Credits

What Is a Travel Credit Card? UK Complete Guide

Table of Contents

- The Hidden Cost of Using the Wrong Card Abroad

- What Is a Travel Credit Card?

- Standard Cards vs Travel Cards: The Cost Comparison

- How Exchange Rates Work on Travel Credit Cards

- The Dynamic Currency Conversion Trap

- Best UK Travel Credit Cards: July 2026

- Section 75: The Legal Protection That Makes Travel Cards Irreplaceable

- Travel Credit Card vs Travel Debit Card vs Prepaid Travel Card

- Travel Credit Card

- Travel Debit Card (Starling, Monzo, Chase)

- Prepaid Travel Cards

- What to Look For When Choosing a Travel Credit Card

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Hidden Cost of Using the Wrong Card Abroad

Most UK credit and debit cards charge a fee every time you use them to spend money outside the United Kingdom. This fee — called a non-sterling transaction fee, a foreign usage fee, or a currency conversion fee — is typically between 2.75% and 3% of every transaction. It applies whether you are buying a coffee in Paris, booking a hotel in Barcelona, or shopping online with a retailer based outside the UK. It applies on top of whatever exchange rate the card uses.Example illustrates the cumulative cost clearly: if you make 50 transactions of £25 each during a typical two-week holiday (totalling £1,250 of spending), a standard card charging 3% adds £75 in fees — the equivalent of two meals, a museum entry, or a family day out completely wasted on charges you could have avoided. Analysis of spending $1,000 in the United States showed a top specialist travel credit card returning £740 to your account in sterling versus significantly less on a poor card — a difference of tens of pounds on a single medium-cost trip.

A travel credit card is a standard UK credit card that eliminates these fees. It does two things that a typical card does not: it waives the non-sterling transaction fee on purchases abroad, and it uses the Visa or Mastercard interbank exchange rate — the closest to the mid-market rate available on any payment card — rather than the bank's inflated proprietary rate. The best travel credit cards add a third layer of value: Section 75 consumer protection, which makes the card issuer jointly liable with any retailer for purchases of £100 to £30,000. This guide explains how travel credit cards work, what the best options are in July 2026, the traps to avoid, and how to combine a travel card with a complementary debit card for the ideal dual-card travel setup.

What Is a Travel Credit Card?

A travel credit card is a credit card specifically designed and marketed for use when spending in foreign currencies — whether abroad in person or online with international retailers. Its defining characteristic is the absence of non-sterling transaction fees, which are the charges that standard cards levy on every foreign currency purchase. Beyond fee elimination, the best travel credit cards also offer favourable exchange rates, no fees on overseas ATM withdrawals (though interest on cash withdrawals typically still applies), and additional travel-relevant benefits.The term 'travel credit card' covers several product types that are worth distinguishing:

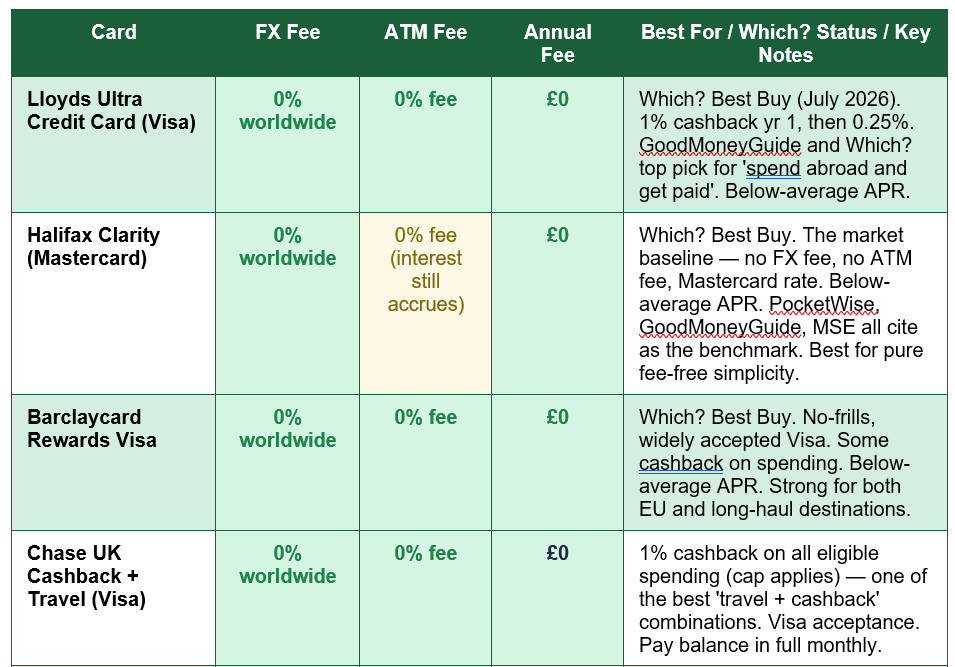

- Pure fee-free travel cards: Cards that exist primarily to provide fee-free foreign spending with the interbank exchange rate. No rewards, minimal additional features, usually no annual fee. Halifax Clarity and Barclaycard Rewards are the defining UK examples. These are the simplest and most accessible travel cards, and Which? has named both as Best Buys in its July 2026 review.

- Travel + cashback cards: Cards that combine fee-free foreign spending with cashback on all spending — both abroad and at home. Lloyds Ultra (1% cashback year one, then 0.25%, which is also a Which? Best Buy) and Chase UK (1% cashback with no annual fee on Visa) are the strongest examples. These are travel cards with an ongoing reward mechanism, making them useful both abroad and in the UK.

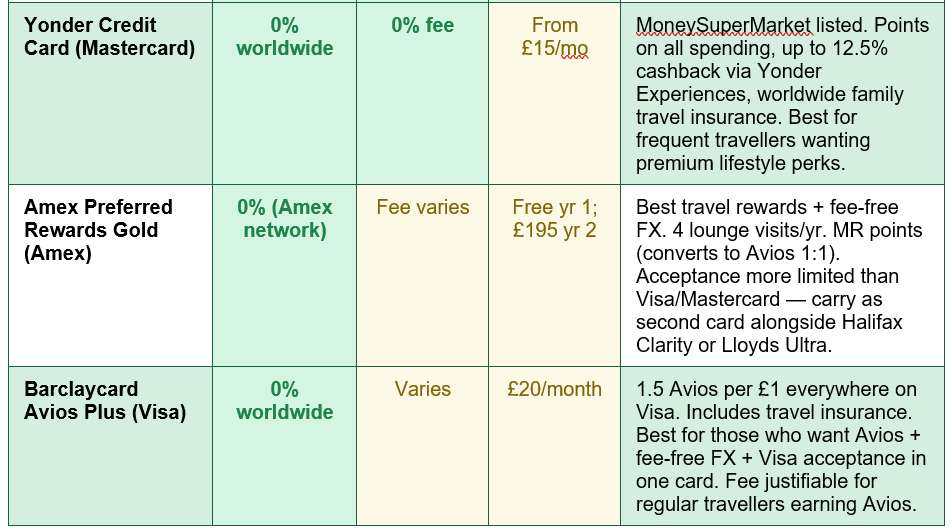

- Travel + airline miles / points cards: Cards that earn Avios, Membership Rewards points, or Virgin Points on all spending, while also eliminating foreign transaction fees. Barclaycard Avios Plus (1.5 Avios per £1 everywhere, Visa, no FX fee) and Amex Preferred Rewards Gold (MR points convertible to Avios, no FX fee, four lounge visits) fall into this category. These carry fees but deliver more value for regular travellers who will use the points.

- Premium travel cards: High-fee cards that bundle extensive travel perks — lounge access, travel insurance, hotel credits, concierge services — alongside fee-free foreign spending. Amex Platinum and Yonder are UK examples. Only financially worthwhile for frequent travellers who use enough of the benefits to exceed the annual fee value.

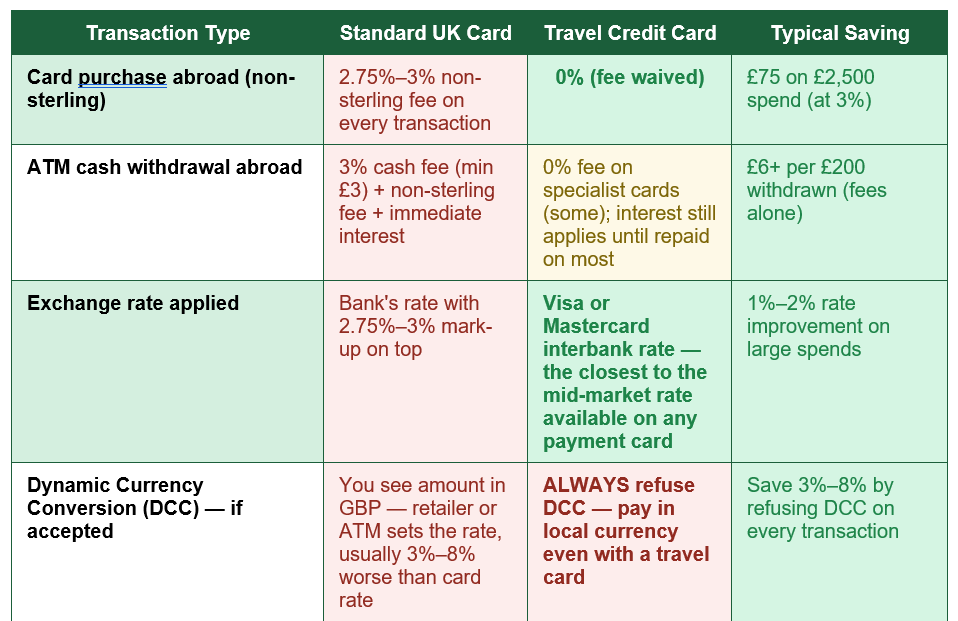

What standard cards cost abroad: 2.75%–3% on every transaction + 3% on ATM withdrawals (min £3) — Using a standard UK card for 50 purchases of £25 on holiday (£1,250 total) costs £75 in non-sterling fees at 3%. A travel credit card costs £0 for the same spending. The average UK two-week holiday involves hundreds of card transactions — the cumulative saving of a travel card is material and guaranteed (MoneySuperMarket July 2026 / Compare the Market July 2026).

Standard Cards vs Travel Cards: The Cost Comparison

The table below maps every major transaction type that occurs during a foreign trip, comparing what a standard UK card charges against what a travel credit card charges, and the saving involved. Understanding each row helps you select the right combination of cards for your travel:

How Exchange Rates Work on Travel Credit Cards

The exchange rate your card uses when you spend abroad is the second critical factor after the fee structure. Most standard UK cards apply their own proprietary exchange rate, which typically includes a mark-up of 2% to 3% on the underlying interbank (mid-market) rate. This mark-up is separate from the non-sterling transaction fee — meaning a card can charge both simultaneously.Travel credit cards use the Visa or Mastercard network exchange rate, which is updated daily and tracks very closely to the interbank mid-market rate — the rate shown on financial data sites like Google Finance or XE.com. Uswitch's July 2026 guide confirms: 'The Visa and Mastercard exchange rates are about the best you'll find anywhere.' This means that using a travel credit card with Visa or Mastercard network produces a conversion as close to the true mid-market rate as any payment card can deliver.

American Express operates its own exchange rate, which is similarly competitive but calculated independently from Visa and Mastercard. The practical difference between Amex, Visa, and Mastercard exchange rates is typically negligible on any individual transaction, though it can accumulate on very large volumes of foreign spending.

The Dynamic Currency Conversion Trap

Dynamic Currency Conversion (DCC) is the practice of a foreign retailer or ATM operator offering to convert your purchase into pounds sterling at the point of sale, rather than processing it in the local currency. The offer appears as a convenience — you can see exactly how much you are paying in pounds — but it is almost always significantly more expensive than letting your travel card apply its own exchange rate.When a retailer converts the transaction to sterling, they set the exchange rate — and that rate is typically 3% to 8% worse than the Visa or Mastercard rate your travel card would have applied. MoneySavingExpert is unambiguous on this: always refuse DCC and pay in the local currency. This applies even if the retailer is insistent, even if the ATM makes refusing difficult, and even if you are using a travel card with no foreign transaction fees — the DCC rate can wipe out the saving from having no FX fee and add a significant additional cost on top.

The DCC rule made simple: When any card machine, restaurant terminal, or ATM abroad offers to show you the amount in pounds, or asks whether you want to pay in 'your home currency', always select 'Pay in local currency' or 'Continue without conversion'. Accepting the conversion to pounds means you pay the retailer's rate. Refusing means you pay Visa or Mastercard's rate, which is materially better. This single rule, applied consistently on every transaction, can save 3%–8% on every foreign purchase regardless of which card you use.

Best UK Travel Credit Cards: July 2026

The table below covers the best UK travel credit cards as of July 2026, sourced from Which? (137 cards compared, data correct to 1 July 2026, 4,995 customers surveyed), GoodMoneyGuide (April 2026), MoneySavingExpert (May 2026), PocketWise (April 2026), and MoneySuperMarket (data updated 3 July 2026):

THE TWO-CARD STRATEGY: Most travel finance experts recommend carrying two complementary cards when travelling abroad: a fee-free travel credit card (like Halifax Clarity or Lloyds Ultra) for purchases, providing Section 75 protection and 0% FX fees; and a fee-free travel debit card (like Starling Bank or Monzo) for ATM cash withdrawals, where debit cards avoid the interest that accrues on credit card cash withdrawals from day one. GoodMoneyGuide confirms this as the optimal approach: 'Carry two cards (ideally Visa + Mastercard), know the fees, always pay in local currency, and repay in full.'

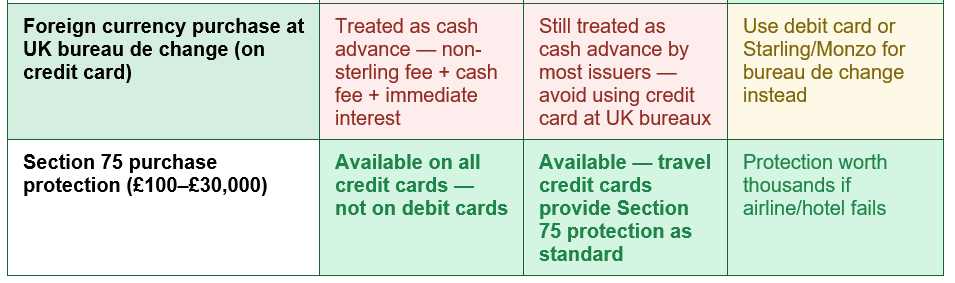

Section 75: The Legal Protection That Makes Travel Cards Irreplaceable

Section 75 of the Consumer Credit Act 1974 provides one of the most powerful and most underused consumer protections in UK law — and it is available on every UK credit card, including travel credit cards, automatically and at no additional cost. Under Section 75, the credit card company is jointly liable with any retailer for purchases of more than £100 and up to £30,000 when those goods or services are faulty, not as described, misrepresented, or never delivered.For travellers, the practical applications of Section 75 are numerous and genuinely significant. If the airline you booked with goes into administration before your flight, you can claim a full refund from your credit card company. If your hotel is significantly different from how it was described when you booked (different location, lower standard, unavailable amenities), Section 75 supports a claim. If a tour operator collapses and your package holiday is cancelled, the full value is claimable from the card issuer. These are not theoretical scenarios — several UK airlines, travel agents, and accommodation providers have collapsed in recent years, and Section 75 claims have paid out millions to affected travellers.

The protection applies even if you paid only part of the purchase price on your credit card. Paying a £50 deposit on a £2,000 holiday package using your travel credit card means the full £2,000 is covered by Section 75 — not just the £50 on the card. You needed to pay at least £1 over the £100 threshold on the credit card to trigger coverage for the full transaction amount. This makes putting even a small portion of any significant travel purchase on a credit card strategically sensible.

Debit cards and prepaid travel cards do not provide Section 75 protection — this coverage is exclusively a feature of credit cards. Debit card payments may have chargeback rights through Visa or Mastercard, which provide some limited protection, but chargeback is a voluntary scheme with shorter dispute windows and lower success rates than the statutory Section 75 entitlement. For large travel bookings, always pay on a credit card.

Travel Credit Card vs Travel Debit Card vs Prepaid Travel Card

Three types of card are commonly used for travel spending, and understanding the differences determines the optimal combination for different travellers:Travel Credit Card

Best for purchases abroad where Section 75 protection matters — hotels, flights, package holidays, car rental, and any purchase over £100. Uses Visa or Mastercard interbank rate. No foreign transaction fee. Interest applies on any balance carried after the monthly statement — so must be cleared in full each month. The gold standard for purchase protection, the worst choice for cash withdrawals (where interest accrues immediately even on fee-free ATM cards).Travel Debit Card (Starling, Monzo, Chase)

Best for ATM cash withdrawals abroad. Starling Bank's fee-free current account, Monzo, and Chase UK all provide 0% foreign transaction fees and 0% ATM withdrawal fees on their debit cards, with no interest charge on withdrawals (unlike credit cards). No Section 75 protection — use the credit card for purchases. The complementary debit card fills the cash withdrawal gap that the credit card leaves. Most experienced travellers carry one travel credit card and one fee-free debit card as their standard international payment setup.Prepaid Travel Cards

Prepaid cards — loaded with a fixed amount before travel — appeal to those who want to limit their foreign spending or who prefer not to travel with a credit card. They avoid credit risk entirely and can lock in an exchange rate. However, their exchange rates are rarely as competitive as Visa or Mastercard rates, many charge loading fees or ATM fees, and they provide no Section 75 protection. For most adult travellers with access to a travel credit card and a fee-free debit card, prepaid cards offer limited additional value and are most useful for those who do not qualify for standard credit products.What to Look For When Choosing a Travel Credit Card

The market for travel credit cards in the UK includes dozens of options, and the right card depends on your travel frequency, spending patterns, and appetite for annual fees. The following criteria framework helps narrow the choice:- Non-sterling transaction fee: Must be 0% worldwide. This is the defining feature of a travel credit card — any card that charges a foreign usage fee for transactions outside the UK is not a travel card. Verify it applies worldwide, not just in the EU.

- ATM cash withdrawal fee: The best cards charge 0% for overseas ATM withdrawals (Halifax Clarity, Lloyds Ultra, Barclaycard Rewards). Even on these cards, interest accrues on cash withdrawals from the day of withdrawal — which is why a fee-free debit card is preferred for actual cash withdrawals.

- Post-0% APR: Which? specifically highlights that the Lloyds Ultra, Halifax Clarity, and Barclaycard Rewards all have below-average APRs compared with the broader credit card market — meaning if you ever accidentally carry a balance, the interest cost is lower than on higher-rate cards.

- Network (Visa, Mastercard, or Amex): Visa and Mastercard are accepted virtually everywhere worldwide. Amex acceptance is strong in the UK, US, and major European cities but can be limited in rural areas, budget hotels, and smaller restaurants in some countries. Carry a Visa or Mastercard travel card as your primary travel card, and use Amex as a supplement where accepted.

- Annual fee: Most strong travel credit cards have no annual fee — Lloyds Ultra, Halifax Clarity, and Barclaycard Rewards are all completely free. Annual fees on travel cards (like the £20/month Barclaycard Avios Plus or the £195/year Amex Gold) are only worth paying if the ongoing rewards or benefits exceed the fee in value for your specific usage pattern.

- Additional travel benefits: Some cards add travel insurance, airport lounge access, or cashback specifically on travel booking. These add genuine value but should be compared against the card's fee before factoring them into the decision.

NEVER CARRY A BALANCE ON A TRAVEL CREDIT CARD: The benefit of fee-free foreign spending disappears entirely if you pay interest. PocketWise's analysis is specific: the saving from avoiding a 3% FX fee on £500/month overseas spending = £15/month = £180/year. A carried balance of just £300 at a typical 20% APR costs roughly the same amount annually — completely erasing the fee saving. A travel credit card is only financially beneficial when the balance is cleared in full every month. If you cannot do this, use a fee-free travel debit card (Starling, Monzo) for foreign spending instead — you will not get Section 75 protection, but you also will not pay interest.

Conclusion

A travel credit card eliminates one of the most persistent and most avoidable costs in UK personal finance — the 2.75% to 3% non-sterling transaction fee that standard credit and debit cards charge on every foreign purchase. For a typical UK traveller spending £2,500 abroad per year across purchases and bookings, a travel credit card saves approximately £75 in fees at zero cost. For those who book significant travel — flights, hotels, package holidays — it also provides Section 75 protection worth potentially thousands of pounds if an airline fails or a booking is misrepresented.The Which? Best Buys as of July 2026 — the Lloyds Ultra (0% FX fee, 0% ATM fee, 1% cashback in year one), Halifax Clarity (the market baseline — no fees, no frills, Mastercard rate), and Barclaycard Rewards Visa (0% FX, 0% ATM fee, cashback) — are all available at no annual fee. They do not require frequent travel to justify. They are worthwhile for anyone who spends money abroad even occasionally, whether at a foreign hotel, an international online retailer, or a single annual holiday. The only requirement is clearing the full balance every month, which prevents interest from wiping out every saving these cards provide.

The optimal travel payment setup for most UK adults is a two-card combination: a travel credit card for purchases (with Section 75 protection), and a fee-free travel debit card such as Starling Bank or Monzo for ATM cash withdrawals (avoiding the credit card interest on cash). Always refuse Dynamic Currency Conversion and pay in the local currency on every transaction. Apply in advance of any trip — cards can take 7 to 14 days to arrive in the post. And remember: the benefit only exists for cardholders who clear the balance in full. For those who do, a travel credit card is one of the simplest, clearest, and most consistently underused financial tools available to UK consumers.

Frequently Asked Questions (FAQ)

What is a travel credit card and how does it work?

A travel credit card is a UK credit card designed for spending abroad that charges no foreign transaction fee on purchases made in foreign currencies. Standard UK credit and debit cards typically charge 2.75% to 3% on every transaction outside the UK. A travel credit card waives this charge and uses the Visa or Mastercard interbank exchange rate — the closest to the true mid-market rate available on any payment card. The card works exactly like a standard credit card but with zero additional cost for foreign spending. You still need to clear the balance in full each month to avoid interest charges — the fee saving only exists for those who do not pay interest.What is the best travel credit card in the UK in July 2026?

Which? named the Lloyds Ultra Credit Card, Halifax Clarity, and Barclaycard Rewards Visa as Best Buys in its July 2026 review (data correct to 1 July 2026, 137 cards compared). All three have 0% foreign transaction fees, 0% ATM withdrawal fees, and no annual fee. They also have below-average APRs compared with the broader market. GoodMoneyGuide and PocketWise both recommend Halifax Clarity as the baseline benchmark for fee-free travel credit cards — it is the most commonly cited starting point for those who want simplicity and reliability. Lloyds Ultra adds 1% cashback in year one, making it the strongest 'travel plus reward' combination among no-fee cards.What is Dynamic Currency Conversion and should I use it?

Dynamic Currency Conversion (DCC) is when a foreign retailer or ATM operator offers to convert your purchase into pounds sterling at the point of sale, rather than leaving it in the local currency for your card to convert. Despite appearing convenient, DCC almost always gives you a significantly worse exchange rate than the Visa or Mastercard rate your travel card would apply — typically 3% to 8% worse. You should always refuse DCC and pay in the local currency. When a card machine shows you an amount in pounds, or an ATM asks whether you want to continue in 'your home currency', select the local currency option. This applies even when using a fee-free travel credit card — the DCC rate can exceed what you would save from having no foreign transaction fee.Does Section 75 protection apply when I use a travel credit card abroad?

Yes. Section 75 of the Consumer Credit Act 1974 applies to any purchase of more than £100 and up to £30,000 made on any UK credit card, including travel credit cards, whether the purchase is made in the UK or abroad. If the goods or services are faulty, not as described, or never delivered, and the retailer fails to resolve the issue, you can claim from your credit card company under Section 75. This is particularly valuable for travel bookings — flights, hotels, holidays, car rental — where supplier failure or misrepresentation does occur. The protection applies even if you only paid part of the purchase on the card, provided the total transaction value exceeds £100. Debit cards and prepaid travel cards do not provide Section 75 protection.Should I use a travel credit card or a travel debit card for cash withdrawals abroad?

For cash withdrawals specifically, a travel debit card from a fee-free provider (Starling Bank, Monzo, or Chase UK) is generally preferable to a travel credit card. Even on the best fee-free travel credit cards — Halifax Clarity, Lloyds Ultra, Barclaycard Rewards — cash withdrawals accrue interest from the day of withdrawal until the balance is cleared in full, because credit card cash advances are not covered by the same grace period as purchases. A fee-free travel debit card has no interest on withdrawals, no cash advance fee, and no foreign transaction fee. The recommended setup is to use a travel credit card for all purchases (to get Section 75 protection and fee-free foreign spending) and a travel debit card for ATM cash withdrawals. Apply for both before travelling.External References

1. Which? — Best Travel Credit Cards July 2026 (137 cards compared, data correct 1 July 2026, 4,995 customers surveyed)

https://www.which.co.uk/money/credit-cards-and-loans/credit-cards/best-credit-card-deals/best-travel-credit-cards-aHLGN5d6y8JR

2. MoneySuperMarket — Best Travel Credit Cards July 2026 (Data updated 3 July 2026)

https://www.moneysupermarket.com/credit-cards/travel-credit-cards/

3. Uswitch — Compare Best Travel Credit Cards UK July 2026 (Updated 1 month ago)

https://www.uswitch.com/credit-cards/best-travel-credit-cards/

4. PocketWise — Best Travel Credit Cards UK 2026: No Foreign Transaction Fees (April 2026)

https://pocketwise.co.uk/credit-cards/travel/best-travel-credit-cards-uk/

5. GoodMoneyGuide — Best Travel Credit Cards for 2026 (April 2026)

https://goodmoneyguide.com/banking/credit-cards/travel-credit-cards/

6. money.co.uk — Best Credit Cards with No Foreign Transaction Fee (Updated 1 week ago)

https://www.money.co.uk/credit-cards/credit-cards-with-no-foreign-transaction-fees

7. Compare the Market — Best Travel Credit Cards (Panel updated 3 July 2026)

https://www.comparethemarket.com/credit-cards/use-abroad/

0 Comments Comments