Insurance

What Is Over 65 Travel Insurance? Complete Guide

Table of Contents

- Why Travel Insurance Changes at 65

- What Is Over 65 Travel Insurance?

- How Over 65 Travel Insurance Differs From Standard Cover

- What Over 65 Travel Insurance Covers

- Emergency Medical Expenses

- Repatriation

- Trip Cancellation and Curtailment

- Pre-Existing Medical Condition Cover

- What Over 65 Travel Insurance Costs in 2026

- Providers With No Upper Age Limit: Who to Consider in 2026

- Declaring Pre-Existing Medical Conditions: Everything You Need to Know

- Conditions That Typically Need Specialist Insurance

- Annual vs Single-Trip Over 65 Travel Insurance: Which Is Right for You?

- How to Find the Best Over 65 Travel Insurance Policy

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why Travel Insurance Changes at 65

Age 65 is the threshold at which UK travel insurance changes character. Below it, most mainstream insurers compete fiercely for your business, comparison sites return dozens of competitive quotes, and premiums are relatively modest. Above it, the market narrows, premiums rise, pre-existing medical conditions become the central underwriting question, and the difference between the right policy and the wrong one can be the difference between a manageable medical claim and a £25,000 evacuation bill that you have to fund yourself.This narrowing of the market is not arbitrary. According to Which?'s May 2026 analysis of 144 annual and single-trip policies, a traveller shopping for cover on their 60th birthday can access 94% of annual policies available. By their 80th birthday, their age alone bars them from more than eight in ten annual policies reviewed. Over-75s pay an average of 65% more than 65 to 74 year-olds for equivalent cover. And yet the demand for travel from this demographic has never been higher: ABTA data shows Britons over 70 took an estimated 8.2 million overseas trips in 2025, and AARP's survey found 86% of Americans aged 50 or older named travel as one of their top three priorities for discretionary income in 2026.

This guide explains exactly what over 65 travel insurance is, how it differs from standard cover, what it costs at different ages and health profiles, which providers offer no upper age limit policies, how pre-existing medical conditions are handled and declared, what specialist cover such as cruise and repatriation insurance involves, and the step-by-step process for finding the best policy for your specific circumstances in 2026. Whether you are planning a European city break at 67 or a long-haul adventure at 81, there is cover available — the key is knowing where to look and what to look for.

What Is Over 65 Travel Insurance?

Over 65 travel insurance is not a single, legally defined product — it is a term for the specialised travel insurance market that serves UK travellers aged 65 and above, where standard mainstream policies increasingly impose age restrictions, require more detailed medical declarations, or become uneconomical due to age-related premium loadings. The cover itself — medical expenses, trip cancellation, baggage, personal liability, and travel delays — is structurally the same as for younger travellers. What differs is the underwriting approach, the premium level, the availability of certain products, and the emphasis placed on the medical coverage component.For UK travellers aged 65 and over, travel insurance matters more, not less, than it did at 45. The cost of medical treatment abroad escalates with age, not only because older travellers are statistically more likely to need treatment but because the treatment required is frequently more complex and more expensive. A hip fracture following a fall, a cardiac event, a stroke, or a diabetic crisis in a destination where English-speaking medical care is limited can generate medical bills of tens of thousands of pounds, plus repatriation costs. Medical evacuation from a European destination can exceed £25,000 according to UtterlyCovered's 2026 guide — a cost no GHIC (Global Health Insurance Card) fully covers, and one that makes adequate travel insurance a financial necessity rather than an optional extra.

How Over 65 Travel Insurance Differs From Standard Cover

The practical differences between over-65 travel insurance and standard policies are significant. MoneySuperMarket's May 2026 data confirms several key distinctions that become more pronounced as age increases:- Reduced policy availability: As noted by Which?, at 80 your age alone restricts access to more than 80% of annual travel policies. Single-trip policies remain more widely available — the average age limit for single-trip policies is 89, compared with 76 for annual policies.

- Higher premiums: Over-65s pay more for equivalent cover, with the premium loading increasing sharply at 75 and again at 80. Over-75s pay an average of 65% more than 65-74 year olds for the same level of cover.

- Shorter maximum trip durations: Some annual policies reduce the maximum duration of individual trips for older policyholders. Where a policy might allow 45 days per trip for customers under 65, the same policy may limit over-65 customers to 31 days, or over-75 customers to 17-21 days. Always check the maximum single trip length before purchasing an annual policy.

- Reduced personal accident cover: Some policies reduce the lump-sum payable under personal accident cover for older policyholders, reflecting actuarial differences in life expectancy and earning capacity. This is less relevant than medical cover for most senior travellers, but worth noting.

- Mandatory pre-existing condition declaration: While all travellers must declare pre-existing conditions, the screening process becomes more intensive and the premium loading more significant with age. Many standard mainstream insurers will exclude specific conditions entirely for older travellers rather than loading the premium.

What Over 65 Travel Insurance Covers

A comprehensive over-65 travel insurance policy in 2026 covers the same core categories as any UK travel insurance policy, though the limits and the medical coverage emphasis differ:Emergency Medical Expenses

This is the most critical component for older travellers and should receive the most scrutiny when comparing policies. Medical cover limits for over-65 specialist policies in 2026 typically range from £5 million to £20 million for European travel, with Forbes Advisor UK's top-rated policy for a 65-year-old couple (Southdowns) providing £20 million in medical cover. For the USA and Canada — where healthcare costs can reach thousands of dollars per day — you need a minimum of £5 million cover, and many specialists recommend £10 million or more for North American destinations. Emergency medical cover should explicitly include: hospitalisation, surgery, prescribed medication, specialist consultations, and ambulance transport.Repatriation

Repatriation — the cost of returning you to the UK following a medical emergency, either on a commercial flight with a medical escort or on a dedicated air ambulance — is a specific benefit within the emergency medical cover section of most policies. It is one of the most expensive claims that can be made on a travel policy: air ambulance repatriation from a European destination can cost £25,000 to £50,000 or more, and from a long-haul destination, significantly more. Always confirm that your policy's medical cover limit is sufficient to include repatriation and that the policy does not separate repatriation into a lower sub-limit.Trip Cancellation and Curtailment

Covers the cost of a trip that you have to cancel before departure or cut short after departure, due to unforeseen circumstances — illness, injury, bereavement, or other listed events. For over-65 travellers, the cancellation benefit is particularly important because the statistical likelihood of a health-related cancellation increases with age. Standard cancellation limits for over-65 policies range from £1,500 to £5,000 per person, with some premium policies offering up to £10,000 or more.Pre-Existing Medical Condition Cover

This is the most complex and most variable element of over-65 travel insurance. A pre-existing condition is any illness, injury, or medical condition for which you have received treatment, taken medication, or sought medical advice in the period prior to the policy start date (typically the last 12 to 24 months, though some policies look further back). All pre-existing conditions must be declared honestly — failure to disclose a known condition can invalidate your entire policy, not just the claim related to that condition.Not all conditions trigger a premium loading. Mild, well-controlled conditions — mild asthma managed with a standard inhaler, well-controlled type 2 diabetes — are accepted by most specialist insurers with modest or no loading. More serious conditions — heart disease, previous cancer (particularly if still under treatment), recent stroke, unstable chronic conditions — require specialist insurers and will attract significant premium loadings. In some cases, an insurer will cover your trip but exclude the specific condition — providing cover for everything except a claim arising from the pre-existing condition. Understanding whether a condition is covered, excluded, or covered with a loading is the most important question to ask when comparing over-65 travel insurance.

The GHIC is not the same as travel insurance: Many UK travellers over 65 hold a GHIC (Global Health Insurance Card) and assume it provides adequate medical cover abroad. It does not. The GHIC entitles you to the same state-funded healthcare that local residents receive in EU countries — which in some countries is basic, in others is more comprehensive, but in all cases excludes repatriation, excludes most private hospital treatment, and provides no coverage at all outside the EU or in countries such as the USA, Canada, or Australia. For any travel outside the UK, comprehensive travel insurance is essential regardless of GHIC status.

What Over 65 Travel Insurance Costs in 2026

Premiums for over-65 travel insurance in 2026 vary significantly by age band, pre-existing condition profile, destination, and policy type. The table below provides indicative premium ranges based on MoneySuperMarket May 2026 data, UtterlyCovered's 2026 research, Forbes Advisor UK's market survey, and SpokenClue's 2026 cost guide:

The USA premium penalty: US/Canada cover typically doubles or trebles European premiums — American healthcare costs are the primary driver — a day in a US hospital can cost $2,000-$10,000 or more, making a week's hospitalisation a $50,000+ claim even before surgery or repatriation. Over-65 travellers heading to the USA need a policy with at least £5 million in medical cover, and many specialists recommend £10 million (UtterlyCovered 2026).

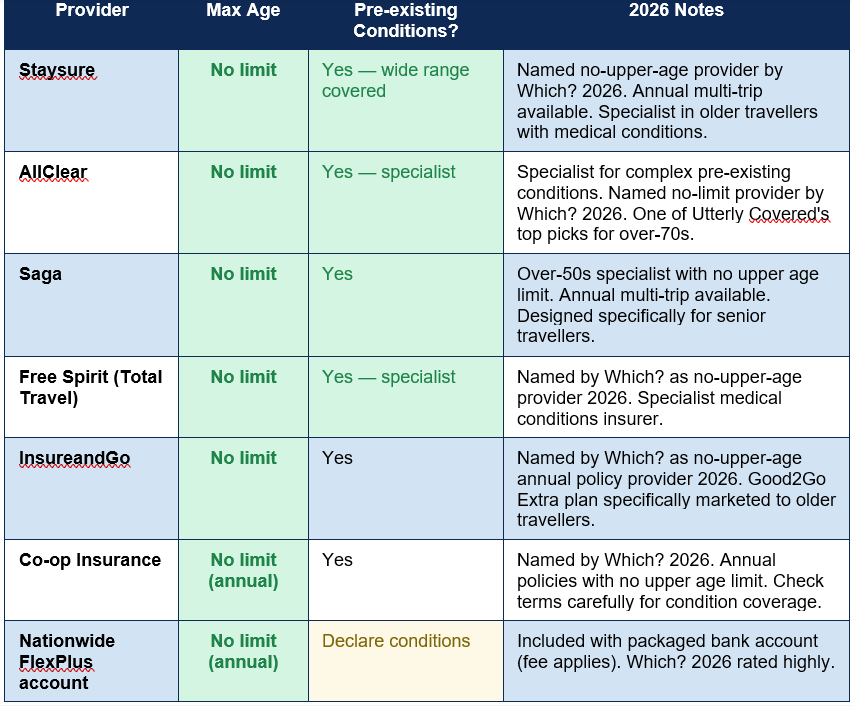

Providers With No Upper Age Limit: Who to Consider in 2026

Which?'s 2026 survey of 48 travel insurance firms found a specific group that offer annual policies with no maximum age for new customers. The table below maps the key providers, their pre-existing condition coverage, and their distinguishing features for 2026:

ALWAYS DO THIS: When comparing over-65 policies, get quotes from at least three specialist providers in addition to any mainstream comparison sites. Many specialist insurers — including Staysure, AllClear, and Free Spirit — do not appear on standard comparison sites, or return better rates when quoted directly. The British Insurance Brokers' Association (BIBA) helpline on 0370 950 1790 can refer you to a specialist broker if online searching proves difficult.

Declaring Pre-Existing Medical Conditions: Everything You Need to Know

Declaring pre-existing conditions honestly and completely is the single most important action any traveller takes when buying travel insurance — and the consequences of non-disclosure are severe enough to warrant treating this with absolute seriousness. If you fail to declare a condition that your insurer would have considered relevant, and you subsequently need to make a claim (whether or not it is related to the undisclosed condition), the insurer may reject the claim entirely and cancel the policy. This is not a technicality — it happens, and it leaves travellers stranded in foreign countries with no cover.The standard definition of a pre-existing condition for UK travel insurance purposes includes any medical condition for which you have received treatment, taken prescribed medication, had medical tests or investigations, been referred to a specialist, or experienced symptoms in the period defined by the policy (typically the past 12 to 24 months). When you complete the medical screening section of an over-65 travel insurance application, you will typically be asked a series of questions about specific conditions and your recent medical history. Answer every question as accurately and completely as possible.

If your condition is declined by mainstream insurers or quoted at a premium you consider prohibitive, several specialist routes remain available. MoneyHelper's Travel Insurance Directory lists providers that specifically cover high-risk conditions. The British Insurance Brokers' Association can connect you with a specialist broker. And some specialist insurers — particularly AllClear and Free Spirit — are specifically designed for travellers with complex or serious medical histories who have been turned down elsewhere.

Conditions That Typically Need Specialist Insurance

- Active or recent cancer (particularly if receiving chemotherapy or radiotherapy at time of travel)

- Cardiac conditions: heart disease, previous heart attack, heart failure, recent cardiac surgery

- Stroke or TIA (transient ischaemic attack) within the past 12 months

- COPD or severe respiratory conditions

- Kidney disease requiring dialysis

- Unstable diabetes or diabetes with complications

- Recent major surgery (within the past 3-6 months, depending on the insurer)

Annual vs Single-Trip Over 65 Travel Insurance: Which Is Right for You?

The choice between an annual multi-trip policy and individual single-trip policies is primarily a financial calculation, but for over-65 travellers the policy availability dimension adds complexity. Annual policies become harder to find above age 75, meaning that for frequent travellers in their late 70s and 80s, single-trip policies may be the only option regardless of preference.Annual policies make financial sense when you take two or more trips per year and all of your trips fall within the maximum single-trip duration allowed by the policy for your age bracket. The annual premium typically equates to approximately two to three single-trip premiums, so two or more trips in the year tip the economics in favour of annual cover. For travellers aged 65-74 with no significant pre-existing conditions who travel regularly, annual policies from Staysure, Saga, or InsureandGo typically represent excellent value.

Single-trip policies are the better choice if you travel only once or twice a year, if your trip duration exceeds the maximum individual trip limit on annual policies for your age, or if you are in an age bracket or health profile where annual policy availability is limited. MoneySuperMarket's May 2026 data tracks premiums across age bands for both policy types — using their comparison tool for both annual and single-trip options before making a decision is always worthwhile.

CRUISING NEEDS SPECIFIC COVER: Standard travel insurance may not fully cover the unique risks of cruise travel — medical emergencies at sea, cabin confinement due to illness, missed port departures, and emergency helicopter evacuation to shore. If you are taking a cruise, specifically ask your insurer about cruise cover or purchase a policy that includes it explicitly. Cruise-specific policies often have higher age limits than standard policies and are designed for exactly the kind of traveller who frequently cruises: older, experienced, and requiring comprehensive medical cover.

How to Find the Best Over 65 Travel Insurance Policy

Finding the right over-65 travel insurance requires a more methodical approach than comparing standard policies, because the market is more fragmented and the relevant criteria more complex. The following step-by-step process is recommended:- Start with specialist comparison sites: Comparison sites that specifically cater to senior travellers and pre-existing conditions — including Medical Travel Compared (medicaltravelcompared.co.uk), AllClear, and Staysure's own comparison tool — often return a better set of results for over-65s than general comparison sites where age caps may filter out your options before you see the results.

- Use general comparison sites as well: MoneySuperMarket, Compare the Market, and GoCompare all provide over-65 quotes. Run searches on these in addition to specialist sites — some mainstream insurers offer competitive over-65 rates that do not appear on specialist platforms.

- Quote directly with no-upper-age-limit providers: Staysure, AllClear, Saga, Free Spirit, and InsureandGo all offer direct quotes without age cutoffs. Quote directly with each in addition to comparison site results.

- Declare all conditions completely in the medical screening: Do not skip or minimise the medical screening section. Complete it fully for every provider. Premium differences between providers for the same condition profile can be substantial — one insurer may load your premium significantly for managed hypertension while another includes it at no additional cost.

- Compare on medical cover limit, not just price: The cheapest policy is not always the best policy. For over-65 travellers, the medical cover limit is the most important single number in the policy. A policy with £5 million medical cover costs less than one with £20 million, but the difference matters enormously if you need extended hospitalisation and repatriation from a serious illness.

- Check the single-trip duration limit for your specific age: Annual policies often reduce the maximum single-trip duration for older policyholders. If your planned trip exceeds the limit for your age bracket, the annual policy will not cover you for that trip regardless of the overall annual policy being active.

Conclusion

Over 65 travel insurance in 2026 is more expensive than standard cover, more complex to compare, and more important than ever. Britons over 70 took 8.2 million overseas trips in 2025. Premiums rise sharply at age 75 — by an average of 65% compared to the 65-74 bracket — and the availability of annual policies narrows from 94% of the market at age 60 to less than 20% at age 80. Medical evacuation from a European destination can cost £25,000 or more, and the GHIC does not cover repatriation, private treatment, or travel outside the EU. For every traveller over 65, comprehensive travel insurance is not a nice-to-have — it is the financial protection that makes travel possible.The good news is that the market, while narrower, does exist — and for travellers who approach it correctly, excellent cover is available at every age. Staysure, AllClear, Saga, Free Spirit, and InsureandGo all offer annual policies with no upper age limit. Specialist comparison sites and the MoneyHelper Travel Insurance Directory provide routes to cover even for those with complex medical histories. Declaring pre-existing conditions completely and accurately is essential — non-disclosure risks invalidating an entire policy, not just a single claim. And comparing medical cover limits, not just premiums, is the most important discipline any senior traveller can bring to the buying process.

Travel in later life should be expansive, not constrained. The right travel insurance is the foundation that makes every trip from a European city break to a long-haul adventure financially secure. Take the time to find it properly — and then go.

Frequently Asked Questions (FAQ)

Why does travel insurance cost more once I turn 65?

Travel insurance costs more for over-65s because insurers assess higher statistical likelihood of a claim and higher average claim costs. Older travellers are more likely to need medical treatment abroad, more likely to need emergency repatriation, and more likely to cancel a trip due to health-related issues. Insurers price these increased risks into premiums. The cost increase is not uniform — a fit, healthy 65-year-old with no pre-existing conditions pays significantly less than someone of the same age managing multiple chronic conditions. Over-75s pay on average 65% more than 65-74 year olds for equivalent cover, reflecting a further statistical increase in claim likelihood and cost at this age bracket.What does 'no upper age limit' mean for travel insurance?

A 'no upper age limit' policy is one where the insurer will provide a quote and offer coverage to new customers regardless of how old they are. Which?'s 2026 survey found eight providers that explicitly confirmed no maximum age for annual policy new customers: AllClear, Co-op Insurance, Free Spirit, InsureandGo, Just Travel Cover (Good2Go Extra), Nationwide, Saga, and Staysure. In practice, even these providers will conduct medical screening that may affect eligibility or premium for older travellers with significant health conditions. 'No upper age limit' means age alone is not the barrier — but health conditions and trip characteristics are still assessed.Do I need to declare pre-existing medical conditions?

Yes, always — and completely. Every pre-existing condition must be declared to your travel insurer as part of the medical screening process. A pre-existing condition is any illness, injury, or medical issue for which you have received treatment, taken medication, or sought medical advice, typically within the past 12 to 24 months. Failing to disclose a condition that your insurer would consider relevant is non-disclosure, which can invalidate your entire travel policy — not just a claim related to the undisclosed condition. If your conditions result in a declined quote or an unaffordable premium from mainstream insurers, use the MoneyHelper Travel Insurance Directory or contact the British Insurance Brokers' Association for specialist providers who specifically cover complex medical histories.Is my GHIC (Global Health Insurance Card) enough coverage for trips abroad?

No. The GHIC entitles you to the same state-funded healthcare that local residents receive in EU countries — which varies enormously in quality and accessibility depending on the destination. It does not cover: emergency repatriation to the UK; private hospital treatment; medical treatment outside EU countries (including the USA, Canada, Australia, and most long-haul destinations); or any of the other standard travel insurance benefits such as trip cancellation, baggage loss, or personal liability. The GHIC should be carried alongside travel insurance, not instead of it. For travellers over 65, the gap between what the GHIC covers and what comprehensive travel insurance covers is particularly significant given the higher statistical likelihood of needing medical treatment.How much medical cover do I need on an over-65 travel insurance policy?

For European travel, a minimum of £5 million in emergency medical cover is recommended, with £10 million or more preferable — particularly for older travellers or those with pre-existing conditions where treatment could be extended and complex. For the USA, Canada, or other destinations with high healthcare costs, a minimum of £5 million is necessary, and many specialists recommend £10 million or more given that a single day in an American hospital can cost thousands of dollars and emergency surgery plus repatriation can reach six figures. Forbes Advisor UK's top-rated policies for over-65s as of 2026 all provide £15 million to £20 million in medical cover. Never choose a policy primarily on price if doing so means accepting a medical cover limit below these recommendations.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Which? — Best Travel Insurance for Over-65s 2026 (Survey of 48 providers, May 2026)

https://www.which.co.uk/money/insurance/travel-insurance/how-to-find-travel-insurance-if-you-are-over-65-aYAee5Q4mQhB

2. Forbes Advisor UK — Best Travel Insurance for Seniors Over 65 in 2026

https://www.forbes.com/advisor/uk/travel-insurance/seniors/

3. MoneySuperMarket — Compare Travel Insurance for Over 65s (May 2026 data)

https://www.moneysupermarket.com/travel-insurance/over-65s/

4. UtterlyCovered — Best Travel Insurance for Over 70s UK 2026 (March 2026)

https://utterlycovered.com/resources/best-travel-insurance-for-over-70s-uk-2026

5. MoneyHelper — Travel Insurance for Over 65s and Medical Conditions

https://www.moneyhelper.org.uk/en/everyday-money/insurance/travel-insurance-for-over-65s-and-medical-conditions

6. Medical Travel Compared — Compare Over 60s Travel Insurance (Updated July 2026)

https://www.medicaltravelcompared.co.uk/travel-insurance/over-60/

7. British Insurance Brokers' Association (BIBA) — Find a Specialist Travel Insurance Broker

https://www.biba.org.uk/find-insurance/

8. NHS — Get a UK Global Health Insurance Card (GHIC)

https://www.nhs.uk/using-the-nhs/healthcare-abroad/apply-for-a-free-uk-global-health-insurance-card-ghic/

0 Comments Comments