Savings

Vacation vs Saving in 2026: What Would You Choose?

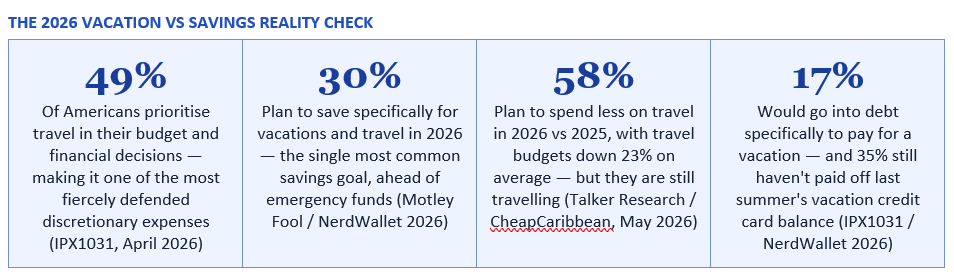

Forty-nine per cent of Americans say they prioritise travel when making financial decisions, according to IPX1031's April 2026 travel report. But one in five of those same people would go into debt to pay for a vacation — and NerdWallet's April 2026 summer travel survey found that 35% of Americans who put last summer's vacation on a credit card still haven't paid it off. The vacation-versus-saving debate is not simply about preference. It is about whether the way you fund your trips is working for you or against you. This guide gives you the framework to do both.

Travel is not a financial vice to be eliminated from a responsible financial life. Research consistently shows that experiences — particularly travel and time with people we care about — produce more lasting wellbeing than material purchases. The Empower 2025 travel survey found that 44% of Americans describe the memories made on vacation as 'priceless,' and 24% prefer to see travel as an investment in themselves. CIT Bank's 2025 Summer Savings Survey is even more direct: the head of the bank notes that 'saving for a vacation is an optimistic and aspirational financial goal — you spend months looking forward to the trip, then you can enjoy the experience knowing you're financially prepared.'

The real debate is not vacation versus saving. It is how you fund a vacation. Two people who both take the same holiday in the same year have entirely different financial outcomes depending on whether one used a sinking fund and the other used a credit card. The trip was the same. The financial consequences were worlds apart. This guide is about becoming the person who takes the trip and arrives home financially ahead rather than financially behind.

The best vacation is one you can actually afford. And the best memories don't require maxing out your credit cards.

— SARA RATHNER, NERDWALLET CREDIT CARD EXPERT — 2025 HOLIDAY SPENDING REPORT

The sequencing matters. Before treating travel as a financial priority, three foundations should be in place: a micro emergency fund of at least $500 to $1,000 (the first line of defence against setbacks that otherwise create debt); minimum contributions to workplace pension or 401(k) to at least capture the employer match (a guaranteed 50% to 100% return that no holiday can match); and the absence of high-interest credit card debt being actively added to each month. None of these conditions requires perfection or years of effort. Many households can establish this baseline in three to six months — at which point travel becomes an unambiguous positive rather than a joy that comes with a financial shadow.

Talker Research's May 2026 CheapCaribbean survey confirms that 70% of Americans are being more financially cautious in 2026, and 74% of those reducing travel spending cite the primary reason as needing to be more careful with finances. This is not pessimism — it is appropriate prioritisation. Financial caution in 2026 is the responsible response to a year (2025) in which 77% of Americans experienced a financial setback.

There is also a compellingly practical argument against indefinitely deferring travel in favour of saving: time is the one resource that cannot be recovered or invested. A holiday with your children when they are young is not interchangeable with the same holiday when they are adults. A trip with ageing parents cannot be taken after they are gone. The desire to save 'until things are better financially' can become a permanent deferral if 'better financially' is never specifically defined.

The 24% of Americans who describe travel as 'an investment in themselves' (Empower 2025) and the 20% who 'prioritise travel regardless of what's going on in the economy' are not being financially irresponsible — they are expressing a clear values-based prioritisation that is entirely valid within a responsible budget. The key qualification is: prioritising travel within a budget is healthy; prioritising travel above a budget is the specific behaviour that creates the debt burden that makes everything else harder.

NerdWallet's April 2026 Summer Travel Survey documents the scale of this: 74% of 2025 summer travelers who paid for their vacation with a credit card did not pay off the balance immediately after returning. More than a third — 35% — still had not paid off last summer's vacation balance as of April 2026. This means that for these households, the 2026 summer vacation will begin before the 2025 one is paid for. The interest on last year's trip is funding this year's planning period.

IPX1031's April 2026 data adds a further dimension: 17% of Americans say they would go into debt specifically to pay for a vacation, and 1 in 10 plan to take on debt for travel in 2026, with the average amount being $2,525. At 22% credit card APR, $2,525 generates approximately $555 in annual interest — the equivalent of a flight, a weekend hotel, or most of a budget break. The holiday costs $2,525 plus $555 in interest for those who carry the balance. It costs $2,525 for those who saved for it first. The experience is identical. The financial outcome is not.

A vacation sinking fund is a dedicated savings pot — separate from your emergency fund and main savings — specifically for travel. It is funded in small weekly or monthly amounts year-round, so that when a holiday booking opens, the money is already there. You spend it guilt-free because you saved it deliberately. You return home with zero new credit card debt related to the trip. The next saving cycle begins immediately.

CIT Bank's 2025 Summer Savings Survey captures the experience of this approach precisely: 'You spend months looking forward to the trip, then you can enjoy the experience knowing you're financially prepared. Afterward, you return home with memories that can last a lifetime.' The anticipation of a planned, funded trip is itself a source of wellbeing — you get the benefit of looking forward to the holiday for months, whereas an impulsive credit card booking produces anxiety about the bill alongside the anticipation of the trip.

In all other circumstances — stable income, emergency fund in place, no actively growing credit card debt — a planned, sinking-fund-financed holiday is a financially sound and personally valid priority.

The mechanism is straightforward: a travel rewards card earns points on everyday purchases — groceries, petrol, utilities, dining — and those points can be redeemed for flights, hotel nights, and travel-related costs. A card earning 2 to 3 points per pound or dollar on spending produces approximately 2 to 3% of spend in travel value. On $3,000 of monthly household spending, that is $60 to $90 per month in travel value — $720 to $1,080 per year — at zero additional cost beyond what would be spent anyway.

The non-negotiable condition for travel rewards cards is paying the balance in full every month. A card balance at 22% APR eliminates the rewards value entirely and then some — a $1,000 in rewards earned on $50,000 of annual spending is worth nothing if the card accrues $500 in interest. Travel rewards cards are a genuine wealth tool only for people who use them as a payment method for budgeted spending rather than as a means of spending beyond their budget. NerdWallet's Sara Rathner notes: 'While it can be tempting to hoard rewards for a major trip, points and miles can lose value over time, so it's a good idea to use them as you need them.'

The vacation sinking fund changes the answer from 'vacation OR saving' to 'vacation AND saving.' $100 to $200 per month, automated into a named travel account, produces $1,200 to $2,400 per year of guilt-free travel money — enough for most of the holidays that most people want. Combine it with a travel rewards card paid in full monthly, smart booking timing, and the cost-saving strategies in this guide, and the best vacation you can actually afford is likely better than you think it is. Save for it first. Spend it without guilt. Return home financially whole.

NerdWallet — 2026 Summer Travel Report: How Americans Plan and Pay (April 2026) https://www.nerdwallet.com/travel/studies/summer-travel-report

Talker Research / Hotel News Resource — Americans Focus on Value as Travel Spending Drops for 2026 (May 2026) https://www.hotelnewsresource.com/article141186.html

Motley Fool Money — Top Financial New Year's Resolutions for 2026 (November 2025) https://www.fool.com/the-ascent/research/financial-new-years-resolutions

CIT Bank / Barchart — Young Americans Saving for Bigger Vacations: CIT Bank 2025 Summer Savings Survey (August 2025) https://www.barchart.com/story/news/33921306/young-americans-are-planning-and-saving-for-bigger-vacations-this-summer-new-cit-bank-survey-finds

Empower — Travel Spending Trends Research: Half of Americans Say Vacation Memories Are Priceless (2025) https://www.empower.com/the-currency/play/travel-spending-trends-research

NerdWallet — 2025 Holiday Spending Report: How Americans Pay for Holiday Travel https://www.nerdwallet.com/credit-cards/studies/holiday-spending-report

TABLE OF CONTENTS

- The Debate: Why This Is Not an Either/Or Question

- The Case for Saving First

- The Case for Prioritising Travel

- The Real Problem: How Most People Fund Their Holidays

- The Both/And Solution: The Vacation Sinking Fund

- How to Build Your Vacation Fund in Five Steps

- Travelling Smarter: How to Spend Less Without Experiencing Less

- When Saving Must Come Before Travel

- The Travel Rewards Approach: Funding Holidays Through Everyday Spending

- Conclusion

- Frequently Asked Questions

- References

The Debate: Why This Is Not an Either/Or Question

The vacation-versus-saving framing presents the choice as a binary: you either take the trip or you save the money. In practice, the data shows that most people refuse to accept this binary — and for good reason. IPX1031's April 2026 travel survey found that 49% of Americans prioritise travel in their budgets, and Motley Fool's November 2025 Financial New Year's Resolution Report found that 30% of Americans plan to save specifically for vacations and travel in 2026 — making it the single most common savings goal, ahead of emergency funds, retirement, and home purchases.Travel is not a financial vice to be eliminated from a responsible financial life. Research consistently shows that experiences — particularly travel and time with people we care about — produce more lasting wellbeing than material purchases. The Empower 2025 travel survey found that 44% of Americans describe the memories made on vacation as 'priceless,' and 24% prefer to see travel as an investment in themselves. CIT Bank's 2025 Summer Savings Survey is even more direct: the head of the bank notes that 'saving for a vacation is an optimistic and aspirational financial goal — you spend months looking forward to the trip, then you can enjoy the experience knowing you're financially prepared.'

The real debate is not vacation versus saving. It is how you fund a vacation. Two people who both take the same holiday in the same year have entirely different financial outcomes depending on whether one used a sinking fund and the other used a credit card. The trip was the same. The financial consequences were worlds apart. This guide is about becoming the person who takes the trip and arrives home financially ahead rather than financially behind.

The best vacation is one you can actually afford. And the best memories don't require maxing out your credit cards.

— SARA RATHNER, NERDWALLET CREDIT CARD EXPERT — 2025 HOLIDAY SPENDING REPORT

The Case for Saving First

Financial security is the foundation on which everything else is built — including enjoyable holidays. A vacation taken by someone who does not have an emergency fund is a gamble: if a car repair, medical bill, or job change arrives in the weeks after they return, they have no financial buffer and will likely use the same credit card that still has the holiday balance on it. The financial stress that follows can make the holiday feel pyrrhic in retrospect.The sequencing matters. Before treating travel as a financial priority, three foundations should be in place: a micro emergency fund of at least $500 to $1,000 (the first line of defence against setbacks that otherwise create debt); minimum contributions to workplace pension or 401(k) to at least capture the employer match (a guaranteed 50% to 100% return that no holiday can match); and the absence of high-interest credit card debt being actively added to each month. None of these conditions requires perfection or years of effort. Many households can establish this baseline in three to six months — at which point travel becomes an unambiguous positive rather than a joy that comes with a financial shadow.

Talker Research's May 2026 CheapCaribbean survey confirms that 70% of Americans are being more financially cautious in 2026, and 74% of those reducing travel spending cite the primary reason as needing to be more careful with finances. This is not pessimism — it is appropriate prioritisation. Financial caution in 2026 is the responsible response to a year (2025) in which 77% of Americans experienced a financial setback.

The Case for Prioritising Travel

There is a genuine and well-supported case for treating travel as a non-negotiable financial priority rather than a discretionary luxury that waits until everything else is perfect. The experiential wellbeing research is consistent: holidays and meaningful experiences produce more lasting increases in happiness than most material purchases at equivalent cost. The memories, the perspective, the relationships reinforced or formed through shared travel — these are not trivial.There is also a compellingly practical argument against indefinitely deferring travel in favour of saving: time is the one resource that cannot be recovered or invested. A holiday with your children when they are young is not interchangeable with the same holiday when they are adults. A trip with ageing parents cannot be taken after they are gone. The desire to save 'until things are better financially' can become a permanent deferral if 'better financially' is never specifically defined.

The 24% of Americans who describe travel as 'an investment in themselves' (Empower 2025) and the 20% who 'prioritise travel regardless of what's going on in the economy' are not being financially irresponsible — they are expressing a clear values-based prioritisation that is entirely valid within a responsible budget. The key qualification is: prioritising travel within a budget is healthy; prioritising travel above a budget is the specific behaviour that creates the debt burden that makes everything else harder.

The Real Problem: How Most People Fund Their Holidays

The vacation-versus-saving debate is often framed as a values conflict when it is actually a mechanics problem. Most people who fall behind financially through travel are not making a considered values trade-off between experiences and savings. They are making the decision in the moment — booking the trip when the impulse is high, funding it with a credit card because the money is not available — and paying compound interest on the decision for months afterward.NerdWallet's April 2026 Summer Travel Survey documents the scale of this: 74% of 2025 summer travelers who paid for their vacation with a credit card did not pay off the balance immediately after returning. More than a third — 35% — still had not paid off last summer's vacation balance as of April 2026. This means that for these households, the 2026 summer vacation will begin before the 2025 one is paid for. The interest on last year's trip is funding this year's planning period.

IPX1031's April 2026 data adds a further dimension: 17% of Americans say they would go into debt specifically to pay for a vacation, and 1 in 10 plan to take on debt for travel in 2026, with the average amount being $2,525. At 22% credit card APR, $2,525 generates approximately $555 in annual interest — the equivalent of a flight, a weekend hotel, or most of a budget break. The holiday costs $2,525 plus $555 in interest for those who carry the balance. It costs $2,525 for those who saved for it first. The experience is identical. The financial outcome is not.

The Both/And Solution: The Vacation Sinking Fund

The solution to the vacation-versus-saving dilemma is not to choose one over the other. It is to change how you fund your travel — from reactive (book now, pay later) to intentional (save now, travel debt-free). The mechanism is the vacation sinking fund.A vacation sinking fund is a dedicated savings pot — separate from your emergency fund and main savings — specifically for travel. It is funded in small weekly or monthly amounts year-round, so that when a holiday booking opens, the money is already there. You spend it guilt-free because you saved it deliberately. You return home with zero new credit card debt related to the trip. The next saving cycle begins immediately.

CIT Bank's 2025 Summer Savings Survey captures the experience of this approach precisely: 'You spend months looking forward to the trip, then you can enjoy the experience knowing you're financially prepared. Afterward, you return home with memories that can last a lifetime.' The anticipation of a planned, funded trip is itself a source of wellbeing — you get the benefit of looking forward to the holiday for months, whereas an impulsive credit card booking produces anxiety about the bill alongside the anticipation of the trip.

How to Build Your Vacation Fund in Five Steps

The vacation sinking fund is one of the simplest savings mechanisms available — it requires a named account, an automatic transfer, and a trip to look forward to.Step 1: Name your fund and set the trip goal

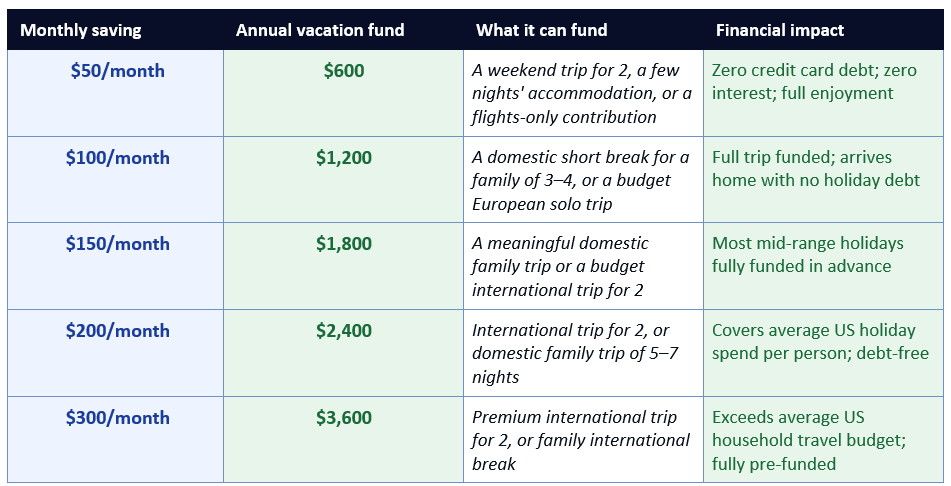

Open a separate savings account — or use a named pot in a banking app that supports this feature (Monzo and Starling in the UK; many US online banks including Ally, Marcus, and SoFi allow named savings goals within a single account). Name it specifically: 'Greece 2027,' 'Family Summer Break,' or 'Adventure Fund.' A specific name creates emotional connection to the goal and reduces the temptation to raid it for non-travel purposes.Step 2: Calculate the monthly saving required

Divide your target trip cost by the number of months until the trip. A $1,800 trip in 12 months requires $150 per month. A $2,400 trip in 18 months requires $133 per month. Include flights, accommodation, spending money, and a 10–15% buffer for unexpected costs. If the monthly figure is too high for your budget, adjust the trip scope, timeline, or use of travel rewards (see Section 9) rather than taking on debt.Step 3: Automate the transfer on payday

Set up an automatic transfer from your checking account to the vacation fund on the day you get paid — before the money is available for discretionary spending. This removes the monthly decision and makes the saving happen regardless of whether you remember or feel motivated. The fund accumulates silently in the background while you live your normal financial life.Step 4: Use a high-yield savings account

In 2026, the best easy-access savings accounts in the US pay up to 5.00% APY (Varo Money, as of May 2026). In the UK, easy-access rates reach up to 4.84% AER (Chip). A vacation fund growing at 4–5% while you accumulate it is earning interest on your holiday. $150 per month for 12 months at 5% APY accumulates to approximately $1,842 rather than $1,800 — the interest is modest but it points in the right direction.Step 5: Spend it guilt-free when the trip arrives

This is the most important step and the one most people find hardest: when the trip arrives and the money is there, spend it. The fund was created for this purpose. Spending pre-saved holiday money is not financial indulgence — it is financial success. You planned, you saved, you earned the trip. NerdWallet's Sara Rathner states it simply: 'The best vacation is one you can actually afford.' You can afford this one because you saved for it.Travelling Smarter: How to Spend Less Without Experiencing Less

The 58% of Americans who plan to spend less on travel in 2026 (Talker Research / CheapCaribbean, May 2026) do not have to experience less travel — they need to travel more efficiently. The cost reduction in travel budgets (down 23% on average) is possible without a proportional reduction in the quality of the travel experience, because the biggest cost drivers in travel are price-elastic in ways that the experience itself often is not.Eight ways to cut travel costs without cutting travel quality

- Fly on weekday non-peak times: NerdWallet's 2025 Holiday Spending Report found that 30% of cost-conscious travellers chose to fly on non-peak days. Tuesday and Wednesday outbound flights consistently cost 10–30% less than Friday or Sunday departures. The destination and experience are identical; the price is not.

- Book accommodation early or late: The sweet spot for accommodation pricing is either 6–8 weeks out (when availability is still broad and prices competitive) or 2–3 days before travel for last-minute deals on rooms that would otherwise go empty. Shoulder season travel (spring and autumn rather than peak summer or Christmas) consistently produces better value at equivalent quality.

- Use travel rewards strategically: 31% of 2026 travellers plan to use travel rewards points and miles to reduce costs (IPX1031, April 2026). A travel rewards credit card — paid in full every month — earns points on everyday spending (groceries, petrol, utilities) that can be redeemed for flights and hotels at effectively zero marginal cost. The key discipline is paying the balance in full monthly, so no interest offsets the rewards value.

- Embrace the staycation strategically: Nearly 30% of Americans plan to take at least one staycation in 2025/2026 (Empower survey). A well-planned staycation — treating your local area as a tourist would, staying in a nearby hotel, visiting attractions you have never prioritised despite living nearby — delivers genuine rest and new experience at 30–60% of the cost of domestic travel.

- Travel in a group for accommodation splits: A $200 per night Airbnb for four people costs $50 per person. The equivalent hotel rooms for each individual would cost $80–$120 per person. Group travel, when the logistics are manageable, produces per-person costs that make significantly better accommodation affordable for everyone.

- Cook some meals, eat out others: Choosing accommodation with a kitchen and buying local groceries for breakfasts and some dinners, while eating out for the meals that produce the most memorable experiences, can halve the food budget on a week-long trip without meaningfully reducing the experience of eating locally.

- Visit in the shoulder season: October in Europe, January in the Caribbean, April in Southeast Asia — shoulder season travel delivers lower prices on flights, accommodation, and activities, fewer crowds at major attractions, and frequently better weather than peak seasons imply. The 38% of Americans willing to travel 'closer to home due to cost' (IPX1031 2026) are applying this logic domestically.

- Set a 'per day' spending budget before departure: Knowing your daily spending target ($100, $150, $200 per day per person) before the trip creates a framework for real-time decisions. A daily budget that covers the average also creates the possibility of underspending on low-cost days and upgrading an experience on one special day without exceeding the total.

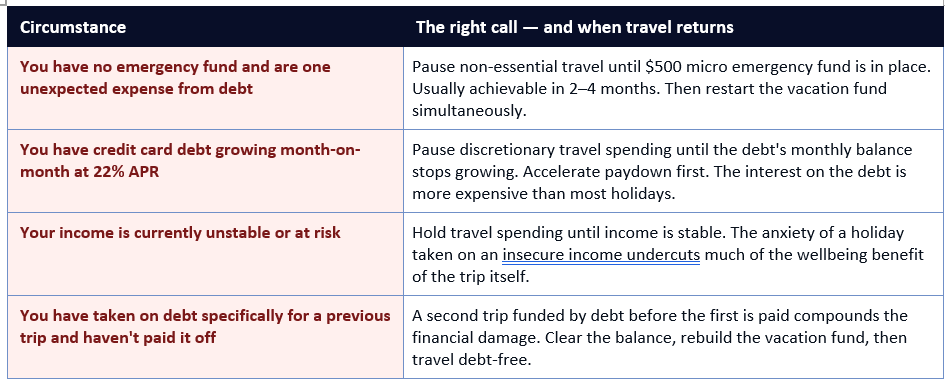

When Saving Must Come Before Travel

There are specific financial circumstances in which the honest answer to 'vacation or saving?' is 'saving, for now.' Understanding these circumstances is not defeatist — it is the clarity that makes the future holiday genuinely joyful rather than tinged with financial anxiety.In all other circumstances — stable income, emergency fund in place, no actively growing credit card debt — a planned, sinking-fund-financed holiday is a financially sound and personally valid priority.

The Travel Rewards Approach: Funding Holidays Through Everyday Spending

Travel rewards credit cards represent one of the few ways to genuinely reduce the financial cost of travel — not by spending less, but by converting spending you would make anyway into travel value. The 31% of 2026 travellers using points and miles (IPX1031, April 2026) and the 25% of 2025 holiday travellers using points for at least some travel costs (NerdWallet 2025) are accessing a meaningful cost reduction with zero additional spending required.The mechanism is straightforward: a travel rewards card earns points on everyday purchases — groceries, petrol, utilities, dining — and those points can be redeemed for flights, hotel nights, and travel-related costs. A card earning 2 to 3 points per pound or dollar on spending produces approximately 2 to 3% of spend in travel value. On $3,000 of monthly household spending, that is $60 to $90 per month in travel value — $720 to $1,080 per year — at zero additional cost beyond what would be spent anyway.

The non-negotiable condition for travel rewards cards is paying the balance in full every month. A card balance at 22% APR eliminates the rewards value entirely and then some — a $1,000 in rewards earned on $50,000 of annual spending is worth nothing if the card accrues $500 in interest. Travel rewards cards are a genuine wealth tool only for people who use them as a payment method for budgeted spending rather than as a means of spending beyond their budget. NerdWallet's Sara Rathner notes: 'While it can be tempting to hoard rewards for a major trip, points and miles can lose value over time, so it's a good idea to use them as you need them.'

CONCLUSION

The choice between going on vacation and saving is a false binary. The real question is not whether to travel, but how to fund the travel you want in a way that leaves you financially ahead rather than behind when you return. Forty-nine per cent of Americans prioritise travel in their budgets, and 30% are saving specifically for vacations in 2026. They are right to do so. Travel is a legitimate, evidence-backed investment in wellbeing. The 17% who would go into debt for it and the 35% still paying for last summer's holiday are not wrong to want the trip — they are just using the most expensive possible funding mechanism.The vacation sinking fund changes the answer from 'vacation OR saving' to 'vacation AND saving.' $100 to $200 per month, automated into a named travel account, produces $1,200 to $2,400 per year of guilt-free travel money — enough for most of the holidays that most people want. Combine it with a travel rewards card paid in full monthly, smart booking timing, and the cost-saving strategies in this guide, and the best vacation you can actually afford is likely better than you think it is. Save for it first. Spend it without guilt. Return home financially whole.

Frequently Asked Questions

Is it financially responsible to prioritise holidays over saving?

Yes — when travel is funded through a dedicated sinking fund rather than through debt, it is entirely financially responsible. IPX1031's April 2026 survey found that 71% of Americans are actively budgeting for their 2026 travel, and Motley Fool's November 2025 Financial Resolutions Report found that saving for travel is the single most common savings goal for 2026. The problem is not travel as a priority — it is travel funded by credit card debt that creates a financial cost multiplier. A holiday that costs $1,800 in cash costs $1,800. The same holiday on a credit card at 22% APR costs $1,800 plus compound interest for however many months it takes to pay off, which NerdWallet's April 2026 data shows is still ongoing for 35% of people who used a card for last summer's trip.How much should I save per month for holidays?

The right figure depends entirely on the trip you want and the time you have to save. The formula is: total estimated trip cost divided by months until departure. A $1,200 trip in 12 months requires $100 per month. A $2,400 trip in 18 months requires $133 per month. Include flights, accommodation, food, activities, and a 10–15% buffer. IPX1031's April 2026 data found that among Americans who plan to take on travel debt in 2026, the average amount is $2,525 — which is achievable as a 12-month sinking fund at approximately $210 per month, or an 18-month sinking fund at approximately $140 per month. At either rate, the trip is funded in advance and no interest is paid. The monthly saving should be automated and set up on a payday-aligned schedule so it happens before discretionary spending.Should I go on holiday if I have credit card debt?

This depends on the state of the debt. If the credit card debt is being actively reduced month-on-month and your balance is falling, a modest, well-planned, cash-funded holiday can be compatible with responsible debt management — particularly if travel is a strong personal value and the amount is modest relative to income. If the credit card balance is growing month-on-month (meaning you are spending more than you earn), taking on additional travel spending worsens an already deteriorating situation. The specific circumstances that argue for postponing travel are: growing credit card debt, no emergency fund, unstable income, or a situation where previous travel debt has not been paid. In all other cases, a planned and pre-saved trip is financially sound.What is the best way to save for a holiday without affecting my other financial goals?

The most effective approach is treating the vacation fund as a parallel savings stream rather than a competing one — separate from both your emergency fund and your long-term savings/investment contributions. Open a named, dedicated savings account (or a named pot in a banking app). Set the automatic transfer amount to something achievable without affecting your emergency fund, debt payments, or pension/retirement contributions. The sequence is: emergency fund and employer pension match first, then all other savings goals simultaneously including the vacation fund. Even $50 per month into a vacation fund is $600 per year — a meaningful contribution to travel — without touching any other financial priority. The 2026 US best HYSA rates of up to 5.00% APY (Varo) mean the vacation fund earns interest while accumulating.How can I afford a good holiday on a tight budget?

The cost of a meaningful holiday is significantly more compressible than most people assume without meaningfully reducing the quality of the experience. Talker Research's May 2026 CheapCaribbean survey found that 70% of Americans who are being financially cautious are still travelling — they have reduced budgets by 23% on average, not to zero. The most effective strategies are: flying on weekday non-peak days (saves 10–30% on flights), travelling in the shoulder season (saves 20–40% on accommodation), choosing accommodation with cooking facilities (reduces food costs by 30–50%), using travel rewards points and miles on a card paid in full (converts existing spending into travel value at no extra cost), and planning with a specific daily budget per person before departure. The Empower 2025 survey found that 82% of cost-conscious travellers use cost-saving strategies without forgoing travel — and 44% still describe their holiday memories as priceless.References

IPX1031 — Americans Travel Report 2026: Plans, Budgets, and AI Use (April 2026) https://www.ipx1031.com/americans-travel-report-2026/NerdWallet — 2026 Summer Travel Report: How Americans Plan and Pay (April 2026) https://www.nerdwallet.com/travel/studies/summer-travel-report

Talker Research / Hotel News Resource — Americans Focus on Value as Travel Spending Drops for 2026 (May 2026) https://www.hotelnewsresource.com/article141186.html

Motley Fool Money — Top Financial New Year's Resolutions for 2026 (November 2025) https://www.fool.com/the-ascent/research/financial-new-years-resolutions

CIT Bank / Barchart — Young Americans Saving for Bigger Vacations: CIT Bank 2025 Summer Savings Survey (August 2025) https://www.barchart.com/story/news/33921306/young-americans-are-planning-and-saving-for-bigger-vacations-this-summer-new-cit-bank-survey-finds

Empower — Travel Spending Trends Research: Half of Americans Say Vacation Memories Are Priceless (2025) https://www.empower.com/the-currency/play/travel-spending-trends-research

NerdWallet — 2025 Holiday Spending Report: How Americans Pay for Holiday Travel https://www.nerdwallet.com/credit-cards/studies/holiday-spending-report

0 Comments Comments