Credits

Accountant Explains Best Balance Transfer Credit Cards in the US & UK

Table of Contents

- The Case for Balance Transfers Has Never Been Stronger

- How Balance Transfers Work: The Complete Mechanism

- Best UK Balance Transfer Credit Cards: July 2026

- Best US Balance Transfer Credit Cards: July 2026

- Calculating the True Cost: Fee vs No Fee, Long vs Short

- UK Worked Example: £5,000 Balance

- US Worked Example: $5,000 Balance

- The Rules for Using a Balance Transfer Card Successfully

- How to Choose the Right Balance Transfer Card for Your Situation

- Balance Transfer vs Personal Loan: Which Is Right for You?

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Case for Balance Transfers Has Never Been Stronger

Credit card debt is expensive. In the UK, MoneyfactsCompare data shows the average APR across credit cards has reached 35.8% — a 20-year high. In the United States, average credit card interest rates remain elevated following the Federal Reserve's rate cycle, with most standard cards charging between 20% and 30%. Against this backdrop, a balance transfer credit card — which allows you to move existing high-interest debt to a new card charging 0% interest for a defined period — is one of the most financially impactful tools available to consumers on both sides of the Atlantic.The numbers confirm that this is a widespread problem. CreditCards.com's 2026 analysis found that 72% of Americans with credit card debt added to it in the past year, and that many are stuck in cycles of minimum payments that barely touch the principal while interest compounds. In the UK, Compare the Market data shows the average balance people want to transfer stands at £5,373. At 35.8% APR, that balance accumulates approximately £1,923 in interest in just one year. Moving it to a 36-month 0% balance transfer card and making regular monthly payments means clearing the debt with zero additional interest — a saving of £1,923 in year one alone, and more in subsequent years.

This guide covers how balance transfer cards work, the best deals available in both the UK and the US as of July 2026, how to calculate the true cost comparison between fee-bearing and fee-free options, the strict rules you must follow to avoid losing the 0% deal, and how to choose between the wide range of options — from guaranteed 36-month UK deals to US cards that bundle rewards alongside the debt-clearing intro period. Whether you are carrying £2,000 or £20,000 in credit card debt, there is a balance transfer strategy in this guide that addresses your situation.

How Balance Transfers Work: The Complete Mechanism

A balance transfer is a process by which you move outstanding debt from one or more existing credit cards to a new credit card that charges either 0% or a lower interest rate for a defined introductory period. The mechanism works as follows:- Apply for a balance transfer card: You apply for a new credit card that offers a 0% balance transfer introductory period. The application results in a credit check. If approved, you receive a credit limit on the new card.

- Request the transfer within the window: Most UK and US balance transfer cards require you to initiate the transfer within a specific number of days of opening the account — typically 60 to 90 days in the UK, and 60 to 120 days in the US depending on the card. If you miss this window, you lose the 0% promotional rate on the transferred balance.

- Your new provider pays off your old card: The new card issuer pays the balance on your old card directly. You now owe the money to the new provider, not the old one. Your old card balance drops to zero.

- The transferred balance sits at 0% for the introductory period: During the 0% period, no interest accrues on the transferred balance. Every payment you make goes directly toward reducing the principal. This is fundamentally different from paying on a card at 35.8% APR, where a significant portion of every payment covers interest rather than the debt itself.

- You pay a one-time balance transfer fee: Most balance transfer cards charge a fee of 3% to 5% (UK typically 3%-3.5%; US typically 3%-5%) on the amount transferred at the point of transfer. This is the cost of accessing the 0% period. Some cards offer fee-free transfers for shorter periods — in the UK, Barclaycard currently offers a 14-month fee-free option.

- The 0% period ends and the standard APR applies: When the introductory period expires, any remaining balance starts accruing interest at the card's standard APR — typically 24.9% in the UK, and 16%-28% in the US. If you have cleared the full balance by this date, you pay nothing. If any balance remains, the interest meter starts immediately.

The interest saving in real terms: £5,373 average BT amount × 35.8% APR = £1,923 interest in year one — versus £0 on a 0% BT card — Compare the Market data (July 2026) shows the average UK balance people want to transfer is £5,373. At the UK average APR of 35.8%, this costs approximately £1,923 in interest annually — money that goes entirely to interest, not toward clearing the debt. A 0% balance transfer stops the meter entirely (Compare the Market July 2026 / MoneyfactsCompare).

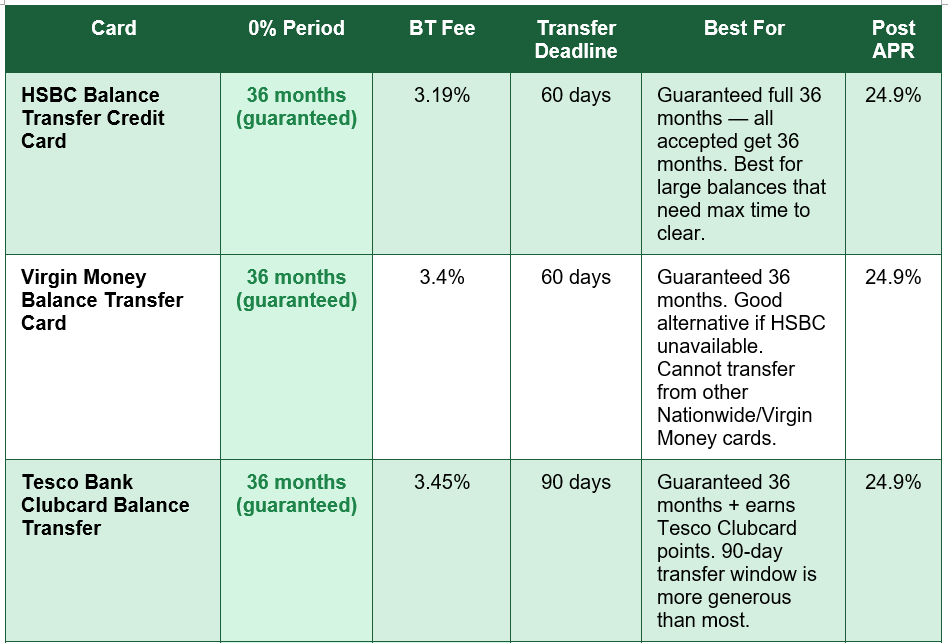

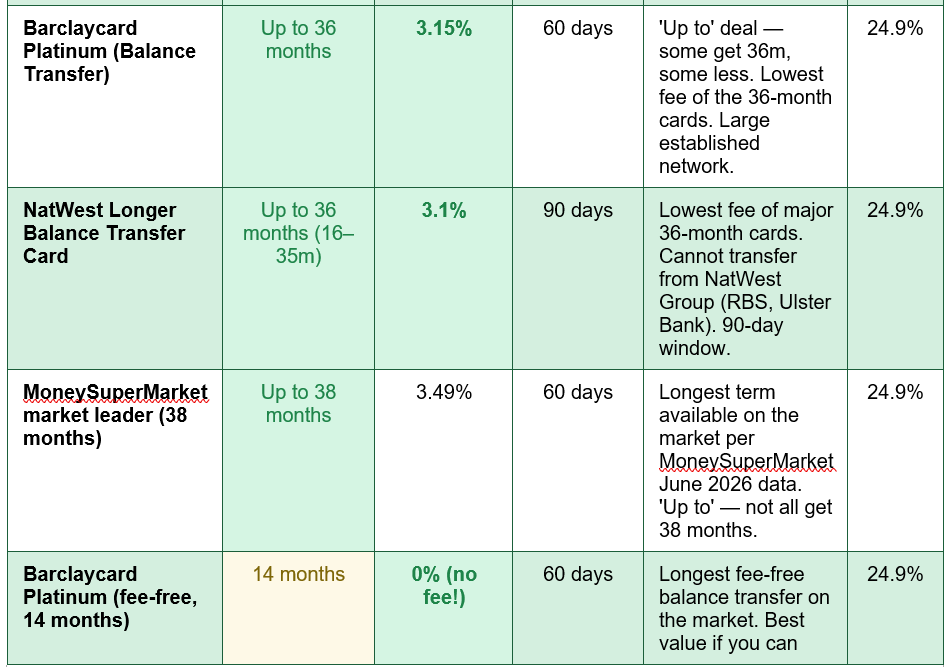

Best UK Balance Transfer Credit Cards: July 2026

The table below covers the best UK balance transfer credit cards as of July 2026, ranked by 0% period length, with transfer fees, windows, and key notes. Data sourced from MoneySuperMarket (data correct 6 July 2026), Uswitch (updated 2 weeks ago), Forbes Advisor UK (1 week ago), and GoodMoneyGuide (June 2026):

Guaranteed vs 'up to' balance transfer periods in the UK: Several of the longest 0% balance transfer periods are advertised as 'up to' a number of months — meaning not all accepted applicants receive the headline figure. You might receive 36 months, or you might receive 20 months, depending on your creditworthiness. HSBC, Virgin Money, and Tesco Bank all currently offer guaranteed 36-month periods — every accepted applicant gets the full 36 months. Barclaycard and NatWest are 'up to' deals. For applicants who prioritise certainty over length, the guaranteed 36-month cards from HSBC, Virgin, and Tesco eliminate the guesswork. For those with strong credit scores who want the lowest fee, NatWest's 3.1% fee is the cheapest among the major 36-month options.

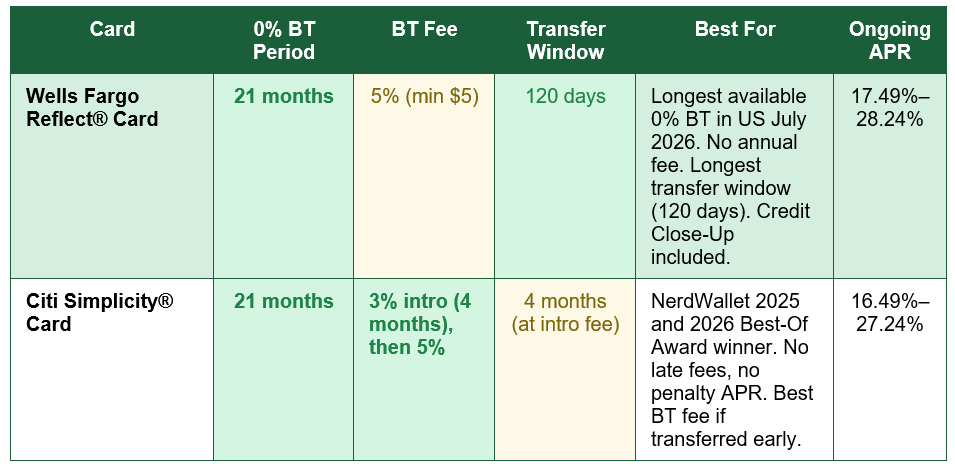

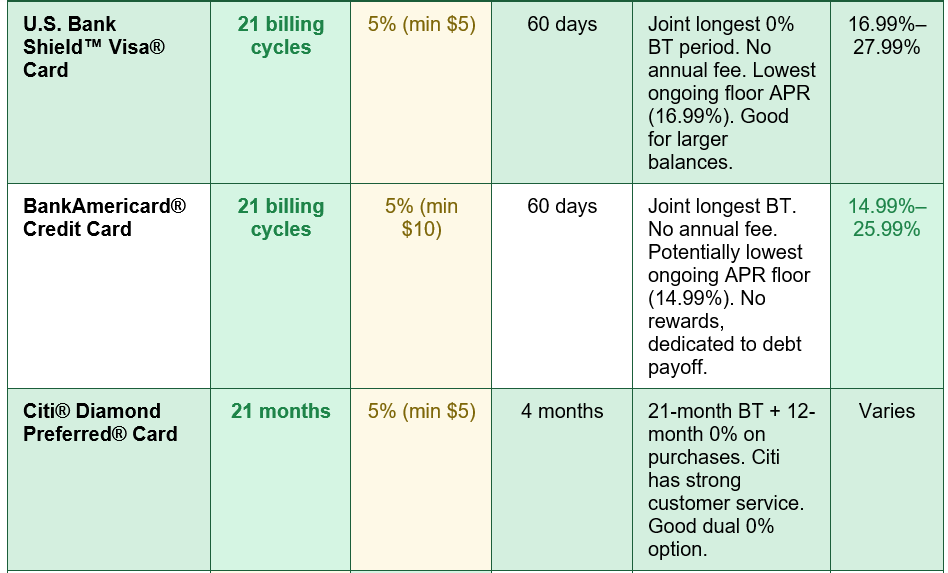

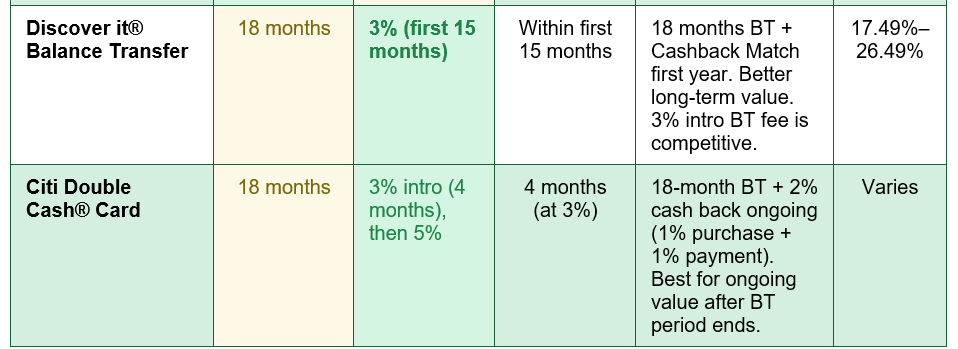

Best US Balance Transfer Credit Cards: July 2026

In the United States, the best balance transfer cards as of July 2026 offer introductory 0% APR periods of up to 21 months — significantly shorter than the UK market but still representing a meaningful window for debt repayment. CreditCards.com's July 2026 analysis of over 1,000 balance transfer cards identified the following top picks, also cross-referenced with NerdWallet, Bankrate, and CreditKarma July 2026 rankings:

US vs UK: A STARK DIFFERENCE IN MARKET DEPTH: The UK balance transfer market offers significantly longer 0% periods (up to 38 months) than the US (capped at 21 months), reflecting different regulatory environments and competitive dynamics. UK cards are also more commonly structured as pure debt management tools with post-0% APRs clustered around 24.9%. US cards more frequently bundle rewards — Citi Double Cash's 2% cash back, Discover it's Cashback Match — making some a better long-term proposition beyond the intro period. If you need more than 21 months to clear your balance, the UK market is structurally more favourable. If you value ongoing rewards alongside debt management, several US options provide both.

Calculating the True Cost: Fee vs No Fee, Long vs Short

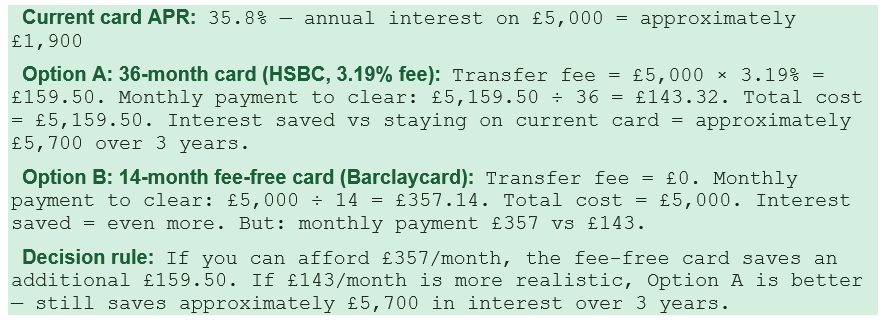

One of the most common mistakes made when choosing a balance transfer card is focusing exclusively on the length of the 0% period without calculating the total cost. The balance transfer fee, the length of period, and how quickly you can realistically clear the balance all interact to determine the true best option for your specific debt.UK Worked Example: £5,000 Balance

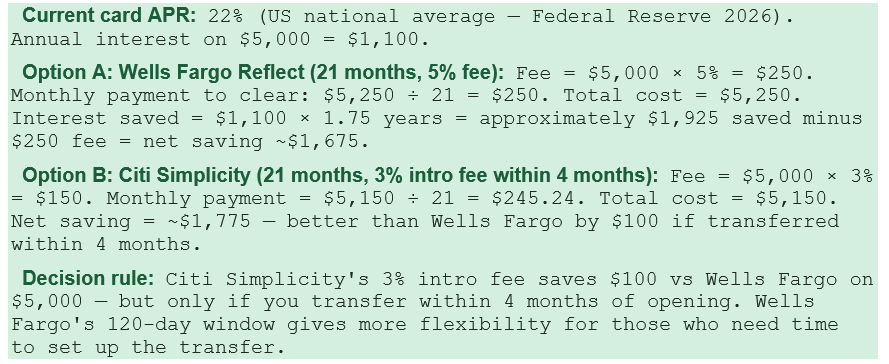

US Worked Example: $5,000 Balance

The Rules for Using a Balance Transfer Card Successfully

Balance transfer cards can save hundreds or thousands in interest — or they can leave you worse off if used carelessly. Every major consumer finance authority including MoneySavingExpert, NerdWallet, Which?, and Bankrate emphasises the same essential rules:- Transfer within the promotional window: The 0% rate only applies to balances transferred within the card's specified window — 60 to 120 days depending on the card. If you miss this window, the balance transfers at the standard APR, not the promotional rate. Complete the transfer as soon as possible after the card is approved.

- Never miss a minimum monthly payment: Missing even a single minimum payment typically triggers immediate loss of the 0% promotional rate, reverting the entire balance to the standard APR. Set up a direct debit for the minimum payment immediately upon receiving the card — not as a future task. Set it up the same day you activate the card.

- Pay more than the minimum — calculate what you actually need: The minimum payment keeps the 0% deal alive but will not clear the balance before the promotional period ends. Divide your total transferred balance by the number of months in the 0% period. This is the monthly payment you need to make. Set up a direct debit or standing order for this amount.

- Do not use the card for new purchases unless they are also 0%: Most balance transfer cards charge the standard APR on new purchases immediately — they are not covered by the 0% promotional rate unless the card explicitly offers 0% on both transfers and spending. Using a balance transfer card for everyday spending while trying to clear your transferred balance defeats the purpose.

- Set a calendar alert one month before the 0% period ends: If any balance remains as the 0% period approaches its end, you need either to clear it in full or to apply for another 0% balance transfer card to carry the remaining balance forward. Give yourself at least one month's notice to arrange this without pressure.

- You cannot transfer between cards in the same banking group: A balance on a Barclaycard cannot be transferred to another Barclaycard. A NatWest credit card balance cannot be transferred to RBS (also in the NatWest Group). A Virgin Money balance cannot go to another Nationwide Group card. Check the banking group of both the old and new card before applying.

THE REVERT TRAP — the most expensive outcome: If you have any remaining balance when the 0% period expires, it immediately accrues interest at the card's standard APR — typically 24.9% in the UK or 16%-28% in the US. On a £2,000 remaining balance at 24.9%, this means £498 per year in new interest charges — ironically, on a card you opened specifically to stop paying interest. The solution is simple: mark the expiry date as a calendar event 30 days before it arrives. If you cannot clear the remaining balance in time, apply for a new 0% balance transfer card before the old one expires and transfer the remaining balance. Chain your 0% periods together rather than letting the rate revert.

How to Choose the Right Balance Transfer Card for Your Situation

The best balance transfer card is not the one with the longest 0% period — it is the one that matches your debt amount, your realistic monthly repayment capacity, and your credit profile. The following framework maps common situations to the appropriate choice:- You have a large balance (UK £5,000+) and need maximum time to clear it: A guaranteed 36-month card from HSBC (3.19%), Virgin Money (3.4%), or Tesco Bank (3.45%) provides the certainty of the full period at fees that represent a fraction of the interest you would otherwise pay. The fee on £5,000 is £159-£172 — versus potentially £5,700+ in interest over 3 years.

- You have a small-to-medium balance (UK under £3,000) and can clear it in 14 months: The Barclaycard fee-free 14-month option saves the transfer fee entirely — worth £60-£90 on a £2,000 balance. If your monthly repayment capacity is sufficient, this is the highest-return option on a smaller balance.

- You want the longest possible 0% period available anywhere in the UK: The MoneySuperMarket market-leading 38-month deal (3.49% fee) — check the current provider via MoneySuperMarket's comparison tool as providers change — offers the maximum runway. Use their eligibility checker before applying.

- You are in the US and want the longest 0% window with the lowest fee: Citi Simplicity is NerdWallet's 2025 and 2026 Best-Of Award winner — it offers 21 months at 0% with a 3% intro balance transfer fee (versus 5% after 4 months), no late fees, and no penalty APR. For those who transfer within the 4-month introductory fee window, it is the lowest-cost 21-month option.

- You want ongoing rewards after the balance transfer period ends: US: Citi Double Cash (2% cash back ongoing) or Discover it Balance Transfer (Cashback Match first year) combine 18-month BT periods with genuine long-term value. UK: Tesco Bank's Clubcard BT card earns Clubcard points alongside the 36-month 0% period — useful for existing Tesco shoppers.

Balance Transfer vs Personal Loan: Which Is Right for You?

A balance transfer card is not always the best way to consolidate credit card debt — for some borrowers and some debt levels, a personal loan offers comparable or better value, and it is important to understand when each approach is optimal.A 0% balance transfer card is better than a personal loan when: the balance transfer fee is less than the interest you would pay on a personal loan; you can realistically clear the full balance within the 0% period; and your credit score qualifies you for competitive balance transfer offers. For UK borrowers, a 36-month 0% card with a 3.19% fee on £5,000 costs £159.50 total — substantially less than most personal loan products on the same amount over the same period, even at competitive loan rates.

A personal loan may be better than a balance transfer when: your debt is very large and the balance transfer fee would be significant; you want a fixed monthly payment over a fixed term with no risk of the rate reverting; you cannot realistically clear the balance within any available 0% period; or your credit score does not qualify you for the best 0% deals but does qualify for a competitive personal loan rate. For amounts above approximately £10,000, the balance transfer fee (3-3.5% = £300-£350) begins to approach the cost of a competitive 2-3 year personal loan, and a direct comparison becomes worthwhile.

Conclusion

Balance transfer credit cards are one of the most powerful debt management tools available to consumers in both the UK and the US — and in July 2026, the deals available represent some of the best in recent memory. In the UK, HSBC, Virgin Money, and Tesco Bank all offer guaranteed 36-month 0% balance transfer periods, meaning every accepted applicant gets the full three years to clear their debt without a penny of interest on the transferred balance. The MoneySuperMarket market-leading deal reaches 38 months. At the UK average APR of 35.8%, clearing a £5,373 average transfer balance over 36 months at 0% saves over £5,700 in interest compared with staying on the original card. The balance transfer fee of 3.1%-3.49% is the entire cost of that saving.In the US, Wells Fargo Reflect, Citi Simplicity, U.S. Bank Shield, and BankAmericard all offer 21-month introductory 0% APR periods — the longest available in the American market. The 72% of US cardholders who added to their credit card debt in the past year are paying an average rate that makes even the standard 5% balance transfer fee look like excellent value. Citi Simplicity's 3% introductory fee (within 4 months) and no-late-fee structure earned it NerdWallet's Best-Of Award in both 2025 and 2026. For US borrowers who can clear their balance within 18 months, Discover it Balance Transfer and Citi Double Cash offer additional cash back rewards alongside the 0% intro period.

The rules that make balance transfers work are simple and consistent across both markets: transfer within the specified window, set up a minimum payment direct debit immediately, calculate and pay the monthly amount to clear the balance in time, keep a calendar alert for the 0% expiry date, and never use the card for new purchases unless they are also 0%. A balance transfer card used according to these rules is one of the most cost-effective ways to escape from credit card debt in 2026. A balance transfer card ignored or mismanaged ends up adding another annual fee or penalty charge to an already difficult situation. The discipline is simple; the saving is substantial.

Frequently Asked Questions (FAQ)

What is the longest 0% balance transfer deal in the UK in July 2026?

The longest 0% balance transfer period currently available in the UK is up to 38 months according to MoneySuperMarket's data correct to 6 July 2026 (3.49% fee). Among guaranteed deals where every accepted applicant receives the full period, HSBC Balance Transfer, Virgin Money, and Tesco Bank Clubcard Balance Transfer all offer 36 guaranteed months at fees of 3.19%, 3.4%, and 3.45% respectively. Barclaycard Platinum and NatWest both offer up to 36 months but are 'up to' deals where some applicants receive shorter periods. The longest fee-free balance transfer is Barclaycard Platinum's 14-month offer, where no balance transfer fee applies at all.How much does a balance transfer cost?

A balance transfer typically costs a one-time fee charged as a percentage of the amount transferred. In the UK, fees on the longest 0% deals range from 3.1% (NatWest) to 3.49% (market-leading 38-month deal). On a £5,000 balance, this equates to £155 to £174.50. Some cards — Barclaycard's 14-month deal in the UK — charge no fee at all, though the 0% period is shorter. In the US, balance transfer fees typically range from 3% to 5%. Citi Simplicity charges 3% if transferred within the first 4 months of account opening (then 5%). Wells Fargo Reflect and BankAmericard charge 5% from the start. On a $5,000 balance, the difference between 3% and 5% is $100.Can I transfer a balance between cards from the same bank?

No — balance transfers between cards from the same banking group are not permitted. In the UK, you cannot transfer from a Barclaycard to another Barclaycard, from a NatWest card to an RBS card (both in the NatWest Group), or from a Virgin Money card to another Nationwide Group card. In the US, you cannot transfer balances between cards from the same issuer. This rule prevents banks from simply shuffling debt internally. Always verify the banking group of both your existing card and the new balance transfer card before applying — if they share a parent company, the transfer will not be permitted regardless of what promotional offers are available.What happens to my old credit card after a balance transfer?

After a balance transfer, your old credit card's balance drops to zero. The card remains open and active — unless you specifically request to close it. Keeping the old card open but unused can actually help your credit score by maintaining your overall available credit limit, which keeps your credit utilisation ratio lower. However, if the old card has an annual fee, closing it after the transfer makes financial sense. Do not use the old card to accumulate new spending after the transfer — the entire point of the balance transfer is to have a single balance on the new 0% card and a clear repayment plan. Accumulating new balances on the old card while clearing the transferred balance adds complexity and can undermine the debt reduction strategy.What is the best balance transfer card in the US in July 2026?

For the longest 0% period in the US, Wells Fargo Reflect, Citi Simplicity, U.S. Bank Shield, and BankAmericard all offer 21 months — the joint longest available in the American market as of July 2026. For the best combination of period and lowest fee, Citi Simplicity stands out: it offers 21 months at 0% with a 3% introductory balance transfer fee (only for transfers made within 4 months of opening — then rises to 5%), no late payment fees, and no penalty APR for missed payments. NerdWallet named it the best balance transfer card for both 2025 and 2026. For cardholders who also want ongoing rewards after the 0% period ends, Citi Double Cash (18 months BT + 2% cash back) and Discover it Balance Transfer (18 months BT + Cashback Match) offer the best long-term value.External References

1. MoneySuperMarket — Best Balance Transfer Credit Cards (Data correct 6 July 2026)https://www.moneysupermarket.com/credit-cards/balance-transfer/

2. Forbes Advisor UK — Best 0% Balance Transfer Credit Cards UK 2026 (1 week ago)

https://www.forbes.com/advisor/uk/credit-cards/balance-transfer/

3. Uswitch — Compare 0% Balance Transfer Credit Cards: July 2026 (2 weeks ago)

https://www.uswitch.com/credit-cards/credit-card-balance-transfers/

4. NerdWallet US — Best Balance Transfer Credit Cards of July 2026 (1 week ago)

https://www.nerdwallet.com/credit-cards/best/balance-transfer

5. Bankrate US — Best Balance Transfer Cards of July 2026 (1 week ago)

https://www.bankrate.com/credit-cards/balance-transfer/best-balance-transfer-cards/

6. CreditCards.com — Best Balance Transfer Credit Cards July 2026 (1 week ago)

https://www.creditcards.com/balance-transfer/

7. GoodMoneyGuide — Best Balance Transfer Credit Cards 2026 Compared (June 2026)

https://goodmoneyguide.com/banking/credit-cards/balance-transfer-credit-cards/

8. Compare the Market — 0% Balance Transfer Credit Cards (Updated 6 July 2026)

https://www.comparethemarket.com/credit-cards/balance-transfer/

0 Comments Comments