Vehicles & Cars

How to Get Cheap Car Insurance in the UK: Complete Guide

Table of Contents

- Introduction: UK Car Insurance in 2026 — Prices Are Falling, but You Still Need to Act

- UK Car Insurance Costs in 2026: What Drivers Are Actually Paying

- 14 Proven Strategies to Cut Your Car Insurance Premium

- The Single Biggest Win: Shop 21–28 Days Before Renewal

- Using Comparison Sites Effectively: The Four-Site Rule

- Telematics (Black Box) Insurance: When It Works Best

- No Claims Discount: Your Most Valuable Long-Term Asset

- Car Insurance Groups: How Vehicle Choice Determines Your Premium

- Pay Annually and Choose Your Excess Carefully

- Paying Monthly vs Annually

- Voluntary Excess

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

UK Car Insurance in 2026 — Prices Are Falling, but You Still Need to Act

There is good news for UK drivers in 2026: car insurance premiums have been falling steadily since their peak in late 2023 and early 2024. The Confused.com Q2 2026 Price Index, based on more than six million real car insurance quotes, shows the UK national average at £719 per year — down 5% (£38) compared to the same period in 2025, and significantly below the peak. 17-year-olds are paying £356 less than a year ago, a 17% reduction. Prices in Manchester and Merseyside have fallen by £89 on average (-10% year-on-year). Inner London remains the most expensive area at £1,088, but even this represents an 8% fall.Here is the catch: falling market prices only benefit you if you actively shop around. MoneySavingExpert's analysis of almost one million quotes (MoneySuperMarket, November 2025 to January 2026) found that the average driver who buys car insurance on their renewal day pays £723 per year. The same driver buying 25 days before renewal pays £377 — a difference of £346. In January 2026, Martin Lewis stated directly: 'car insurance prices have fallen by approximately 11% over the past year, meaning drivers who have auto-renewed without checking the market are almost certainly paying more than necessary.' Auto-renewing is the single most expensive mistake UK drivers make.

This guide covers every proven method for reducing your car insurance premium in 2026, from the single highest-impact action (shopping early and using multiple comparison sites) through to telematics policies, no claims discount strategy, insurance group selection, and the lesser-known tactics that consistently produce savings. The 14 strategies are mapped against effort level and realistic saving to help you prioritise. Whether you are a 17-year-old facing a £2,000 first quote or a 45-year-old looking to squeeze more out of an already competitive renewal, the evidence is clear: there is almost always money to be saved by someone who knows where to look.

UK Car Insurance Costs in 2026: What Drivers Are Actually Paying

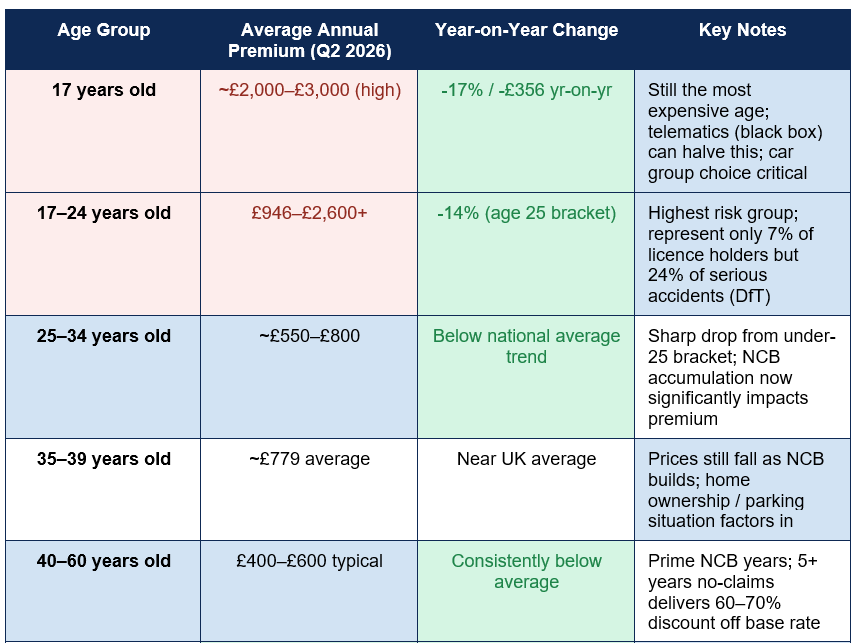

The Confused.com Q2 2026 Price Index — the UK's most comprehensive real-quote car insurance dataset, collecting over six million quotes per quarter — provides the most current picture of what UK drivers are actually paying. The table below shows average premiums by age group, year-on-year changes, and the key factors that influence each bracket:

The regional variation: Inner London average £1,088 vs South West average £504 — location is one of the most significant premium factors after age — inner city drivers in London pay more than double the premium of equivalent drivers in the South West. Manchester and Merseyside saw the biggest annual reductions — £89 (-10%) year-on-year (Confused.com Q2 2026).

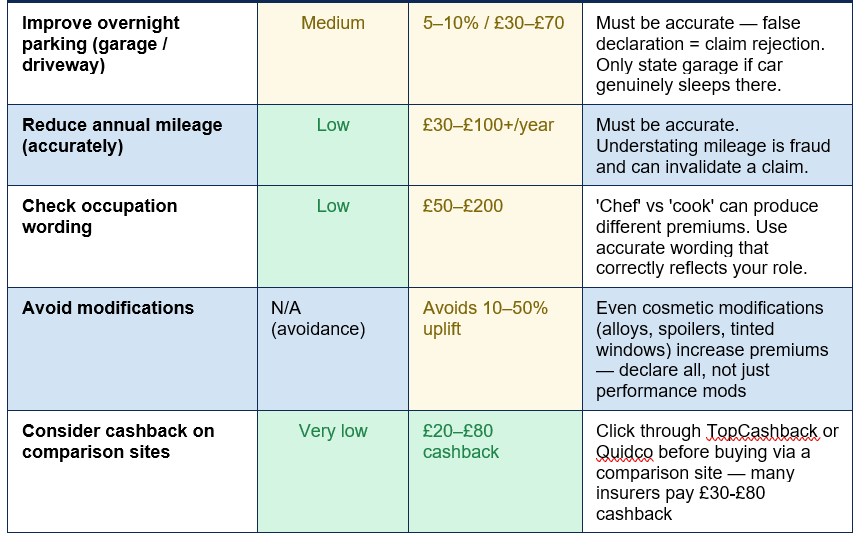

14 Proven Strategies to Cut Your Car Insurance Premium

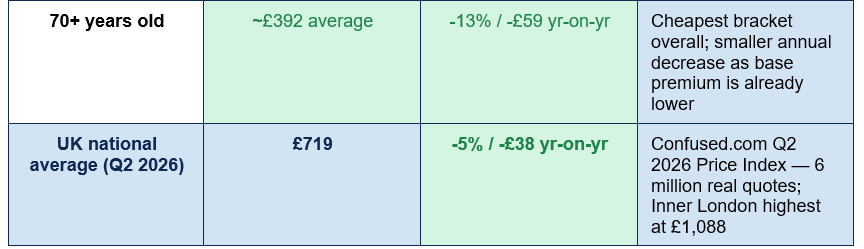

The table below maps every major premium reduction strategy against effort level, realistic saving, and the key details or caveats that determine whether it applies to your situation:

The Single Biggest Win: Shop 21–28 Days Before Renewal

The most impactful, easiest, and least-known car insurance saving available to UK drivers in 2026 is simply timing when you buy. MoneySavingExpert's analysis of nearly one million real quotes found that the cheapest day to buy car insurance is approximately 25 days before your policy start date — with the average premium at that point being £377 versus £723 on the actual renewal day. That is a saving of £346 on the same policy from the same insurer pool, simply by buying 25 days earlier.Why does this happen? Insurers use buying behaviour as a risk signal. Drivers who are renewing on the day their policy expires are statistically seen as higher risk — they may not have shopped around, they may be less organised, and organised, proactive drivers who plan their renewal tend to have better overall risk profiles. Buying too early (more than 27 days out) also pushes prices up slightly as fewer insurers provide quotes that far in advance. The sweet spot, confirmed by both MoneySavingExpert (25 days) and Confused.com (28 days), is three to four weeks before your renewal date.

CALENDAR ACTION: Set a reminder now, 25 days before your next renewal date, labelled 'Car insurance: compare and buy today.' This single action, applied every year, saves hundreds of pounds over a driving lifetime.

The loyalty premium myth vs the comparison gap: Since 2022, FCA rules have banned insurers from charging renewing customers more than new customers — ending the 'price-walking' penalty for loyalty. But as Martin Lewis explained in January 2026, this does not mean your renewal quote is a good deal. It means the worst practice has been stopped. The comparison gap between different insurers for the same driver is still very real and very wide. Shopping around is not about getting a loyalty penalty reversed — it is about finding the insurer whose algorithm prices your specific risk profile most favourably. Different insurers weight the same risk factors completely differently, which is why identical drivers can receive quotes hundreds of pounds apart.

Using Comparison Sites Effectively: The Four-Site Rule

No single comparison site covers every insurer. This is the most important practical fact about using price comparison websites for car insurance. Each of the four main sites — MoneySuperMarket, Compare the Market, GoCompare, and Confused.com — has its own panel of insurers, and the overlap between them is not complete. An insurer that appears on Compare the Market may not appear on MoneySuperMarket, and vice versa.The four-site rule says: run quotes on all four major comparison sites, and then check directly with the two or three major insurers who do not feature on comparison sites — primarily Direct Line and Admiral (in some circumstances). This takes approximately 20-30 minutes but consistently produces a wider spread of quotes than using a single site. MoneySavingExpert recommends MoneySuperMarket and Compare the Market as the two to prioritise if time is limited, as they tend to have the largest insurer panels. The price optimiser tool on MoneySuperMarket, launched in April 2026, adjusts your quote details interactively to find the cheapest combination of excess, mileage, and other factors.

Once you have your best comparison site quote, call the insurer directly and ask if they can match or improve it. Many insurers have direct-purchase discounts not available through comparison sites, and the retention team of your current insurer will often match a quote from a competitor rather than lose a customer they can see is actively shopping.

Telematics (Black Box) Insurance: When It Works Best

Telematics insurance — also called black box insurance — uses data from a device fitted to your car, a plug-in OBD dongle, or a smartphone app to price your premium based on how you actually drive rather than solely on statistical group characteristics like age and postcode. Speed, braking, cornering, acceleration, time of day, and annual mileage are all recorded and used to calculate your risk profile, which then determines your premium at renewal.Consumer Intelligence research from November 2025 (cited by Which? and MyMoneyComparison) found that telematics policies were the cheapest option 42% of the time across all quotes, with an average saving of £228 where they were cheaper. For drivers aged 17-19 specifically, the impact is transformative: the cheapest telematics premiums were roughly half the price of the cheapest conventional alternatives, with price differences exceeding £1,000 per year in some cases. For any driver under 25 or anyone with a limited driving history, telematics insurance should always be included in the comparison set.

The key consideration for telematics is lifestyle fit. Most black box policies include curfews (restrictions on when you can drive without a premium penalty — typically midnight to 5am) or time-of-day scoring that penalises night driving. If you regularly drive late at night for work or social reasons, the curfew penalty may offset the premium saving. For drivers whose lifestyle accommodates the restrictions, black box insurance is consistently one of the cheapest available products in 2026.

No Claims Discount: Your Most Valuable Long-Term Asset

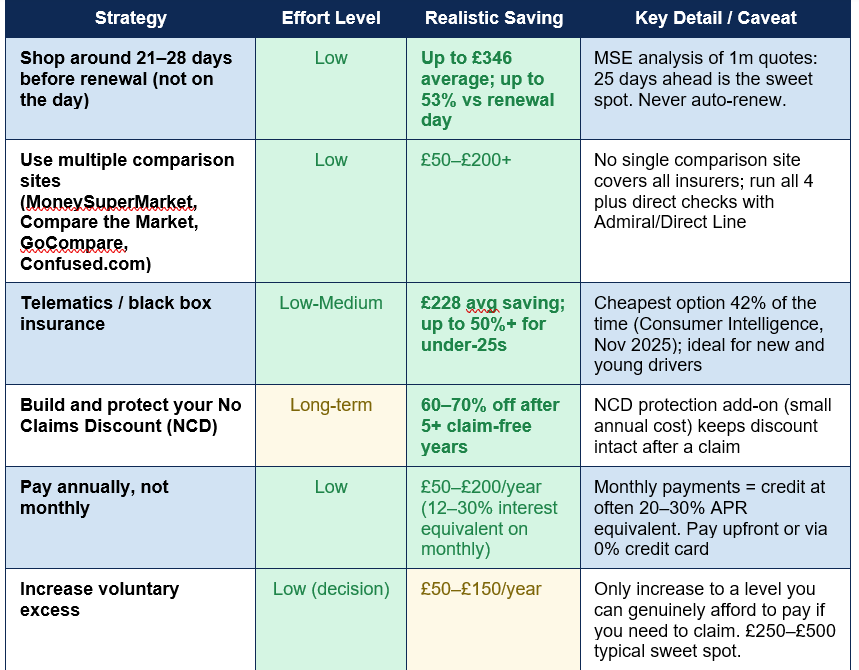

The No Claims Discount (NCD) — sometimes called No Claims Bonus (NCB) — is the single most valuable long-term car insurance asset a UK driver can build. After five or more consecutive claim-free years, the NCD typically delivers a discount of 60-70% off the base premium that would otherwise apply to your age, car, and location profile. For a driver whose base premium would be £800 without NCD, five years of no claims converts that to approximately £240-£320.Three important NCD strategies that many drivers do not know about: First, NCD protection add-ons allow you to make one claim (sometimes two) per year without losing your accumulated discount. The add-on typically costs £20-£50 per year and is almost always worth purchasing once you have accumulated four or more years of NCD. Second, NCD is portable — it follows you as a driver from insurer to insurer when you switch, provided you can evidence it with your renewal notice or a letter from your previous insurer. Third, NCD can typically be built on a company car and transferred to a private policy when you leave employment, provided your employer's insurer will confirm your claim-free record in writing.

The fronting trap — a common mistake with serious consequences: Some young drivers are set up as the named driver on a parent's policy, with the parent listed as the main driver, to access lower premiums. This is called fronting, and it is insurance fraud. If a claim is made and the insurer determines the true main driver was the listed named driver rather than the policyholder, the claim can be voided entirely and the policy cancelled. The consequence — no insurance, a potential fraud record, and no NCD — is catastrophically worse than the higher premium a young driver would have paid on their own policy. Young drivers should be the primary policyholder on their own insurance from the first day they drive their own car.

Car Insurance Groups: How Vehicle Choice Determines Your Premium

Every car sold in the UK is allocated an insurance group rating that directly influences premiums across all insurers. The group is determined by Thatcham Research based on the car's engine power, repair costs, safety rating, security features, and theft profile. A lower group number means a cheaper car to insure — and for young drivers in particular, the group choice at purchase can represent the most impactful long-term premium decision available.The UK is currently in an 18-month transition period between two insurance group systems. Cars registered before August 2024 use the traditional 1-50 scale. Cars registered from August 2024 onward use the new Vehicle Risk Rating (VRR) system on a 1-99 scale, introduced by Thatcham Research and the ABI to provide greater pricing granularity. During the transition period, most insurers use both systems simultaneously. You can check any car's insurance group for free at the Thatcham Research website using the vehicle's registration number.

For under-25 drivers, the difference between a Group 1-5 car and a Group 20-25 car can be £1,000-£2,000 per year in premium. Over three years — the typical period before a young driver's age-based premium begins to fall significantly — that difference represents a saving that often exceeds the total purchase price of the car. Checking the insurance group before buying any car is one of the highest-return five-minute actions available to a UK car buyer.

CHECK BEFORE YOU BUY: Before purchasing any car — new or used — enter its registration at check.thatcham.org to see its insurance group. This single step, done before any purchase decision, can save hundreds or thousands of pounds per year in premiums.

Pay Annually and Choose Your Excess Carefully

Paying Monthly vs Annually

Monthly car insurance payments are not cheaper than annual ones — they are typically 20-30% more expensive in total, because monthly payment is effectively a credit arrangement that the insurer charges interest on. The equivalent APR on many monthly car insurance payment plans is 20-40%. A £600 annual premium paid monthly might cost £720 over the year — an additional £120 for the convenience of spreading payments. Paying annually eliminates this cost entirely. Where the annual payment is a cashflow challenge, using a 0% interest credit card to pay the annual premium and then repaying the credit card across the year achieves the same result at no interest cost.Voluntary Excess

Increasing your voluntary excess — the amount you agree to contribute toward any claim — reduces your premium, but the saving must be weighed against the risk of needing to pay the excess if you make a claim. The MoneySuperMarket Price Optimiser data from April 2026 confirmed that increasing voluntary excess returned a cheaper price in a majority of cases. The recommended approach is to set voluntary excess at a level you could genuinely afford to pay immediately from your savings if you needed to claim — typically £250-£500 for most drivers. Excess above this level reduces premiums meaningfully but creates financial vulnerability that the saving may not justify.Conclusion

UK car insurance premiums are falling in 2026 — down 5% year-on-year to an average of £719 according to Confused.com's Q2 2026 Price Index — but falling market prices only benefit drivers who actively compare and switch rather than auto-renewing. The evidence from MoneySavingExpert's analysis of nearly one million quotes is unambiguous: buying 25 days before renewal saves an average of £346 compared with buying on the day. That single action, combined with using all four major comparison sites and checking directly with off-panel insurers like Direct Line, is the foundation of cheap car insurance in 2026.Beyond timing and shopping around, the strategies with the highest impact per unit of effort are telematics insurance (42% of the time cheapest, with average savings of £228 — and up to 50% savings for under-25s), no claims discount accumulation and protection (60-70% off after five years), paying annually rather than monthly (20-30% effective interest saving), and insurance group selection at the point of vehicle purchase (£200-£1,500/year difference between Group 5 and Group 25 for the same driver). The new Vehicle Risk Rating system introduced for cars from August 2024 is still being integrated into insurer pricing, making it particularly important to check VRR ratings before any new vehicle purchase.

The common thread across every strategy in this guide is the same: car insurance is not a fixed price, and the insurer's default renewal is not the best available offer. The market is competitive, the pricing algorithms vary widely between insurers for the same driver, and the reward for five minutes of comparison is frequently several hundred pounds per year. Set the calendar reminder for 25 days before your renewal. Use all four comparison sites. Include telematics in your comparison set if you are under 30. Protect your NCD once you have earned four years. Pay annually. And never, under any circumstances, simply auto-renew.

Frequently Asked Questions (FAQ)

What is the average cost of car insurance in the UK in 2026?

The UK national average car insurance premium was £719 in Q2 2026 according to the Confused.com Price Index, based on more than six million real car insurance quotes. This is down 5% (£38) year-on-year. Premiums vary significantly by age — 17-year-olds pay an average of £2,000 to £3,000, while 70-year-olds average around £392. Regional variation is substantial: Inner London drivers average £1,088 while South West drivers average £504. The overall market trend has been downward since the peak in late 2023 to early 2024, though Confused.com noted a £8 month-on-month increase in Q2 2026, the first since late 2023.What is the cheapest time to buy car insurance?

MoneySavingExpert's analysis of nearly one million car insurance quotes (MoneySuperMarket, November 2025 to January 2026) found that the cheapest day to buy car insurance is approximately 25 days before your policy start date. The average premium bought at this point was £377, compared with £723 on the actual renewal or start day — a difference of £346. Confused.com's data similarly identifies buying around 28 days before renewal as producing premiums up to 53% cheaper than buying on the day. The sweet spot for most drivers is 21-28 days before renewal. Set a calendar reminder 25 days ahead and shop on that day for maximum savings.Is black box (telematics) insurance worth it?

For most drivers under 30, and particularly those aged 17-25, telematics insurance is consistently one of the best available options for reducing premiums. Consumer Intelligence research from November 2025 found telematics was the cheapest option 42% of the time, with an average saving of £228 where it was cheaper. For drivers aged 17-19, telematics premiums can be roughly half the cost of equivalent conventional insurance — a difference of over £1,000 per year in some cases. The main consideration is whether the policy's driving restrictions (typically midnight to 5am curfews and time-of-day scoring) are compatible with your lifestyle. For drivers who rarely need to drive late at night, telematics is strongly worth including in every comparison.Is comprehensive car insurance always more expensive than third-party?

No — and this is one of the most persistently misunderstood facts about UK car insurance. Comprehensive cover is often priced lower than third-party only (TPO) or third-party fire and theft (TPFT) for the same driver. The reason is that drivers who opt for TPO cover are, statistically, a higher-risk group on average — often younger or with more limited driving history — which pushes up the base premium that insurers charge for that level of cover. Always request quotes at all three levels of cover when comparing policies, and never assume that less cover means a lower cost. The MoneySavingExpert guide confirmed this market quirk explicitly, as did the 2026 guidance from Pocketwise and MyMoneyComparison.How much can no claims discount save me?

After five or more consecutive claim-free years, a No Claims Discount (NCD) typically delivers 60-70% off your base premium. For a driver whose base premium without NCD would be £800, five years of no claims reduces that to approximately £240-£320. NCD is portable — it follows you when you switch insurers, provided you can evidence it with a letter from your previous insurer. NCD protection add-ons (costing typically £20-£50 per year) allow you to make one or two claims without losing your discount, and are almost always worth purchasing once you have accumulated four or more years. Building NCD from the first year of driving is the most valuable long-term car insurance investment available to any UK driver.

External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Confused.com — Q2 2026 Car Insurance Price Index (Published 24 June 2026)

https://www.confused.com/compare-car-insurance/average-car-insurance-cost-uk

2. MyMoneyComparison — How to Reduce Car Insurance Costs: 14 UK Tips in 2026 (March 2026)

https://www.mymoneycomparison.com/how-to-reduce-car-insurance-costs/

3. Brumble — Average Car Insurance Cost UK: £560–£719 in 2026 (June 2026)

https://brumble.co.uk/guides/car-insurance-cost-2026

4. Carsa — Cheapest Cars to Insure for New Drivers UK 2026 (July 2026)

https://www.carsa.co.uk/blog/cheapest-cars-insure-new-drivers-uk-2026

5. Confused.com — New Year Savings: Car Insurance Prices Drop by £111 on Average

https://www.confused.com/press/releases/2026/new-years-savings-car-insurance-prices-drop-by-111-on-average

6. Thatcham Research — Vehicle Insurance Group Check (Official ABI/Thatcham Tool)

https://www.thatcham.org/abi-group-rating-check/

7. Association of British Insurers (ABI) — Motor Insurance Premium Tracker Q1 2026

https://www.abi.org.uk/products-and-issues/topics-and-issues/motor-premium-tracker/

0 Comments Comments