerang' Moves and Young Adults' Mental Well-Being in the UK

https://www.sciencedirect.com/science/article/pii/S1040260823000060

6. GOV.UK — Lifetime ISA Official Guidance

https://www.gov.uk/lifetime-isa

7. Student Loans Company — Student Loan Statistics

https://www.gov.uk/government/organisations/student-loans-company

8. MoneyHelper — Budgeting and Saving Advice for Young Adults

https://www.moneyhelper.org.uk/en/everyday-money/budgeting

0 Comments Comments