Taxes

What Is Income Tax and National Insurance in the UK?

Table of Contents

- Two Taxes, One Payslip

- What Is Income Tax?

- Income Tax and NI Rates Combined: 2026/27 Full Reference

- What Is National Insurance?

- The State Pension and Qualifying Years

- National Insurance Classes: Who Pays What

- Employer National Insurance: The Tax You Never See on Your Payslip

- Scotland: Different Income Tax, Same National Insurance

- How PAYE Works: From Gross Pay to Your Take-Home

- Worked Example: £40,000 Salary (England, 2026/27)

- Fiscal Drag: How the Threshold Freeze Increases Your Tax Without Changing Rates

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Two Taxes, One Payslip

Most UK employees see two separate deductions from their pay before a penny reaches their bank account: income tax and National Insurance Contributions (NICs). These are not the same thing, they are calculated differently, they serve different stated purposes, and the rates and thresholds that govern each behave differently as income rises. Yet for most people, they appear side by side on a payslip as two numbers that together determine how large the gap between gross pay and take-home pay actually is.Understanding how both work — what rates apply at each income level, what the combined burden is across the salary spectrum, what National Insurance actually builds toward compared to income tax, and how the frozen thresholds of 2026/27 are gradually pulling more workers into higher tax bands — is genuinely useful financial knowledge. It affects decisions about salary sacrifice, pension contributions, overtime, secondary employment, and how earnings from self-employment compare to employment.

For the 2026/27 tax year (6 April 2026 to 5 April 2027), the headline rates are unchanged from 2025/26: the personal allowance remains at £12,570, the basic rate of income tax remains at 20%, the higher rate at 40%, and employee National Insurance at 8% in the main band and 2% above the upper earnings limit. But the freeze on these thresholds — legislated to continue until 2030/31 — means that as wages grow, the real tax burden quietly increases without any rate change. This effect, called fiscal drag, is reshaping the tax position of millions of UK workers. This guide explains everything — the rates, the mechanics, the employer side, the Scotland difference, and what NI actually earns you.

What Is Income Tax?

Income tax is the principal direct tax levied by the UK government on an individual's income. It applies to employment income, self-employment profits, pension income, rental income, savings interest (above the personal savings allowance), and dividend income (above the £500 dividend allowance). It is calculated on taxable income — the total income above the personal allowance and any other deductions such as pension contributions.The UK income tax system is progressive — different rates apply to different slices of income, not to your total income at the highest rate you reach. If you earn £60,000, you do not pay 40% on all of it. You pay 0% on the first £12,570, 20% on the next £37,700 (from £12,571 to £50,270), and 40% only on the remaining £9,730. This is the most important and most frequently misunderstood feature of the UK tax system. The words 'I'm a higher rate taxpayer' do not mean 40% of all earnings goes to HMRC — only the portion above £50,270 is taxed at 40%.

For employees, income tax is collected through the Pay As You Earn (PAYE) system. Your employer deducts the correct amount from each pay packet based on your tax code and pays it directly to HMRC. Your tax code — typically 1257L for the standard 2026/27 tax year — tells your employer how much of your income to treat as tax-free before applying the relevant rate. PAYE operates cumulatively across the year, so if you overpay early in the tax year (due to an irregular pay pattern or a new job starting mid-year), the system corrects itself over subsequent pay periods.

Fiscal drag: the silent tax rise: Thresholds frozen at 2021/22 levels until 2030/31 — real tax burden rises without any rate change — the personal allowance has been fixed at £12,570 since 2021/22 and the higher rate threshold at £50,270 since the same year. With UK wages growing at 3-5% per year, more workers cross the higher rate threshold each year without any change in nominal tax rates. The House of Commons Library (June 2026) confirms all thresholds are unchanged for 2026/27 and due to remain frozen through 2030/31.

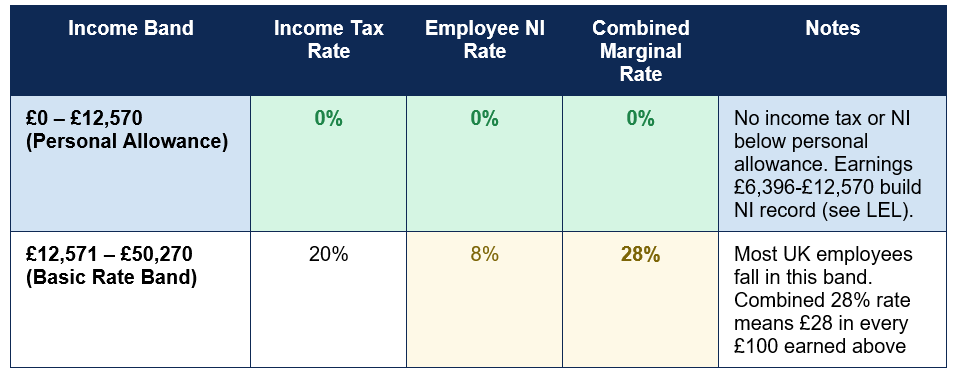

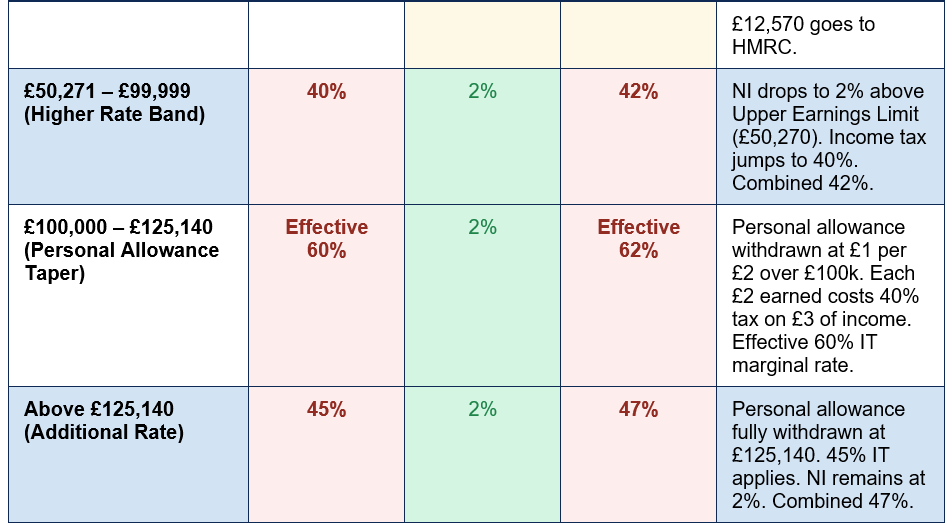

Income Tax and NI Rates Combined: 2026/27 Full Reference

The table below maps the complete income tax and employee National Insurance framework for England, Wales, and Northern Ireland in 2026/27. Scotland uses different income tax bands and rates — see the Scotland section below for details. The combined marginal rate column shows the true cost of each additional pound of employment income at each band:

What Is National Insurance?

National Insurance Contributions (NICs) are described as a social insurance system — contributions you make during your working life that fund your entitlement to the State Pension, Maternity Allowance, Bereavement Support Payment, and certain other contributory benefits including the contribution-based element of Jobseeker's Allowance. In this sense, NI differs from income tax: it is the only UK tax from which paying directly earns you a defined long-term entitlement. You cannot earn State Pension entitlement by paying income tax; you earn it only by accumulating qualifying years through NI contributions or NI credits.In practice, however, NI operates as a second income tax in cash-flow terms. The receipts go into general government revenue, not into a personal ring-fenced account. UKTaxDrag's 2026/27 NI guide is direct about this: 'National Insurance is presented as a contributory social-insurance system but in cash-flow terms behaves identically to a hypothecated income tax.' The contributory entitlement is real and valuable — but the mechanism is revenue collection, identical in practice to income tax.

The key practical differences from income tax are: NI only applies to earned income (wages, self-employment profits) and not to savings interest, dividends, rental income, or pension payments — meaning higher earners with investment income can have a low effective NI rate; NI is calculated per pay period (non-cumulative), not cumulatively across the year like income tax; and the rates change at thresholds that do not precisely match the income tax bands, creating a complex combined rate structure.

The State Pension and Qualifying Years

The full new State Pension in 2026/27 is £12,547.60 per year, indexed annually by the Triple Lock (the highest of inflation, earnings growth, or 2.5%). To receive the full amount, you need 35 qualifying years of NI contributions or NI credits. Each missing year reduces the pension by 1/35th — approximately £342 per year for life, or around £6,840 over a typical 20-year retirement.Qualifying years are built through employment (Class 1 NI), self-employment (Class 2 or Class 4), voluntary contributions (Class 3), and NI credits (awarded automatically for certain circumstances including claiming Child Benefit, being on Universal Credit, or being a carer). You can check your NI record and State Pension forecast at gov.uk/check-national-insurance-record and fill gaps by paying voluntary Class 3 contributions at £18.40 per week in 2026/27 — a rate that the PocketWise NI guide describes as one of the best-value financial decisions available to anyone with gaps in their record.

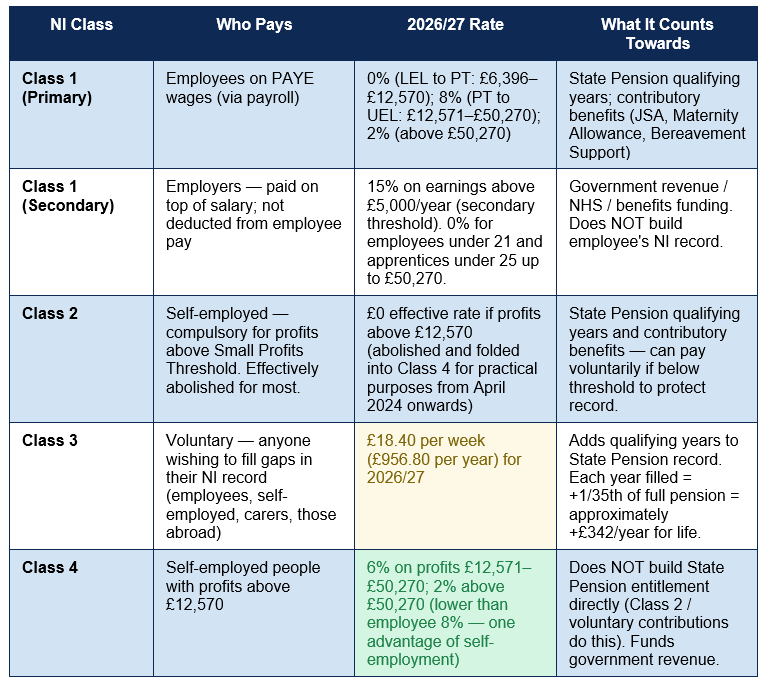

National Insurance Classes: Who Pays What

National Insurance is divided into different classes depending on your employment status and income level. The table below covers every class relevant to 2026/27:

The most underused financial tool in the UK: Voluntary Class 3 NI contributions. At £18.40 per week (£956.80 per year) in 2026/27, you can purchase additional qualifying years toward your State Pension at a defined, guaranteed rate. Each year purchased adds approximately £342 to your annual State Pension — a return of approximately 36% per year from the day you claim. For anyone with gaps in their NI record — years spent caring for children, living abroad, in lower-paid work below the Lower Earnings Limit, or not working — checking and filling these gaps through Class 3 is often the highest-return financial decision available. Check your record at gov.uk/check-national-insurance-record before State Pension age.

Employer National Insurance: The Tax You Never See on Your Payslip

Employer National Insurance — Class 1 Secondary contributions — is paid by employers on top of your salary and does not appear on your payslip as a deduction from your pay. It is an employment cost that sits between your gross salary and what your employer actually pays to employ you. For 2026/27, the employer NI rate is 15% on all earnings above the secondary threshold of £5,000 per year (approximately £417 per month or £96 per week).The employer NI rate increased significantly in October 2024 following Chancellor Rachel Reeves's 2024 Autumn Budget — rising from 13.8% to 15%, while the secondary threshold was simultaneously cut from £9,100 per year to £5,000 per year. The combined effect of both changes represents a substantial increase in the cost of employment for UK businesses. EmployersCalculator's June 2026 analysis notes: 'The 2026/27 tax year continues the significant changes to employer National Insurance introduced in April 2025. The employer NI rate remains at 15%, and the Secondary Threshold stays at £5,000 per year.'

While employer NI does not reduce your take-home pay directly, it matters for employees in three ways. First, for salary discussions — your employer's total cost of employing you is your gross salary plus employer NI, meaning a £40,000 salary costs approximately £44,650 to the employer. Second, for salary sacrifice pension contributions — contributions made under salary sacrifice reduce your gross salary and therefore reduce the employer NI bill, which is why many employers share part of the NI saving with employees as additional pension contributions. Third, for the self-employed — someone moving from employment to self-employment escapes employer NI entirely, which is one of the genuine financial advantages of self-employment that affects total economic cost even if it does not show in personal income.

The Employment Allowance remains at £10,500 in 2026/27, with the previous £100,000 NI liability cap for eligibility completely removed. This means most small employers can offset their first £10,500 of employer NI liability against this allowance — making it one of the most valuable reliefs available to small businesses employing staff.

Scotland: Different Income Tax, Same National Insurance

Scottish taxpayers pay the Scottish Rate of Income Tax (SRIT) set by the Scottish Parliament, which has diverged significantly from the rest of the UK in recent years. For 2026/27, Scotland has six income tax bands compared with England and Wales's three, with a more graduated structure:- Starter rate: 19% on income from £12,571 to £16,538

- Basic rate: 20% on income from £16,539 to £29,527

- Intermediate rate: 21% on income from £29,528 to £43,662

- Higher rate: 42% on income from £43,663 to £75,000

- Advanced rate: 45% on income from £75,001 to £125,140

- Top rate: 48% on income above £125,140

Scottish taxpayers pay more income tax than equivalent earners in England, Wales, and Northern Ireland at most income levels above approximately £28,000. The Scottish Government's position is that this funds additional public services including free prescriptions and enhanced childcare. National Insurance rates and thresholds are identical across all four nations — NI is reserved to the UK Parliament and cannot be varied by devolved governments.

SCOTTISH TAXPAYERS AND GIFT AID: Despite paying higher Scottish income tax rates (e.g. 42% higher rate vs 40% in England), Gift Aid is still calculated and reclaimed at the UK basic rate of 20% by charities — the same mechanism applies everywhere. Scottish higher-rate taxpayers (41-48%) claim the difference between their Scottish rate and the 20% basic rate through their Scottish Self Assessment return. The mechanism is the same but the personal reclaim can be larger given higher Scottish marginal rates.

How PAYE Works: From Gross Pay to Your Take-Home

PAYE — Pay As You Earn — is the system through which employers deduct income tax and employee NI from wages and pay them directly to HMRC on your behalf. For most UK employees, PAYE means you never need to file a tax return — your tax is calculated, deducted, and paid automatically. Understanding the mechanics helps you verify your payslip and identify if something looks wrong.Your tax code is the key instruction your employer receives from HMRC. The standard 2026/27 code for most employees is 1257L — the L suffix means standard personal allowance, and the number (1257) means your employer will treat your first £12,570 as tax-free. If your code is different — for example, a lower number like 900L — it may mean HMRC has reduced your allowance to collect a previous underpayment, or you have taxable benefits in kind. If your code is higher than 1257L, it may mean HMRC has added additional tax relief (such as professional subscriptions) to your code. Your current tax code appears on your payslip and can be checked at gov.uk/check-income-tax.

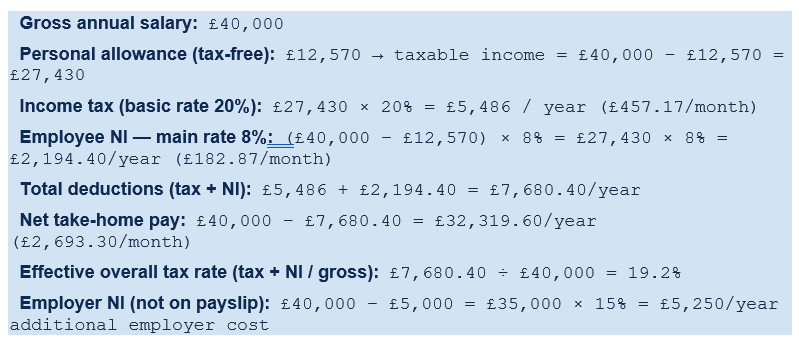

Worked Example: £40,000 Salary (England, 2026/27)

The following example calculates the income tax and employee NI deductions for a full-time employee in England earning £40,000 gross per year in 2026/27, with no salary sacrifice or other adjustments:

This example illustrates the combined impact of income tax and NI for a typical earner, and shows that the effective overall rate (19.2%) is considerably lower than the headline basic rate (20%) because the personal allowance and NI thresholds mean a significant portion of earnings are taxed at 0%.

Fiscal Drag: How the Threshold Freeze Increases Your Tax Without Changing Rates

Fiscal drag is the process by which frozen tax thresholds, combined with wage growth, gradually increase the real tax burden on workers without any nominal change in tax rates. When the personal allowance was first set at £12,570 in 2021/22, it represented a meaningful proportion of average earnings. As average earnings have grown by several percentage points each year since, the real value of the personal allowance has eroded — a larger share of each worker's income now falls into taxable bands.The effect is most visible at the higher rate threshold. In 2021/22, a worker needed to earn more than £50,270 to pay any higher rate tax. That threshold has not moved since. As wages have grown, a growing number of UK workers whose real living standard has barely improved find themselves paying 40% income tax — and 42% combined — on their earnings above £50,270. The Moorepay 2026 analysis of tax changes notes this directly: 'the continued freeze on income tax and NI thresholds meaning that more employees will gradually move into higher tax bands as wages rise — a key driver of fiscal drag.'

For individual workers, the practical implications of fiscal drag are: regularly checking whether you have crossed the higher rate threshold and are now entitled to claim higher-rate pension relief and Gift Aid higher-rate refunds through Self Assessment; considering salary sacrifice pension contributions to reduce taxable income below key thresholds; and being aware that a pay rise that appears to bring you into the 40% band may be partially offset by claiming all relevant reliefs.

Conclusion

Income tax and National Insurance are the two pillars of the UK's direct tax system for individuals, together accounting for the majority of the gap between what most workers earn and what they take home. For 2026/27, the rates and thresholds are unchanged from 2025/26: income tax at 0%, 20%, 40%, and 45% across successive bands; employee NI at 0%, 8%, and 2%; a personal allowance of £12,570 and higher rate threshold of £50,270, both frozen until 2030/31. The combined marginal rate in the basic band (£12,571-£50,270) is 28%; in the higher rate band it is 42%; in the personal allowance taper zone (£100,000-£125,140), it reaches an effective 62%.National Insurance is not simply a second income tax, though it operates like one in cash-flow terms. It is the mechanism through which you build State Pension qualifying years and entitlement to contributory benefits. The full new State Pension of £12,547.60 per year requires 35 qualifying years — gaps in your NI record can be filled through voluntary Class 3 contributions at £18.40 per week in 2026/27, one of the highest-return financial decisions available to those with incomplete records. Employer NI, invisible on your payslip but real to your employer, rose to 15% with a £5,000 secondary threshold in October 2024 — a change that affects salary negotiation, salary sacrifice economics, and the total cost of employment.

The freeze on thresholds until 2030/31 means that fiscal drag will continue to pull more UK workers into higher tax bands through wage growth alone, without any change in headline rates. For workers approaching or crossing the £50,270 higher rate threshold, the most financially important actions in 2026/27 are: claiming all higher-rate tax relief through Self Assessment, using salary sacrifice to reduce taxable income where possible, and checking the NI record to ensure State Pension entitlement is complete. This guide provides the foundation for all of those decisions.

Frequently Asked Questions (FAQ)

What are the UK income tax rates and bands for 2026/27?

For England, Wales, and Northern Ireland in 2026/27, income tax is charged at: 0% on the first £12,570 (personal allowance); 20% on income from £12,571 to £50,270 (basic rate); 40% on income from £50,271 to £125,140 (higher rate); and 45% on income above £125,140 (additional rate). Between £100,000 and £125,140, the personal allowance is withdrawn at £1 per £2 of income above £100,000, creating an effective marginal income tax rate of 60% in this range. Scotland has different rates and bands including a 42% higher rate (compared with England's 40%) and a 48% top rate. All thresholds have been frozen since 2021/22 and are due to remain frozen until 2030/31.How much National Insurance do I pay as an employee in 2026/27?

As an employee, you pay no NI on earnings below £12,570 per year (the primary threshold, aligned with the personal allowance). On earnings from £12,571 to £50,270, you pay 8% NI. On earnings above £50,270 (the upper earnings limit), the rate falls to 2%. For a full-time employee earning £35,000, employee NI costs approximately £1,794 per year — around £149 per month. The 8% rate is the result of two consecutive cuts from 12%: a reduction to 10% in January 2024 and to 8% in April 2024. These cuts are unchanged for 2026/27. NI is calculated per pay period, not cumulatively across the year — which can have implications if you receive a large one-off payment.What does National Insurance actually pay for?

National Insurance funds your State Pension entitlement and entitlement to certain contributory benefits including Jobseeker's Allowance (contribution-based), Maternity Allowance, and Bereavement Support Payment. The full new State Pension in 2026/27 is £12,547.60 per year, and requires 35 qualifying years of NI contributions or NI credits. Each qualifying year you are missing reduces your State Pension by approximately £342 per year — a gap that can be filled by paying voluntary Class 3 NI contributions (£18.40 per week in 2026/27). NI receipts go into general government revenue alongside income tax and are not held in a personal account, but the contributory entitlement (the qualifying year count) is genuine and tracked through your NI record.What is fiscal drag and how does it affect me?

Fiscal drag is the effect of frozen tax thresholds combined with wage growth. In the UK, the personal allowance (£12,570) and the higher rate threshold (£50,270) have been frozen since 2021/22 and are due to remain at these levels until 2030/31. As wages grow each year, a larger proportion of each worker's income falls into taxable bands — and more workers cross the higher rate threshold — without any change in the nominal tax rates. This is a real increase in tax burden achieved without a rate rise. For individual workers, the most immediate practical consequence is that annual pay rises now include a growing tax component. Workers who cross the £50,270 higher rate threshold should register for Self Assessment to claim higher-rate pension and Gift Aid relief they become newly entitled to.Do I pay the same income tax in Scotland as in England?

No. Scottish taxpayers pay the Scottish Rate of Income Tax set by the Scottish Parliament, which has six bands compared with England's three. For 2026/27, Scottish rates include a starter rate of 19%, basic rate of 20%, intermediate rate of 21%, higher rate of 42% (versus 40% in England), advanced rate of 45%, and top rate of 48% (versus 45% in England). Most Scottish taxpayers earning above approximately £28,000 pay more income tax than equivalent earners in England. National Insurance rates and thresholds are identical across all four UK nations — NI cannot be varied by the Scottish Parliament. Residents of Wales and Northern Ireland pay the same income tax as England and Northern Ireland — Wales currently mirrors England's rates.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. House of Commons Library — Direct Taxes: Rates and Allowances for 2026/27 (June 2026)

https://commonslibrary.parliament.uk/research-briefings/cbp-10618/

2. GOV.UK — Rates and Thresholds for Employers 2026 to 2027 (Official HMRC)

https://www.gov.uk/guidance/rates-and-thresholds-for-employers-2026-to-2027

3. PocketWise — National Insurance Rates 2026/27: Complete UK Guide (March 2026)

https://pocketwise.co.uk/tax/national-insurance-rates-2026-27/

4. UKTaxDrag — UK National Insurance Complete Guide 2026/27 (May 2026)

https://uktaxdrag.co.uk/uk-national-insurance-guide-2026-27

5. Deloitte / Taxscape — UK Tax Rates 2026/27 (Autumn Budget 2025 Edition)

https://taxscape.deloitte.com/taxtables/deloitte-uk-tax-rates-2026-27.pdf

6. Moorepay — Tax and National Insurance Changes 2026-27 (March 2026)

https://www.moorepay.co.uk/payroll-hr-rates/tax-and-national-insurance-changes/

7. GOV.UK — Check Your National Insurance Record and State Pension Forecast

https://www.gov.uk/check-national-insurance-record

8. GOV.UK — Income Tax: Personal Allowances and Reliefs

https://www.gov.uk/income-tax-rates

0 Comments Comments