Finance

How Does Compound Interest Work? Complete Guide

Table of Contents

- The Most Powerful Force in Personal Finance

- What Is Compound Interest?

- Simple Interest vs Compound Interest: The Core Distinction

- The Compound Interest Formula Explained

- Worked Examples Using the Formula

- Compounding Frequency: Does Daily or Monthly Compounding Really Matter?

- The Power of Compounding Over Time: The Growth Table

- The Most Important Compound Interest Lesson: Start Early

- Compound Interest in Action: UK Savings, Debt, and Investing Scenarios

- What Is AER? The Standard Rate That Accounts for Compounding

- The Dark Side: How Compound Interest Works Against Borrowers

- ISAs, Pensions, and Tax-Free Compounding

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

The Most Powerful Force in Personal Finance

Compound interest has been called the eighth wonder of the world — a phrase often attributed to Albert Einstein, though its precise origin is debated. What is not debated is the sentiment: compound interest is one of the most powerful mathematical forces available to savers and investors, and one of the most dangerous forces working against borrowers. It is, at its simplest, the ability to earn interest on interest. And it is this apparently modest extra step — earning returns not just on your original money but on every pound of accumulated interest as well — that turns small, patient deposits into significant sums over time.The numbers make the case more powerfully than any description. Deposit £10,000 at 4% annual interest and leave it for 40 years using simple interest — the basic calculation applied only to the original amount — and you end up with £26,000. Apply compound interest to the same £10,000 at the same 4% rate for the same 40 years, and you end up with £48,010. The difference is not a small adjustment: it is almost £22,000 extra on the same £10,000 deposit. That gap — between £26,000 and £48,010 — is the concrete financial value of compounding over four decades. It is why Aviva's investment education describes it with the phrase: 'Put simply, compound interest is the ability to earn interest on interest on interest over the life of your investment.'

This guide explains everything about compound interest for UK readers in 2026: what it is and how it works, the difference from simple interest, the formula, how compounding frequency (daily vs monthly vs annual) affects returns, the extraordinary power of starting early, how the same force that builds wealth for savers destroys borrowers who carry credit card debt, what AER means and why it matters when comparing accounts, and the practical steps to maximise the benefit of compounding in UK savings accounts, ISAs, and long-term investments.

What Is Compound Interest?

Compound interest is interest calculated on both the original principal amount and on the accumulated interest from previous periods. In other words, once interest is added to your balance, it immediately begins earning further interest itself. The interest earns interest. Over multiple compounding periods, this creates an accelerating, self-reinforcing cycle of growth.Equifax's explanation captures the mechanism clearly: 'Compound interest refers to the principle that when you save money, as well as earning interest on the savings, you also earn interest on the interest itself. Therefore, every year that the money is in your account you are earning interest on each previous year's interest.' This creates a snowball effect: the longer money is left to compound, the faster the absolute amount of interest generated in each period grows, even with no additional contributions.

Simple Interest vs Compound Interest: The Core Distinction

Simple interest is calculated only on the original principal, every time, for every period. It does not accumulate or build on itself. If you deposit £1,000 at 10% simple interest, you earn £100 per year, every year — because each year's interest is always 10% of the same original £1,000.Compound interest calculates each period's interest on the running balance — which includes all previously earned interest. The same £1,000 at 10% compound interest earns £100 in year one (same as simple). But in year two, interest is calculated on £1,100 (the original £1,000 plus the £100 interest from year one), earning £110. In year three, interest is calculated on £1,210, earning £121. The amount of interest earned grows every year, even with no additional deposits, because the base on which it is calculated grows every year.

After 10 years, the £1,000 at 10% simple interest becomes £2,000 (£100 per year × 10 years = £1,000 in interest). The same £1,000 at 10% compound interest becomes £2,593.74 — an extra £593.74 from the same rate, over the same time, simply because of compounding. After 20 years: simple interest gives £3,000; compound interest gives £6,727.50 — more than twice as much from interest alone.

The compounding advantage in one comparison: £10,000 at 4% for 40 years: simple interest = £26,000 vs compound (daily) = £49,627 — a difference of £23,627 — the difference between simple and daily compound interest on a £10,000 deposit at 4% over 40 years is £23,627 — equivalent to starting with more than three times the original investment in additional returns. Compounding adds more to the balance in the final 10 years of a 40-year period than in the first 30 years combined — time is the most powerful variable (calculations using standard compound interest formula A = P(1 + r/n)^nt)

The Compound Interest Formula Explained

The standard compound interest formula is: A = P(1 + r/n)^nt• A = the final amount (what you end up with)

• P = the principal (your starting deposit)

• r = the annual interest rate expressed as a decimal (e.g. 4% = 0.04)

• n = the number of times interest is compounded per year (1 = annually, 12 = monthly, 365 = daily)

• t = the time in years

The formula looks more complex than it is in practice. You do not need to calculate it by hand — every major UK bank, savings comparison site, and personal finance platform provides free compound interest calculators. The value of understanding the formula is in knowing which variables to change to improve your outcome: a higher r (interest rate), a higher n (more frequent compounding), a larger P (bigger starting deposit), or a longer t (more time) will each increase the final amount, with t having the most dramatic long-term impact.

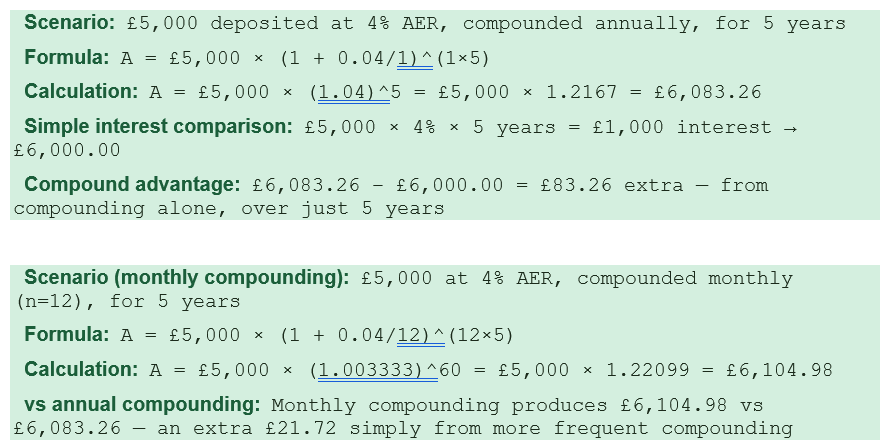

Worked Examples Using the Formula

Compounding Frequency: Does Daily or Monthly Compounding Really Matter?

Most UK savings accounts compound interest either daily or monthly. Some fixed-rate bonds compound annually. The frequency of compounding affects the final balance because more frequent compounding means interest is added to the principal more often, giving each addition slightly more time to earn further interest. As the compounding frequency increases, the benefit grows — but with diminishing returns: the jump from annual to monthly compounding is more significant than the jump from monthly to daily.Aviva's savings education provides a clear illustration: a £1,000 deposit at 5% for 10 years produces £1,628.89 if compounded annually, and £1,647.01 if compounded monthly — a difference of £18.12 on a £1,000 deposit over 10 years. That difference is modest on a small deposit, but scales directly with the amount deposited. On £100,000 over 10 years, the same difference in compounding frequency produces approximately £1,812 more from monthly vs annual compounding — meaningfully worth checking when choosing between accounts.

The practical takeaway is that while compounding frequency matters, it is the second-order concern after the interest rate itself. A savings account paying 4.5% AER compounded annually will almost always outperform one paying 4.0% AER compounded daily. When comparing savings accounts, the AER (Annual Equivalent Rate) is the standardised metric that already incorporates the effect of compounding frequency — see the AER section below.

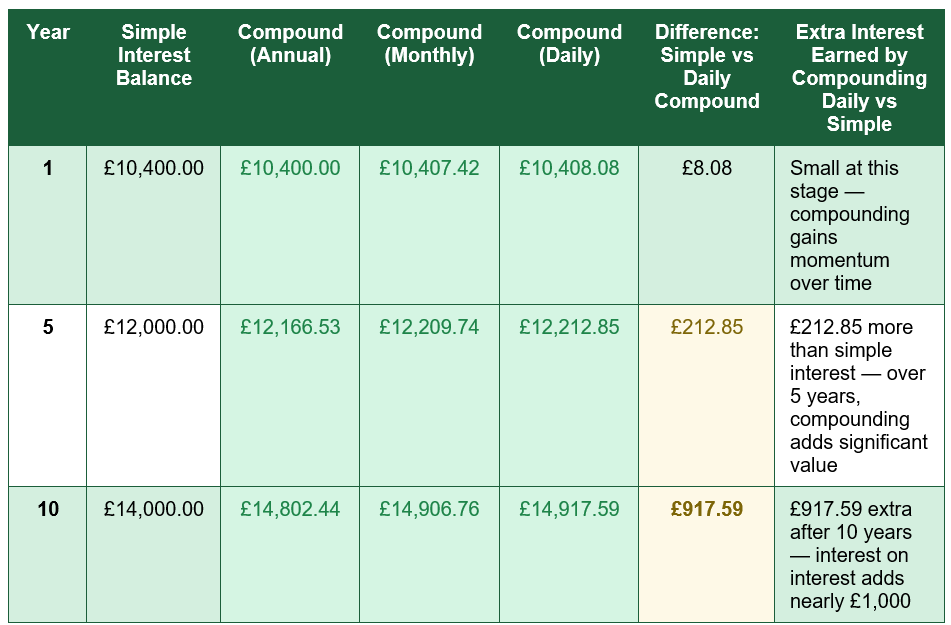

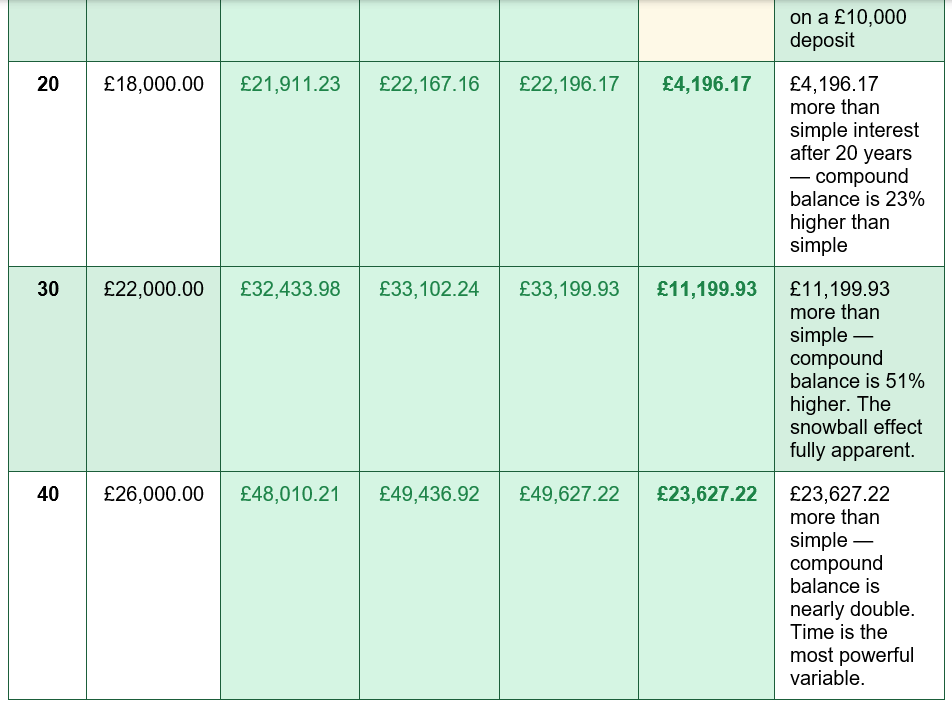

The Power of Compounding Over Time: The Growth Table

The table below illustrates the dramatic difference between simple interest and compound interest across different compounding frequencies on a £10,000 deposit at 4% AER over 40 years — showing the growing advantage of compounding as time increases:

Why compounding gains momentum: The numbers in this table reveal one of the most important features of compound interest — acceleration. In year 1, the difference between simple and compound interest on £10,000 at 4% is just £8.08. After 10 years, it is £917.59. After 20 years, it is £4,196. After 40 years, £23,627. The pound amount of interest earned grows every year — not because the rate increases, but because the balance on which the rate is applied grows with every compounding period. This is the 'snowball effect' that Aviva and many finance educators describe: a small snowball rolling down a long slope gains speed and size from the same gravitational pull, compounding its mass at each revolution.

The Most Important Compound Interest Lesson: Start Early

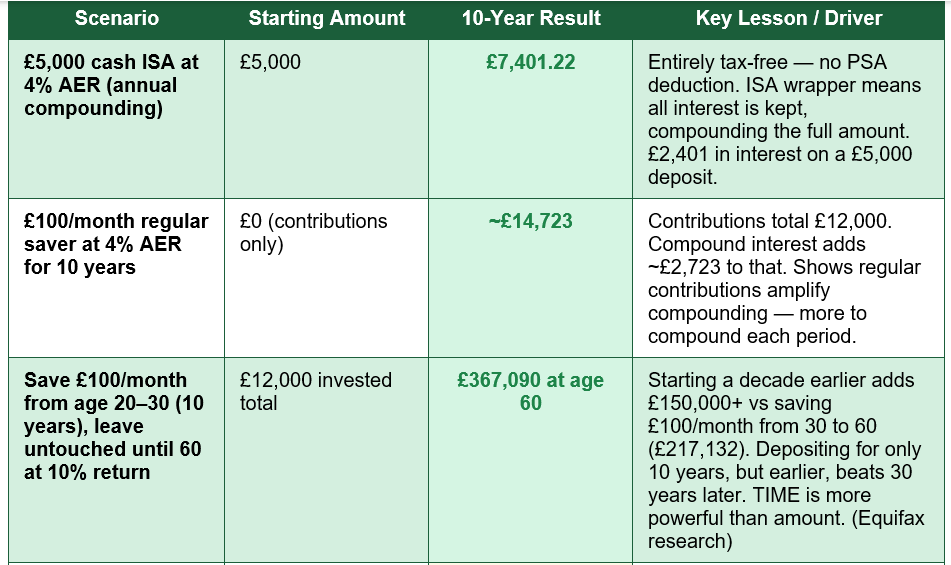

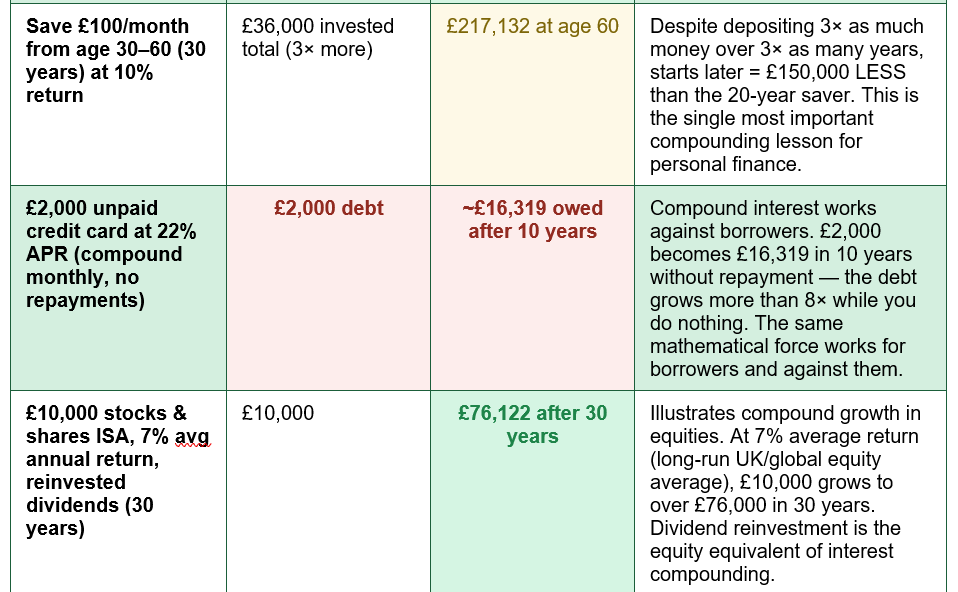

The single most impactful insight from compound interest for personal financial planning is the extraordinary advantage of starting early. The mathematics of compounding rewards time above all other variables — more than rate, more than deposit size, more than contribution frequency. This is counterintuitive and frequently underestimated.Equifax's research presents the most compelling illustration of this principle: an individual who saves £100 per month from age 20 to 30 (only 10 years of contributions, totalling £12,000 invested) and then stops completely but leaves the money untouched until age 60, will accumulate £367,090.06 at a 10% annual return. The same individual who saves £100 per month from age 30 to 60 (30 years of contributions, totalling £36,000 invested — three times more money paid in) will accumulate only £217,132.11. The person who saved for just 10 years but started a decade earlier ends up with £149,957 more — despite contributing three times less money — because their money had 30 years versus 20 years to compound.

This result appears almost paradoxical, but it is straightforward mathematics. The early saver's deposits had 30-40 years to compound rather than 20-30 years, and in the later decades of a long compounding period, the absolute annual gain in interest becomes very large because the total balance is very large. The later saver's contributions never had enough time to reach that snowball effect stage.

For UK readers, the practical implication is clear: the decision about when to start saving for the long term — whether into a pension, a stocks and shares ISA, or a long-term savings account — is more financially important than almost any other savings variable. A 25-year-old starting a pension versus a 35-year-old starting the same pension will likely retire with dramatically more money even if they contribute the same monthly amount, for the same reason illustrated above.

Compound Interest in Action: UK Savings, Debt, and Investing Scenarios

The table below illustrates compound interest across the full range of personal finance situations — savings accounts, long-term investing, pensions, debt, and the Rule of 72:

What Is AER? The Standard Rate That Accounts for Compounding

When comparing UK savings accounts, credit cards, mortgages, and other financial products, the Annual Equivalent Rate (AER) is the standardised measure that allows fair comparison across products with different compounding frequencies. The AER shows the actual annual return on a savings account taking into account the effect of compounding — it is what you will truly earn over a full year expressed as a single percentage, regardless of whether the underlying account compounds daily, monthly, or annually.This matters because two accounts can have the same nominal headline rate but different AERs if they compound at different frequencies. An account that pays 4% interest compounded monthly has an AER of approximately 4.074%, because the monthly compounding produces slightly more than 4% over the full year. An account paying exactly 4% compounded annually has an AER of exactly 4%. When comparing savings accounts, always compare AER to AER — never compare a monthly compounding rate to an annually compounding rate directly.

MoneyfactsCompare's savings guide is explicit: 'Note that when comparing the best savings accounts, you should always go by the AER, or the annual equivalent rate.' All UK savings accounts are required by the FCA to display their AER prominently, making this comparison straightforward in practice. The AER is the single number that tells you how much your money will grow in one year, all compounding effects included.

UK SAVINGS ACCOUNT TYPES AND COMPOUNDING: Different UK savings account types handle compounding differently. Easy-access savings accounts typically compound daily or monthly and allow withdrawals without penalty — best for short-term savings and emergency funds. Fixed-rate bonds lock your money for a defined term (6 months to 5 years) and typically offer higher rates, compounding annually or at maturity. Regular saver accounts reward monthly contributions and often have the highest rates, but usually limit deposit amounts. Cash ISAs compound tax-free — crucially, because the interest stays in the account without tax being deducted, the full interest amount compounds rather than the post-tax remainder. Current UK easy-access rates are around 4.5-5.2% AER; 1-year fixed bonds are around 4.8-5.3% AER.

The Dark Side: How Compound Interest Works Against Borrowers

Compound interest does not discriminate between savings and debt. The same mathematical force that steadily builds wealth for savers works in exactly the same way against borrowers who carry unpaid balances. If you only make the minimum monthly repayment on a credit card — or worse, make no repayments at all — interest is added to the outstanding balance, and then in the next period, interest is charged on the balance including that unpaid interest. The debt compounds in exactly the same way as savings, but in the wrong direction.The Fast Loan UK worked example illustrates the scale of this risk: a £2,000 credit card balance at 22% APR, with no repayments made, would grow to approximately £16,319 in 10 years. The same mathematical force that turns £10,000 into £48,000 in savings turns £2,000 of debt into £16,000 in just a decade. NatWest's guidance emphasises: 'With certain credit cards, you might have to repay both the original interest, plus interest that has built up over time. This could raise the cost of borrowing.'

The most dangerous pattern in credit card debt is the minimum repayment trap. Credit card providers set minimum monthly repayments at very low levels — often 1% to 2% of the outstanding balance or a fixed minimum of £25, whichever is higher. At 22% APR, a minimum repayment on a £2,000 balance barely keeps pace with the monthly interest charge, meaning the principal reduces extremely slowly while interest compounds continuously on most of the balance. A borrower making only minimum repayments on a £2,000 card balance at 22% APR can take 20 years or more to clear the debt, paying thousands of pounds in compound interest over that period.

THE MINIMUM REPAYMENT TRAP: Making only the minimum monthly repayment on credit card debt is one of the most financially damaging habits in personal finance. On a £2,000 balance at 22% APR, the interest charge in the first month is approximately £36.67. If the minimum repayment is £40, only £3.33 reduces the principal. As long as the balance stays near £2,000, compound interest keeps generating nearly the same monthly charge — ensuring the debt persists for years or decades. The only solution: pay as much above the minimum as possible, every month, to reduce the principal on which compound interest is calculated. Clear the full balance monthly if at all possible to avoid paying any compound interest at all.

ISAs, Pensions, and Tax-Free Compounding

In the UK, the tax environment significantly affects the real compounding return on savings and investments. Outside a tax wrapper, interest earned above the Personal Savings Allowance (PSA) — £1,000 per year for basic rate taxpayers, £500 for higher rate, and zero for additional rate — is subject to income tax. When tax is deducted from interest before it can compound, the effective compounding rate is reduced.An ISA (Individual Savings Account) eliminates this problem entirely. Interest earned inside a cash ISA, and returns earned inside a stocks and shares ISA, are completely free of income tax and capital gains tax — permanently. This means every pound of interest stays in the account, compounding the full balance rather than the post-tax amount. Over long periods, this tax-free compounding advantage compounds substantially. The annual ISA allowance is £20,000 per person for the 2025/26 tax year.

Pension contributions add a further layer of compounding advantage: income tax relief on contributions effectively reduces the cost of investing, meaning the actual return relative to the net cost is significantly higher than the nominal rate. For a basic rate taxpayer contributing £800 to a pension, the government adds £200 in tax relief, making the effective return on the £800 invested equivalent to earning on £1,000. This 25% uplift on day one, compounded over decades, makes pension investing particularly powerful for long-term wealth building.

The most effective strategy for maximising compound interest in the UK in 2026 combines both wrappers: maximise the ISA allowance first for accessible long-term savings, and pension contributions for retirement savings where the tax relief is most valuable. All compounding growth inside both wrappers is entirely tax-free, allowing the full mathematical force of compound interest to operate without the drag of annual tax deductions reducing the balance on which future interest is calculated.

Conclusion

Compound interest is the most important mathematical concept in personal finance — and understanding it fully transforms how you approach both saving and borrowing. For savers and investors, it is the force that turns patient, consistent deposits into significant wealth over time: £10,000 left at 4% for 40 years becomes £48,010 through compound interest, versus just £26,000 under simple interest. The person who saves £100 per month for 10 years starting at age 20 accumulates £150,000 more by age 60 than the person who saves the same amount for 30 years starting at age 30 — not from skill or higher returns, but from the compounding of time.For borrowers, the same force operates in reverse. A £2,000 credit card balance at 22% APR, left unrepaid, grows to over £16,000 in 10 years through compound interest — the same mathematical process that builds wealth for the patient saver destroys financial stability for the habitual minimum-payment maker. Recognising compound interest as a force working simultaneously in two directions — for those who save and against those who borrow — is the practical wisdom that separates disciplined financial management from a lifetime of interest payments.

In 2026, the tools to harness compound interest in the UK are accessible and well-structured: easy-access savings accounts at 4.5%-5.2% AER, fixed-rate bonds at up to 5.3%, cash ISAs providing tax-free compounding, stocks and shares ISAs for long-term equity compound growth, and pension wrappers with upfront tax relief that turbocharges the effective return from day one. The mathematics of compounding does not require exceptional rates or large starting sums. It requires time and discipline: starting early, contributing regularly, leaving the balance untouched to compound, and keeping the growth sheltered from tax in an ISA or pension. These are the habits through which ordinary savings become extraordinary outcomes over ordinary lifetimes.

Frequently Asked Questions (FAQ)

What is compound interest in simple terms?

Compound interest is interest earned on both your original deposit and on any interest you have already earned. Once interest is added to your savings balance, that interest immediately starts earning further interest itself. It is sometimes called 'interest on interest.' The result is that your savings grow faster over time, and the rate of growth accelerates — because every year, the amount on which interest is calculated is larger than the year before. On a £5,000 deposit at 4% AER, year one's interest is £200. Year two's interest is £208 (because it is now calculated on £5,200 rather than £5,000). Year three's is slightly more again. This self-reinforcing cycle is what makes compound interest fundamentally different from simple interest, which is always calculated only on the original deposit.What is the difference between compound and simple interest?

Simple interest is calculated only on the original principal, every period, with no accumulation. If you deposit £1,000 at 10% simple interest, you earn exactly £100 per year, every year, regardless of how long the money is held. After 10 years, you have £2,000 (£1,000 + £1,000 in interest). Compound interest calculates each period's interest on the running total — including all previously earned interest. The same £1,000 at 10% compounding annually earns £100 in year one, £110 in year two (on £1,100), £121 in year three (on £1,210), and so on. After 10 years, you have £2,593.74 — over £593 more than simple interest, from the same rate and the same starting amount. After 20 years, the compound balance is £6,727 versus £3,000 for simple interest — more than twice as much. Simple interest is rarely used in UK savings accounts; almost all savings accounts use compound interest.What is AER and why does it matter for comparing savings accounts?

AER stands for Annual Equivalent Rate. It is the standardised measure that shows the effective annual return on a savings account after accounting for the compounding frequency. All UK savings accounts are required to display their AER, making it the correct metric for comparing accounts. Two accounts might appear identical if you only look at their headline interest rate — but if one compounds monthly and the other annually, the monthly-compounding account has a slightly higher AER because interest is added to the balance more often, giving each increment slightly more time to earn further interest. A 4% rate compounded monthly has an AER of approximately 4.074%. When comparing savings accounts, always compare AER figures directly. The headline rate and the AER will be the same only if the account compounds annually.How does compound interest work on credit card debt?

On credit card debt, compound interest works against the borrower in exactly the same way it works for the saver — but in reverse. Each month, interest is added to the outstanding balance. In the following month, interest is then charged on the larger balance including the unpaid interest from the previous month. If you never make any repayment, a £2,000 credit card balance at 22% APR grows to over £16,000 in 10 years through compound interest. Even making only the minimum repayment each month keeps the balance high for much longer than most borrowers realise, because a small repayment at 22% APR barely reduces the principal while interest continues to compound on most of the balance. The only way to avoid paying compound interest on credit card debt is to clear the full balance every month before interest is charged. If that is not possible, pay as much above the minimum as you can, every month, to reduce the balance on which compound interest is calculated.What is the Rule of 72 and how do I use it?

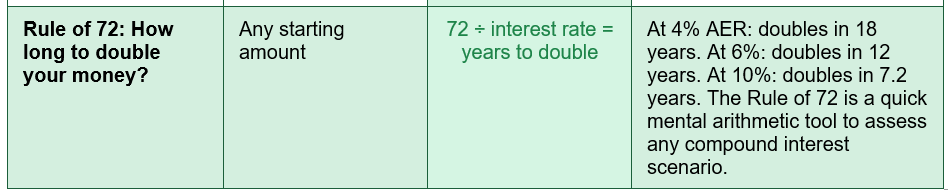

The Rule of 72 is a quick mental arithmetic shortcut for estimating how long it will take for a sum of money to double under compound interest. Divide 72 by the annual interest rate (as a percentage), and the result is approximately the number of years it takes to double. Examples: at 4% AER, 72 ÷ 4 = 18 years to double. At 6%, 72 ÷ 6 = 12 years. At 8%, 72 ÷ 8 = 9 years. At 10%, 72 ÷ 10 = 7.2 years. The Rule of 72 works in both directions: a 22% APR credit card debt doubles in approximately 72 ÷ 22 = 3.3 years without repayment. The rule is an approximation but is accurate enough for most personal finance planning purposes. It is particularly useful for quickly assessing whether a savings rate is sufficient to protect against inflation, or how quickly a debt will grow if not actively repaid.

External References

1. Unbiased — Compound Interest Calculator UK: Daily, Monthly, Yearly (3 weeks ago)https://www.unbiased.co.uk/discover/personal-finance/savings-investing/compound-interest-calculator

2. Aviva — What Is Compound Interest? How It Works for Savings (April 2026)

https://www.aviva.co.uk/investments/savings-accounts/knowledge-centre/what-is-compound-interest/

3. NatWest — What Is Compound Interest? (May 2026)

https://www.natwest.com/savings/savings-guides/what-is-compound-interest.html

4. Equifax UK — Explaining Compound Interest (early vs late saving research)

https://www.equifax.co.uk/resources/loans-and-credit/explaining-compound-interest.html

5. MoneyfactsCompare — Compound Interest Savings Accounts: How Do They Work? (October 2025)

https://moneyfactscompare.co.uk/savings-accounts/guides/what-does-compound-interest-mean/

6. Fast Loan UK — What Is Compound Interest and Why It Matters for Saving and Borrowing (1 month ago — credit card compound interest example)

https://www.fastloanuk.co.uk/blog/what-is-compound-interest-and-why-it-matters-for-saving-and-borrowing/

7. UK Calculator — Interest Rate Calculator UK 2025/26: Simple and Compound Interest (updated March 2026)

https://ukcalculator.com/interest-rate-calculator.html

8. MoneyHelper — Savings and Interest: Understanding How Your Money Grows

https://www.moneyhelper.org.uk/en/savings/types-of-savings/savings-accounts

0 Comments Comments