Finance

RFID Blocking Wallet 2026: What Actually Works

Every wallet brand claims 'RFID blocking' in 2026. Most are exaggerating. A thin foil liner does not reliably block radio signals. Real-world RFID skimming is far rarer than the marketing suggests — but the threat is not zero, and for travellers and city commuters the peace of mind has genuine value. This guide explains exactly how RFID technology works, what the actual risk is, which wallets genuinely block signals versus those that merely claim to, and the five best tested picks of 2026.

The RFID chip in a modern contactless payment card is a passive device — it has no battery. It works by harvesting energy from the electromagnetic field generated by the reader, using that energy to power the chip briefly, and transmitting a response. The chip in most modern contactless payment cards operates at 13.56 MHz — the frequency used by NFC (Near Field Communication), which is the contactless payment standard used by Visa PayWave, Mastercard PayPass, and Apple Pay. Older transit cards, building access cards, and some ID documents may use 125 kHz, which has a slightly different risk profile.

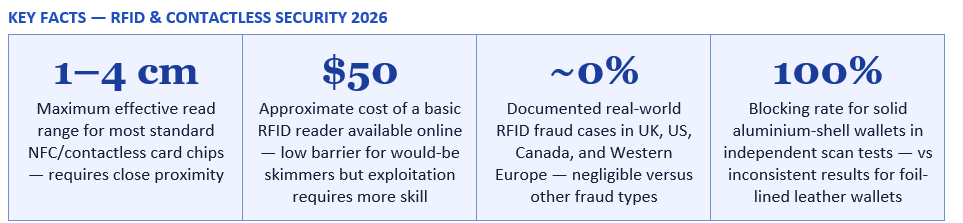

The read range of an NFC chip is typically one to four centimetres under standard conditions. This is why tap-to-pay requires physical proximity to the terminal — the reader must be very close to your card for the transaction to work. Some readers can extend this range under ideal conditions — unobstructed line of sight, no interference from other cards, laboratory-grade equipment — but the practical distance for any real-world skimming attempt is still measured in centimetres, not metres.

When you tap to pay, your actual card number isn't transmitted. Instead, a temporary token represents your account. Even if intercepted, this token can't be used for other transactions.

— PAPERWALLET — RFID BLOCKING WALLETS: DO YOU REALLY NEED ONE IN 2026? (FEBRUARY 2026)

For this to work, several conditions must be met. The attacker must get within a few centimetres of the target's wallet. The target must be carrying RFID-enabled cards. The cards must not be shielded by other cards, a metal wallet, or other obstructing materials. The attacker's reader must successfully interrogate the card. And the data captured must then be usable for fraud. Each of these conditions creates friction that reduces the real-world viability of the attack.

Modern contactless payment cards implement EMV tokenisation, which means that when a contactless transaction is initiated, the card does not transmit your actual card number. Instead it transmits a unique, one-time transaction token that is cryptographically linked to a specific transaction with a specific reader. According to Visa's own security documentation, cited across multiple sources including Norton and AARP: 'Visa contactless transactions generate a one-time, transaction-specific code. Due to the nature of the code and additional fraud protection processes built into the Visa network, it is difficult to use skimmed cardholder information for fraudulent purchases. As a result, fraud from skimming is very unlikely and limited in scope.'

What a successful RFID skim can capture, in a worst case, is the card number and expiration date. The CVV security code — required for most online card-not-present transactions — is not transmitted via NFC. Without the CVV, stolen card data has very limited utility for online fraud, which accounts for the vast majority of card fraud. In-person fraudulent transactions using skimmed NFC data would require a sophisticated cloning setup that is well beyond what most opportunistic criminals deploy.

BNDT's March 2026 analysis puts it plainly: 'Real-world RFID skimming causing financial loss is extremely rare, EMV tokenisation has made contactless cards far more secure than magnetic stripes, and the economics of RFID crime do not favour it over other forms of fraud. When criminals can purchase stolen card data in bulk on dark web marketplaces for pennies per record, why bother with technically challenging, low-yield RFID skimming?' The Reddit consensus on r/cybersecurity and r/privacy, cited by BNDT, reaches the same conclusion: RFID skimming is a theoretical threat that has not materialised into a practical one.

SlashGear's May 2026 analysis frames the issue accurately: 'RFID skimming is a legitimate concern in theory, but in practice it's a relatively rare method of financial fraud. There's no harm in opting for wallets with RFID shielding, but you likely don't need the extra protection.' The key takeaway is that an RFID blocking wallet is a reasonable, low-cost precaution with no downside — but it is not a critical security necessity for most people in most contexts, and it should not be prioritised over much more impactful security measures such as strong passwords, two-factor authentication, and phishing awareness.

Applied to an RFID-blocking wallet, the principle is that the wallet's lining or body contains a layer of conductive material — aluminium, copper mesh, or a metallic alloy fabric — that surrounds the cards and prevents external electromagnetic signals from reaching the RFID chips inside. When the wallet is closed, the conductive layer forms a near-complete Faraday cage around the card compartment. An RFID reader's electromagnetic field is attenuated or blocked before it can reach the cards, meaning the chips cannot harvest enough energy to power themselves and therefore cannot transmit any data.

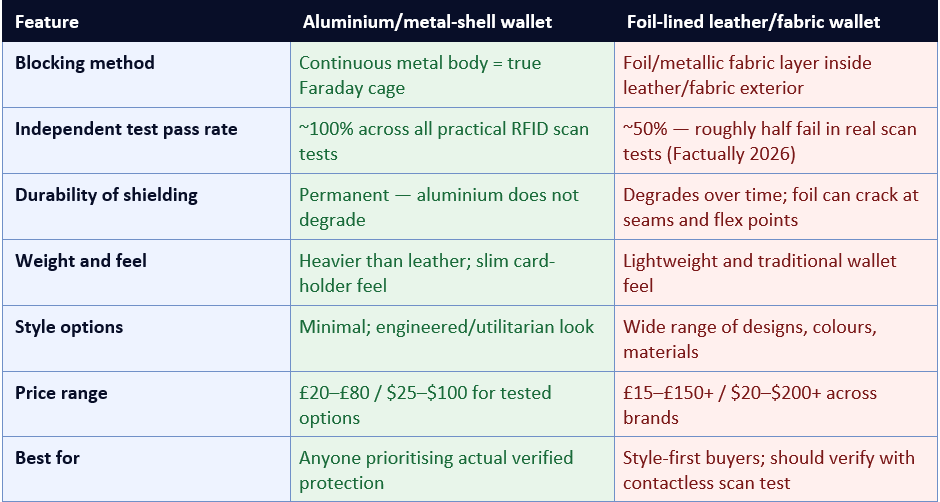

The effectiveness of this shielding depends critically on the material and its coverage. A solid aluminium or metal-shell wallet provides near-complete shielding — independent testers consistently report 100% blocking rates for wallets with continuous metal bodies. A wallet with a foil-lined leather or fabric body is far less reliable, because the foil layer is often thin, has gaps at seams and edges, and may degrade over time. The BNDT analysis published in March 2026 makes this distinction emphatically: 'Don't pay extra for a RFID blocking sticker on a leather wallet with a foil liner. If RFID protection matters to you, get a wallet with an actual aluminium body.'

The Factually review of tested wallets confirms the same finding: 'Independent testers report a clear split: wallets with a solid aluminium or metal shell pass every RFID scan test, while wallets that rely on a thin foil liner are inconsistent — roughly half fail in practical scans during hands-on tests.'

Sources: Factually (April 2026 lab test review), Travel + Leisure (NFC contactless test, Bellroy), CyberGuy (April 2026 picks), BNDT (March 2026 tested analysis). Prices approximate and may vary by retailer.

The most widely reviewed blocking card options in 2026 include the SignalVault, which uses what the manufacturer describes as E-Field technology, has been featured on Shark Tank, and is sold in two-card packs so you have a backup. CyberGuy's April 2026 review notes it can protect up to six nearby RFID-enabled cards per card and requires no setup or maintenance — you simply slide it into your wallet's card slot.

The Secret Trends review of the Wallet Defender card describes its mechanism as 'passive RFID-blocking technology — a metallic mesh or foil layer embedded within the card that absorbs and redirects the electromagnetic field generated by an external scanner.' Their test using an NFC reader app and a standard Android phone found that without the blocking card, card data was readable in under one second; with the card in the wallet, the scan failed completely.

The important caveat is that blocking cards work only for the cards stored in the same wallet compartment, close enough to be within the shielding field. A blocking card in the main card slot of a bifold wallet may not protect cards in a separate zipped compartment. And like all foil-based solutions, the effectiveness depends on material quality — cheaper blocking cards may provide inconsistent protection. For comprehensive coverage, a wallet with an integrated metal cage or aluminium body remains the more reliable solution.

Phishing attacks — emails, text messages, and phone calls that trick you into revealing your card details, banking credentials, or personal information — account for the overwhelming majority of consumer financial fraud in both the UK and the US. UK Finance's annual fraud report consistently shows that authorised push payment (APP) fraud and phishing represent the largest categories of consumer fraud loss by value. Card-not-present fraud (fraudulent online purchases using stolen card details, typically obtained via phishing or data breaches rather than RFID skimming) is the dominant form of card fraud. Data breaches — in which criminals acquire millions of card records at once by attacking merchants, payment processors, or financial institutions — are far more cost-effective from a criminal's perspective than trying to skim one card at a time in a crowd.

Physical ATM skimming — devices attached to ATM card readers that steal magnetic stripe data — remains a meaningful threat, particularly in tourist areas and at independent ATMs. This is a genuine and documented form of card fraud that steals magnetic stripe data, not NFC data. Using bank-installed ATMs inside bank branches, covering your PIN entry, and checking the card reader for tampering before inserting your card are the most effective countermeasures.

The security priorities that actually matter in 2026 are well-established: strong, unique passwords for all financial accounts and a password manager to manage them; two-factor authentication on all accounts where available; immediate transaction alerts from your bank for any charge above a specified threshold; regular review of bank and credit card statements; awareness of phishing techniques; and, for those who use the same magnetic stripe card frequently, the benefit of switching to contactless-only or digital wallet transactions. An RFID-blocking wallet is a reasonable supplementary measure — but it sits at the bottom of any honest prioritised security checklist, not at the top.

And yet: an RFID blocking wallet with verified shielding costs £30 to £80, has no downside, provides meaningful protection for more vulnerable credentials like e-passports and building access cards, and delivers genuine peace of mind for frequent travellers and urban commuters. If you are buying one, buy one that actually works — an aluminium-shell or independently tested wallet, not a foil-lined leather wallet with an untested blocking claim. The Bellroy Zip Wallet, Ekster Parliament, Secrid Miniwallet, and BNDT Maverick all provide verified protection in tested scenarios. If you do not want a new wallet, a blocking card insert provides an affordable, compact alternative. And whichever physical protection you choose, prioritise the digital security measures — strong passwords, two-factor authentication, transaction alerts — that address the threats you actually face.

Paperwallet — RFID Blocking Wallets: Do You Really Need One in 2026? (February 2026) https://paperwallet.com/blogs/the-paper-trail-blog/rfid-blocking-wallets-worth-it-2026

BNDT — Best RFID Blocking Wallet 2026: What Actually Works (March 2026) https://bndtla.com/blogs/news/best-rfid-blocking-wallet-2026-what-actually-works-and-whats-marketing-bs

BNDT — What Is RFID Blocking and Do You Actually Need It? (March 2026) https://bndtla.com/blogs/news/what-is-rfid-blocking-and-do-you-actually-need-it

Factually — Best RFID Blocking Wallets of 2026: Tested Picks (April 2026) https://factually.co/product-reviews/beauty-personal-care/best-rfid-blocking-wallets-2026-test-results-ec84ee

VaultSkin — RFID Skimming in 2026: What's Real, What's Hype (February 2026) https://vaultskin.com/blogs/news/rfid-skimming-2026-myths-facts-protection

VetoproPac — What Is RFID Blocking and Do You Actually Need It In Your Bag? (2026) https://vetopropac.com/rfid-blocking-backpack-do-you-need-it/

Norton — RFID Blocking: What It Is, How It Works, and Why You May Need It https://us.norton.com/blog/privacy/rfid-blocking

AARP — Do RFID-Blocking Wallets and Purses Work? (Expert analysis) https://www.aarp.org/money/scams-fraud/rfid-wallets-purses/

CyberGuy — Protect Your Credit Cards and IDs With the Best RFID-Blocking Cards (April 2026) https://cyberguy.com/gadgets/protect-credit-cards-ids-best-rfid-blocking-cards/

TABLE OF CONTENTS

- What Is RFID and How Does It Work?

- How RFID Skimming Actually Happens

- The Honest Risk Assessment: How Worried Should You Be?

- How RFID Blocking Works: The Science Explained

- The Critical Difference: Aluminium vs Foil-Lined Wallets

- Which Cards Actually Need RFID Protection?

- The Best RFID Blocking Wallets of 2026 — Tested

- RFID Blocking Cards: The Alternative to a New Wallet

- Five Things to Check Before Buying Any RFID Wallet

- Beyond RFID: The Real Fraud Threats You Face in 2026

- Practical Tips for Contactless Card Security

- Conclusion

- Frequently Asked Questions

- References

What Is RFID and How Does It Work?

RFID stands for Radio Frequency Identification. It is a wireless communication technology that uses electromagnetic fields to identify and track objects — or, in the case of payment cards and passports, to transmit data in response to a reader's signal. You interact with RFID technology every time you tap your contactless card at a payment terminal, swipe your work access badge, scan your passport at an e-gate, or use an Oyster card or Clipper card on public transport.The RFID chip in a modern contactless payment card is a passive device — it has no battery. It works by harvesting energy from the electromagnetic field generated by the reader, using that energy to power the chip briefly, and transmitting a response. The chip in most modern contactless payment cards operates at 13.56 MHz — the frequency used by NFC (Near Field Communication), which is the contactless payment standard used by Visa PayWave, Mastercard PayPass, and Apple Pay. Older transit cards, building access cards, and some ID documents may use 125 kHz, which has a slightly different risk profile.

The read range of an NFC chip is typically one to four centimetres under standard conditions. This is why tap-to-pay requires physical proximity to the terminal — the reader must be very close to your card for the transaction to work. Some readers can extend this range under ideal conditions — unobstructed line of sight, no interference from other cards, laboratory-grade equipment — but the practical distance for any real-world skimming attempt is still measured in centimetres, not metres.

When you tap to pay, your actual card number isn't transmitted. Instead, a temporary token represents your account. Even if intercepted, this token can't be used for other transactions.

— PAPERWALLET — RFID BLOCKING WALLETS: DO YOU REALLY NEED ONE IN 2026? (FEBRUARY 2026)

How RFID Skimming Actually Happens

RFID skimming — also called electronic pickpocketing or digital pickpocketing — is the practice of using a concealed RFID reader to capture data from someone's contactless cards or documents without their knowledge or consent. The theoretical attack scenario is well-understood: a person carries a hidden RFID reader in a backpack, shopping bag, or modified clothing item, positions themselves close to a target in a crowded space (a subway, airport, shopping centre, or concert), and attempts to trigger a read from cards in the target's wallet or bag.For this to work, several conditions must be met. The attacker must get within a few centimetres of the target's wallet. The target must be carrying RFID-enabled cards. The cards must not be shielded by other cards, a metal wallet, or other obstructing materials. The attacker's reader must successfully interrogate the card. And the data captured must then be usable for fraud. Each of these conditions creates friction that reduces the real-world viability of the attack.

Modern contactless payment cards implement EMV tokenisation, which means that when a contactless transaction is initiated, the card does not transmit your actual card number. Instead it transmits a unique, one-time transaction token that is cryptographically linked to a specific transaction with a specific reader. According to Visa's own security documentation, cited across multiple sources including Norton and AARP: 'Visa contactless transactions generate a one-time, transaction-specific code. Due to the nature of the code and additional fraud protection processes built into the Visa network, it is difficult to use skimmed cardholder information for fraudulent purchases. As a result, fraud from skimming is very unlikely and limited in scope.'

What a successful RFID skim can capture, in a worst case, is the card number and expiration date. The CVV security code — required for most online card-not-present transactions — is not transmitted via NFC. Without the CVV, stolen card data has very limited utility for online fraud, which accounts for the vast majority of card fraud. In-person fraudulent transactions using skimmed NFC data would require a sophisticated cloning setup that is well beyond what most opportunistic criminals deploy.

The Honest Risk Assessment: How Worried Should You Be?

This section deliberately presents the most honest, evidence-based assessment of RFID skimming risk available — because the market for RFID-blocking wallets is heavily influenced by marketing that overstates the threat, and consumers deserve accurate information.What the evidence shows

Law enforcement agencies in the UK, US, Canada, Australia, and across Western Europe report virtually no documented cases of criminals successfully using RFID skimming to commit financial fraud in the wild. As the Paperwallet analysis published in February 2026 states: 'The UK's National Fraud Intelligence Bureau, financial industry security experts, and consumer protection agencies consistently report that RFID fraud represents a negligible fraction of card crime.' VetoproPac's 2026 security analysis draws a similar conclusion: 'Comprehensive search of law enforcement reports, fraud statistics, and security research reveals virtually zero documented cases of actual RFID skimming causing financial loss in developed countries.'BNDT's March 2026 analysis puts it plainly: 'Real-world RFID skimming causing financial loss is extremely rare, EMV tokenisation has made contactless cards far more secure than magnetic stripes, and the economics of RFID crime do not favour it over other forms of fraud. When criminals can purchase stolen card data in bulk on dark web marketplaces for pennies per record, why bother with technically challenging, low-yield RFID skimming?' The Reddit consensus on r/cybersecurity and r/privacy, cited by BNDT, reaches the same conclusion: RFID skimming is a theoretical threat that has not materialised into a practical one.

The nuance: theoretical is not impossible

The low documented risk does not mean the threat is zero or static. Security researchers continue to find edge cases and vulnerabilities in specific card implementations. Some older RFID-enabled ID documents and transit cards — particularly those using 125 kHz rather than 13.56 MHz NFC — have weaker encryption and are more vulnerable to cloning. As contactless cards become more prevalent and RFID readers more sophisticated, the risk landscape can shift. And for certain high-risk environments — international travel to regions with different fraud dynamics, crowded tourist hotspots, or contexts where someone is carrying high-value RFID documents such as an e-passport — the practical case for protection is stronger.SlashGear's May 2026 analysis frames the issue accurately: 'RFID skimming is a legitimate concern in theory, but in practice it's a relatively rare method of financial fraud. There's no harm in opting for wallets with RFID shielding, but you likely don't need the extra protection.' The key takeaway is that an RFID blocking wallet is a reasonable, low-cost precaution with no downside — but it is not a critical security necessity for most people in most contexts, and it should not be prioritised over much more impactful security measures such as strong passwords, two-factor authentication, and phishing awareness.

How RFID Blocking Works: The Science Explained

An RFID blocking wallet works on the principle of a Faraday cage — a concept in physics named after the nineteenth-century scientist Michael Faraday. A Faraday cage is an enclosure made of conductive material (typically metal) that blocks electromagnetic fields by redistributing charges within the material in response to an external field, effectively cancelling the field inside the enclosure. A metal box is a perfect Faraday cage. A metal mesh, if the holes are smaller than the wavelength of the signal being blocked, achieves the same effect.Applied to an RFID-blocking wallet, the principle is that the wallet's lining or body contains a layer of conductive material — aluminium, copper mesh, or a metallic alloy fabric — that surrounds the cards and prevents external electromagnetic signals from reaching the RFID chips inside. When the wallet is closed, the conductive layer forms a near-complete Faraday cage around the card compartment. An RFID reader's electromagnetic field is attenuated or blocked before it can reach the cards, meaning the chips cannot harvest enough energy to power themselves and therefore cannot transmit any data.

The effectiveness of this shielding depends critically on the material and its coverage. A solid aluminium or metal-shell wallet provides near-complete shielding — independent testers consistently report 100% blocking rates for wallets with continuous metal bodies. A wallet with a foil-lined leather or fabric body is far less reliable, because the foil layer is often thin, has gaps at seams and edges, and may degrade over time. The BNDT analysis published in March 2026 makes this distinction emphatically: 'Don't pay extra for a RFID blocking sticker on a leather wallet with a foil liner. If RFID protection matters to you, get a wallet with an actual aluminium body.'

The Factually review of tested wallets confirms the same finding: 'Independent testers report a clear split: wallets with a solid aluminium or metal shell pass every RFID scan test, while wallets that rely on a thin foil liner are inconsistent — roughly half fail in practical scans during hands-on tests.'

The Critical Difference: Aluminium vs Foil-Lined Wallets

Which Cards Actually Need RFID Protection?

Not all the cards and documents you carry pose the same RFID risk profile. Understanding which items in your wallet are actually vulnerable helps you make a rational decision about protection.RFID risk by card type — from highest to lowest vulnerability

- E-passports (biometric passports): These contain an RFID chip holding your personal data including name, date of birth, nationality, and a digital photo. Unlike payment cards, some e-passport implementations have had documented vulnerabilities — though modern passports include Basic Access Control (BAC) or Supplemental Access Control (SAC) encryption that requires the optical data on the passport page to be read first before the chip responds. Nonetheless, for international travellers, this is the most legitimate use case for RFID blocking.

- Building access cards and hotel key cards: These typically use 125 kHz RFID technology without strong encryption. They are genuinely cloneable with inexpensive equipment and have been demonstrated as vulnerable in security research. If you carry a workplace access card daily, RFID blocking prevents the theoretical risk of someone cloning your access credentials in proximity.

- Older contactless transit cards: Cards like older versions of transit passes in some markets use 125 kHz MIFARE technology with weaker encryption. Newer implementations (Oyster, Clipper, etc.) have been upgraded to more secure protocols but older cards still in circulation may have higher vulnerability.

- Modern contactless payment cards (lowest risk): EMV NFC payment cards (Visa PayWave, Mastercard PayPass) are protected by tokenisation — they transmit a one-time code, not your card number. Even if skimmed, the data has extremely limited fraud utility. Contactless transactions are also capped at low amounts (typically £100 in the UK, $100–$250 in the US) requiring PIN for larger amounts. The risk is low and the cardholder is protected by zero-liability fraud policies.

- Driving licences and government IDs: Most UK and US driving licences do not currently contain RFID chips. However, enhanced driving licences (EDL) in the US and some national ID cards in Europe do. Check whether your specific document has the contactless symbol before assuming it needs RFID protection.

The Best RFID Blocking Wallets of 2026 — Tested

The following wallets have been identified by independent review sources including Factually's lab-style testing, Travel + Leisure's practical NFC verification, CyberGuy's 2026 picks, and VaultSkin's 2026 analysis. All have been selected on the basis of verified blocking effectiveness rather than marketing claims alone.Sources: Factually (April 2026 lab test review), Travel + Leisure (NFC contactless test, Bellroy), CyberGuy (April 2026 picks), BNDT (March 2026 tested analysis). Prices approximate and may vary by retailer.

Bellroy Zip Wallet — Best overall

Bellroy is one of the most extensively reviewed wallet brands in the world, and the Zip Wallet is its most widely recommended option. Travel + Leisure named it 'Best Overall,' praised the zipper security and slim profile, and confirmed RFID blocking by testing contactless payments without removing cards — the card could not complete a tap-to-pay transaction while inside the closed wallet. It is a leather wallet with a tested RFID liner, not a metal-shell design, which means its blocking relies on the liner integrity. The Travel + Leisure contactless test confirmation gives it substantially more credibility than wallets that simply print 'RFID blocking' on the packaging without verification.Ekster Parliament — Best for everyday carry

Ekster's Parliament wallet is a slim, engineered card-holder with a quick-deploy mechanism for fast card access and an aluminium card cage that protects the cards in the main compartment. Factually's comparative testing rated it 'best for everyday EDC with tech features,' with reliable blocking confirmed in repeated comparative tests. The slim profile fits comfortably in a front pocket, which itself reduces the practical theft risk from conventional pickpocketing alongside the RFID protection.Secrid Miniwallet — Best for bifold users

Secrid is a Dutch brand that pioneered the aluminium card protector insert for bifold wallets. The Miniwallet combines a leather bifold exterior with a rigid aluminium internal cage that holds four to six cards. The aluminium cage provides genuine Faraday-cage-level protection for the stored cards, and Secrid's mechanism allows rapid card deployment. Factually's review highlights Secrid's 'durable build and handiness' as key differentiators. It is particularly suited to users who want a traditional-feeling wallet with the reassurance of metal-shell blocking.BNDT Maverick — Best for absolute blocking

For those who want the highest verified protection regardless of aesthetics, the BNDT Maverick is the top recommendation from BNDT's own March 2026 analysis. It features a solid aluminium body that forms a complete Faraday cage around the card compartment, a quick-trigger card access mechanism, holds up to seven cards, and is priced at around $55 — making verified, complete blocking accessible without a premium price. Independent testers report 100% pass rates in RFID scan tests.RFID Blocking Cards: The Alternative to a New Wallet

If you do not want to replace your existing wallet — whether because you love the one you have, it was an expensive gift, or you simply do not want to spend on a new wallet — RFID blocking cards offer an alternative. These are credit-card-sized inserts that you place inside your existing wallet alongside your payment cards, providing a shielding effect around the cards stored nearby.The most widely reviewed blocking card options in 2026 include the SignalVault, which uses what the manufacturer describes as E-Field technology, has been featured on Shark Tank, and is sold in two-card packs so you have a backup. CyberGuy's April 2026 review notes it can protect up to six nearby RFID-enabled cards per card and requires no setup or maintenance — you simply slide it into your wallet's card slot.

The Secret Trends review of the Wallet Defender card describes its mechanism as 'passive RFID-blocking technology — a metallic mesh or foil layer embedded within the card that absorbs and redirects the electromagnetic field generated by an external scanner.' Their test using an NFC reader app and a standard Android phone found that without the blocking card, card data was readable in under one second; with the card in the wallet, the scan failed completely.

The important caveat is that blocking cards work only for the cards stored in the same wallet compartment, close enough to be within the shielding field. A blocking card in the main card slot of a bifold wallet may not protect cards in a separate zipped compartment. And like all foil-based solutions, the effectiveness depends on material quality — cheaper blocking cards may provide inconsistent protection. For comprehensive coverage, a wallet with an integrated metal cage or aluminium body remains the more reliable solution.

9. Five Things to Check Before Buying Any RFID Wallet

What to verify before buying — the 5-point RFID wallet checklist

- Has it been independently tested — not just claimed? Look for wallets that have been verified by a named publication (Travel + Leisure's contactless NFC test, Factually's lab-style review, BNDT's scan analysis) rather than simply bearing a 'RFID blocking' or 'RFID safe' label. Any brand can print these words on packaging. Independent scan test confirmation is what separates genuine blocking from marketing copy.

- What is the shielding material? Aluminium or metal-shell wallets provide the most consistent, verifiable protection. Foil-lined leather or fabric wallets are inconsistent — Factually's testing found roughly half fail in practical scans. If the product description says 'foil liner,' treat its blocking claims with scepticism unless backed by third-party scan testing.

- Does it cover all card compartments equally? Some wallets protect the main card slot but not secondary pockets. Check whether the RFID shielding covers every section where you intend to store contactless cards. A blocking wallet that leaves your passport pocket unshielded is not providing the protection you assume.

- Will it interfere with your daily use? RFID blocking wallets prevent cards from responding to all RFID readers — including legitimate ones. To use tap-to-pay, you will need to physically remove the card from the wallet first (or, for some metal-shell wallets, open the wallet fully before tapping). If you use contactless payment dozens of times per day, consider whether the small friction of card removal is acceptable. If you primarily use a digital wallet (Apple Pay, Google Pay) for contactless payments, this is not a practical concern.

- Does it fit your everyday carry needs? The best RFID wallet is the one you will actually use consistently. A wallet that provides excellent RFID protection but is too bulky for a front pocket, too stiff to hold receipts, or incompatible with your daily routine will be abandoned in favour of a non-blocking alternative — leaving your cards unprotected anyway. Functionality and RFID protection should both be satisfied by your choice.

Beyond RFID: The Real Fraud Threats You Face in 2026

The honest consumer guide to contactless security must spend at least as much time on the real threats as on RFID — because the marketing around RFID-blocking wallets has created a distorted picture of where your security attention should actually be directed.Phishing attacks — emails, text messages, and phone calls that trick you into revealing your card details, banking credentials, or personal information — account for the overwhelming majority of consumer financial fraud in both the UK and the US. UK Finance's annual fraud report consistently shows that authorised push payment (APP) fraud and phishing represent the largest categories of consumer fraud loss by value. Card-not-present fraud (fraudulent online purchases using stolen card details, typically obtained via phishing or data breaches rather than RFID skimming) is the dominant form of card fraud. Data breaches — in which criminals acquire millions of card records at once by attacking merchants, payment processors, or financial institutions — are far more cost-effective from a criminal's perspective than trying to skim one card at a time in a crowd.

Physical ATM skimming — devices attached to ATM card readers that steal magnetic stripe data — remains a meaningful threat, particularly in tourist areas and at independent ATMs. This is a genuine and documented form of card fraud that steals magnetic stripe data, not NFC data. Using bank-installed ATMs inside bank branches, covering your PIN entry, and checking the card reader for tampering before inserting your card are the most effective countermeasures.

The security priorities that actually matter in 2026 are well-established: strong, unique passwords for all financial accounts and a password manager to manage them; two-factor authentication on all accounts where available; immediate transaction alerts from your bank for any charge above a specified threshold; regular review of bank and credit card statements; awareness of phishing techniques; and, for those who use the same magnetic stripe card frequently, the benefit of switching to contactless-only or digital wallet transactions. An RFID-blocking wallet is a reasonable supplementary measure — but it sits at the bottom of any honest prioritised security checklist, not at the top.

Practical Tips for Contactless Card Security

Practical contactless security tips for 2026

- Enable transaction alerts: Set up real-time transaction notifications from your bank or card issuer for every transaction, or at minimum for any transaction above a small threshold (£1/$1). This means any fraudulent transaction — RFID or otherwise — is flagged to you within seconds, enabling immediate card blocking and fraud reporting.

- Know your contactless transaction limits: In the UK, contactless transactions above £100 require your PIN. In the US, the limit varies by card issuer but is typically $100–$250. Large fraudulent transactions would require your PIN regardless of how the card data was obtained — limiting potential losses even in a worst-case skimming scenario.

- Use Apple Pay or Google Pay for contactless payments: Digital wallets tokenise every transaction independently and store your card details on the device rather than on a physical card chip. They require device authentication (biometric or PIN) for every transaction, making them significantly more secure than physical card taps for contactless use. If you use Apple Pay or Google Pay, the physical card in your wallet is irrelevant for everyday contactless payments.

- Test your wallet before relying on it: If you buy an RFID-blocking wallet or insert a blocking card, test it. Use your phone's NFC settings or the NFC reader function of an Android phone to try to read a contactless card both before and after the wallet is closed around it. This is the same method used by Travel + Leisure in its testing and provides immediate verification of whether your wallet is actually blocking.

- Report fraud immediately and know your zero-liability rights: In the UK, banks are required by the Payment Services Regulations to refund unauthorised contactless transactions unless you have acted with gross negligence. In the US, zero-liability policies from Visa, Mastercard, and American Express cover unauthorised contactless charges. The financial risk of contactless card fraud is substantially lower than many consumers believe, precisely because of these protections.

- Carry fewer RFID-enabled cards: Every RFID-enabled card in your wallet is another potential scan target. Consider whether you need to carry all your contactless cards every day. A travel card, a building access card, and two payment cards represent a typical risk profile. Additional RFID-enabled cards should be left at home if not needed.

CONCLUSION

The honest conclusion about RFID blocking wallets in 2026 is this: the real-world risk of RFID skimming is very low — law enforcement in the UK, US, and Western Europe documents virtually no cases of consumer financial loss attributable to contactless card skimming. EMV tokenisation has made modern payment cards inherently resistant to the most straightforward skimming attacks. And your financial risk from phishing, data breaches, and ATM skimming is orders of magnitude higher than your risk from someone waving an NFC reader near your wallet on the Tube.And yet: an RFID blocking wallet with verified shielding costs £30 to £80, has no downside, provides meaningful protection for more vulnerable credentials like e-passports and building access cards, and delivers genuine peace of mind for frequent travellers and urban commuters. If you are buying one, buy one that actually works — an aluminium-shell or independently tested wallet, not a foil-lined leather wallet with an untested blocking claim. The Bellroy Zip Wallet, Ekster Parliament, Secrid Miniwallet, and BNDT Maverick all provide verified protection in tested scenarios. If you do not want a new wallet, a blocking card insert provides an affordable, compact alternative. And whichever physical protection you choose, prioritise the digital security measures — strong passwords, two-factor authentication, transaction alerts — that address the threats you actually face.

Frequently Asked Questions

Do I actually need an RFID blocking wallet in 2026?

For most people in the UK, US, Canada, and Western Europe, the honest answer is no — not as a critical security necessity. Law enforcement agencies report virtually no documented cases of criminals successfully using RFID skimming to commit financial fraud in these regions. Modern contactless payment cards use EMV tokenisation, which means they transmit a one-time code rather than your card number, severely limiting the utility of any skimmed data. That said, there is no downside to having RFID blocking, and it provides meaningful protection for more vulnerable items like e-passports and building access cards. If you travel frequently, commute through very crowded environments, or simply value the peace of mind, a tested blocking wallet is a reasonable, low-cost investment. If you are looking for the most impactful security upgrade, focus on phishing awareness, two-factor authentication, and transaction alerts first.What is the difference between RFID and NFC?

NFC (Near Field Communication) is a specific, short-range subset of RFID technology. All NFC is RFID, but not all RFID is NFC. NFC operates at 13.56 MHz and has a read range of 1–4 centimetres, making it the standard for contactless payments (Visa PayWave, Mastercard PayPass), Apple Pay, and Google Pay. Older RFID technologies operate at 125 kHz or 134 kHz and are used in some building access cards, older transit cards, and pet microchips. When a wallet is marketed as 'RFID blocking,' it should block both NFC (13.56 MHz) and lower-frequency RFID signals. Most quality blocking wallets cover the full spectrum. When reviewing a blocking wallet, check whether the manufacturer specifies which frequencies are blocked.How do I know if my wallet is actually blocking RFID?

The most reliable test is also the simplest: try to make a contactless payment with your card while it remains inside the closed wallet. If the payment fails (because the card cannot communicate with the terminal through the wallet), your wallet is blocking. If it succeeds, it is not blocking effectively. An alternative is to use an Android smartphone with NFC capability to attempt to read your contactless card: open the phone's NFC settings or download a free NFC reader app, attempt to scan your card through the wallet, and observe whether the phone detects the card. Travel + Leisure uses this contactless-payment test approach to verify blocking in their wallet reviews. This test is free, takes 30 seconds, and tells you definitively whether your wallet is providing actual protection.Does RFID blocking affect my ability to use contactless payment?

Yes — when the card is inside a properly blocking wallet, it cannot make contactless payments. To use tap-to-pay, you need to remove your card from the wallet first (or, for some designs, open the wallet fully so the shielding is no longer enclosing the card). This is a deliberate feature, not a bug: the blocking is working exactly as intended. If you use Apple Pay or Google Pay for most contactless transactions, this is not a practical issue because your physical card stays in the wallet and you pay via your phone. If you frequently use your physical card for tap-to-pay dozens of times per day, the additional step of removing the card may be a minor inconvenience worth considering before buying a metal-shell wallet.Are foil-lined leather RFID wallets actually effective?

In many cases, no — or at least not reliably. Factually's April 2026 review of tested wallets found that 'wallets with a solid aluminium or metal shell pass every RFID scan test, while wallets that rely on a thin foil liner are inconsistent — roughly half fail in practical scans during hands-on tests.' The BNDT March 2026 analysis reaches the same conclusion: a thin foil liner does not reliably block RFID signals, and the mere presence of a 'RFID blocking' label on a leather wallet is not a reliable indicator of effectiveness. If you choose a leather wallet, look for one with independently verified blocking (tested by a named publication with a described method) rather than relying on manufacturer claims alone. The Bellroy Zip Wallet is an example of a leather wallet that has passed independent contactless scan verification.What is a Faraday cage and how does it relate to RFID blocking?

A Faraday cage is an enclosure made of conductive material that blocks electromagnetic fields by redistributing charges in response to an external field, cancelling the field inside the enclosure. It is named after physicist Michael Faraday. Applied to RFID blocking, a wallet with a complete metal or aluminium body creates a Faraday cage effect around the card compartment — any electromagnetic signal from an external RFID reader is attenuated before it can reach the cards inside. Wallets described as providing 'Faraday cage' protection typically have a continuous aluminium or metal shell rather than a lined interior. Solid aluminium wallets like the BNDT Maverick provide the most complete Faraday cage effect available in a consumer wallet, and consistently pass 100% of independent scan tests as a result.References and Further Reading

SlashGear — Are RFID-Blocking Wallets Still Needed Or Useful In 2026? (May 2026) https://www.slashgear.com/2165804/do-you-need-rfid-blocking-wallet-2026/Paperwallet — RFID Blocking Wallets: Do You Really Need One in 2026? (February 2026) https://paperwallet.com/blogs/the-paper-trail-blog/rfid-blocking-wallets-worth-it-2026

BNDT — Best RFID Blocking Wallet 2026: What Actually Works (March 2026) https://bndtla.com/blogs/news/best-rfid-blocking-wallet-2026-what-actually-works-and-whats-marketing-bs

BNDT — What Is RFID Blocking and Do You Actually Need It? (March 2026) https://bndtla.com/blogs/news/what-is-rfid-blocking-and-do-you-actually-need-it

Factually — Best RFID Blocking Wallets of 2026: Tested Picks (April 2026) https://factually.co/product-reviews/beauty-personal-care/best-rfid-blocking-wallets-2026-test-results-ec84ee

VaultSkin — RFID Skimming in 2026: What's Real, What's Hype (February 2026) https://vaultskin.com/blogs/news/rfid-skimming-2026-myths-facts-protection

VetoproPac — What Is RFID Blocking and Do You Actually Need It In Your Bag? (2026) https://vetopropac.com/rfid-blocking-backpack-do-you-need-it/

Norton — RFID Blocking: What It Is, How It Works, and Why You May Need It https://us.norton.com/blog/privacy/rfid-blocking

AARP — Do RFID-Blocking Wallets and Purses Work? (Expert analysis) https://www.aarp.org/money/scams-fraud/rfid-wallets-purses/

CyberGuy — Protect Your Credit Cards and IDs With the Best RFID-Blocking Cards (April 2026) https://cyberguy.com/gadgets/protect-credit-cards-ids-best-rfid-blocking-cards/

0 Comments Comments