Real Estate

How to Get on the Property Ladder in (UK)

Table of Contents

- The Current Property Ladder Landscape: Key Statistics

- Stamp Duty Relief: What First-Time Buyers Actually Pay

- The Lifetime ISA: A 25% Government Bonus on Your Deposit Savings

- The Mortgage Guarantee Scheme: Buying With a 5% Deposit

- Shared Ownership: Buying a Share, Renting the Rest

- The First Homes Scheme: Permanent Discounts for Local Buyers

- Comparing Your Routes Onto the Property Ladder

- Building Your Property Ladder Plan: A Step-by-Step Approach

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Getting onto the property ladder remains one of the most significant financial milestones for adults in the UK — and, for many, one of the most daunting. With the average UK house price sitting at around £290,000 and average earnings rising more slowly than property prices over the past two decades, the gap between wanting to buy and being able to buy has widened considerably for an entire generation of prospective first-time buyers.

The encouraging news is that the support landscape for first-time buyers, while it has changed considerably since the closure of the Help to Buy Equity Loan scheme at the end of 2023, remains genuinely substantial. Stamp duty relief, the Lifetime ISA, the Mortgage Guarantee Scheme, Shared Ownership, and the First Homes Scheme together provide multiple legitimate routes for buyers with limited savings, modest incomes, or both to move from renting into ownership — often faster than they might assume.

This guide walks through every major scheme and strategy currently available, the actual numbers behind deposit requirements and stamp duty thresholds, how to build a realistic savings and mortgage plan, and the practical mistakes that most commonly derail first-time buyers. Whether you are just beginning to think about buying or actively saving toward a deposit, this guide is designed to give you a clear, current, and actionable roadmap.

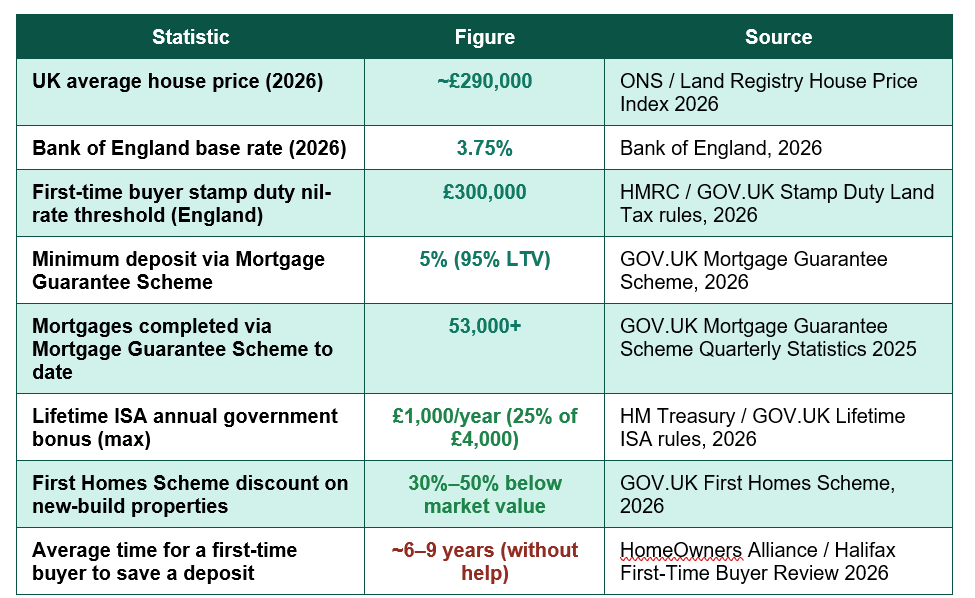

The Current Property Ladder Landscape: Key Statistics

Before exploring specific schemes, it helps to understand the scale of the challenge and the support actually available right now:

Average time to save a deposit unassisted: 6–9 years — for a typical first-time buyer relying solely on personal savings without using government schemes — a figure that the schemes covered in this guide are specifically designed to reduce (HomeOwners Alliance / Halifax 2026)

A note on falling interest rates: The Bank of England base rate has fallen to 3.75% in 2026, the lowest level since spring 2023, with further cuts anticipated. This has already begun improving mortgage affordability for first-time buyers compared to the higher-rate environment of 2023-2024, making this a genuinely more favourable moment to plan a purchase than it has been for several years.

Stamp Duty Relief: What First-Time Buyers Actually Pay

Stamp Duty Land Tax (SDLT) is one of the most significant upfront costs in any property purchase in England and Northern Ireland, and first-time buyers benefit from meaningful relief that should be factored into any budget calculation from the outset.As of 2026, first-time buyers pay no stamp duty on the first £300,000 of a property's purchase price. For properties priced between £300,001 and £500,000, the standard 5% rate applies only to the portion above £300,000 — meaning a first-time buyer purchasing a £350,000 home pays 5% on just £50,000 (£2,500), rather than facing the full standard rates that apply to non-first-time buyers. Properties priced above £500,000 do not qualify for first-time buyer relief at all, and standard rates apply to the entire purchase price.

It is worth noting that this £300,000 nil-rate threshold was reduced from a higher £425,000 threshold that applied prior to April 2025 — a change that has had a particularly noticeable impact in higher-cost regions such as London and the South East, where average first-time buyer purchase prices frequently exceed the new threshold. Scotland and Wales operate their own equivalent property transaction taxes (Land and Buildings Transaction Tax and Land Transaction Tax respectively) with different thresholds, so buyers outside England and Northern Ireland should check the relevant devolved guidance.

The Lifetime ISA: A 25% Government Bonus on Your Deposit Savings

The Lifetime ISA (LISA) remains one of the single most valuable tools available to first-time buyers, and one that is significantly underused relative to its value. Available to UK residents aged 18 to 39 when the account is opened, a LISA allows savings of up to £4,000 per year, with the government adding a 25% bonus on top — up to £1,000 of free money annually.The bonus is paid monthly on contributions and can be used toward a first home purchase of up to £450,000, provided the account has been open for at least 12 months before the funds are withdrawn for that purpose. For a buyer saving the maximum £4,000 per year over five years, the LISA bonus alone contributes £5,000 toward a deposit — a meaningful head start that no standard savings account can replicate, since it represents a guaranteed 25% return regardless of market conditions.

Who should think carefully before opening a LISA: The £450,000 property price cap means the LISA is most valuable for buyers targeting properties below this threshold — which covers the large majority of first-time buyer purchases outside London and the most expensive parts of the South East, but excludes many properties in those higher-cost areas. Withdrawing LISA funds for any purpose other than a first home purchase (before age 60) incurs a 25% government withdrawal penalty, which effectively claws back the bonus and a small portion of your own original contribution — so the LISA should only be used by buyers who are reasonably confident they will purchase a qualifying property.

The Mortgage Guarantee Scheme: Buying With a 5% Deposit

For many prospective first-time buyers, the single biggest barrier is not affordability of monthly repayments but the size of the deposit required upfront. The Mortgage Guarantee Scheme directly addresses this by encouraging mortgage lenders to offer 95% loan-to-value (LTV) mortgages — meaning a deposit of just 5% of the purchase price — by having the Government guarantee a portion of the loan to the lender in the event of default.More than 53,000 mortgages have been completed with support from the Mortgage Guarantee Scheme since its launch, according to the Government's own quarterly statistics, demonstrating that this is a well-established and widely used route into homeownership rather than a niche or experimental programme. On a £290,000 property, a 5% deposit requirement equates to £14,500 — a dramatically more achievable target than the £58,000 a 20% deposit would require on the same property, and one that can realistically be reached within two to three years for many savers, particularly when combined with a Lifetime ISA.

The trade-off to understand clearly is that 95% LTV mortgages typically carry higher interest rates than mortgages with larger deposits, reflecting the higher risk lenders take on at lower deposit levels. Buyers using this scheme should budget for a somewhat higher monthly repayment than they would face with a 10% or 15% deposit, and should plan to remortgage onto a better rate once they have built additional equity, either through repayment or property price growth, typically reviewing this option every two to five years as fixed-rate deals expire.

Shared Ownership: Buying a Share, Renting the Rest

Shared Ownership allows buyers to purchase a percentage share of a property — typically between 25% and 75% — while paying subsidised rent to a housing association on the remaining share. This significantly reduces the deposit and mortgage required, since both are calculated only against the share being purchased rather than the property's full value.On a £290,000 property, purchasing a 40% share (£116,000) with a 5% deposit on that share requires just £5,800 upfront — a dramatically lower barrier to entry than buying outright. Over time, buyers can increase their ownership share through a process known as staircasing, gradually buying additional percentages as their finances allow, in some cases working toward full ownership of the property.

Shared Ownership is particularly well suited to buyers in high-cost areas, including much of London and the South East, where outright ownership of an equivalent property would otherwise be unattainable on the deposits and incomes typical of first-time buyers. The scheme is available on both new-build properties and an increasing number of resale Shared Ownership properties, widening the choice available compared to when the scheme primarily covered new developments.

The First Homes Scheme: Permanent Discounts for Local Buyers

The First Homes Scheme offers new-build homes to eligible first-time buyers and key workers at a discount of between 30% and 50% below full market value. Unlike some previous schemes, the discount is permanently attached to the property through a legal restriction, meaning that when the property is eventually resold, it must again be sold at the same percentage discount to a new eligible buyer — preserving affordability for future generations rather than allowing the initial discount to simply convert into windfall profit for the first buyer.Eligibility and availability vary significantly by local authority area, with priority frequently given to local residents, key workers such as NHS staff, teachers, and emergency services personnel, and households below specified income thresholds. Because availability is limited and demand in popular areas can be high, First Homes properties are best approached by registering interest with local housing associations and developers well in advance and monitoring new development announcements in your target area.

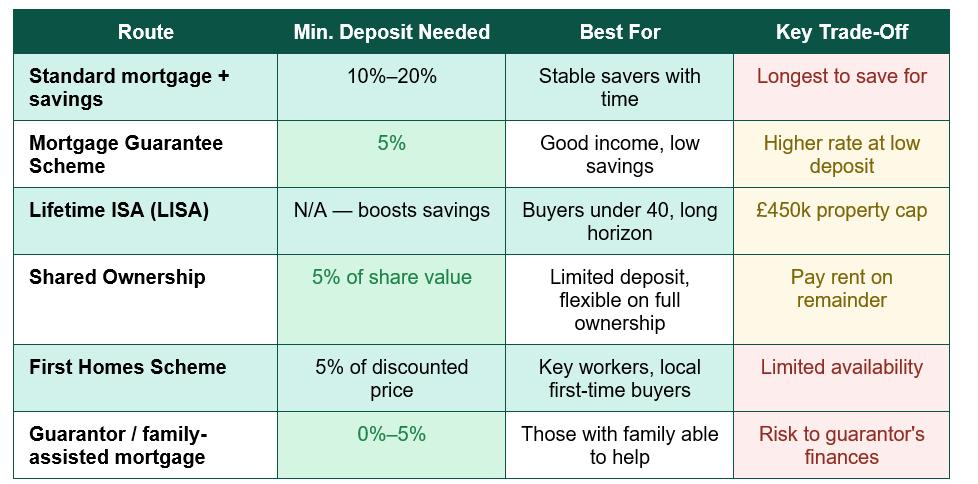

Comparing Your Routes Onto the Property Ladder

The table below compares the main routes covered in this guide, helping you identify which combination of schemes is likely to suit your circumstances:

For many buyers, the most effective approach is not choosing a single route but combining several: using a Lifetime ISA to accelerate deposit savings with a 25% bonus, then applying that deposit toward a Mortgage Guarantee Scheme-backed 95% LTV mortgage, while simultaneously benefiting from first-time buyer stamp duty relief on the purchase itself. This layered approach is how many successful first-time buyers in 2026 are bridging what would otherwise be an unworkable affordability gap.

Building Your Property Ladder Plan: A Step-by-Step Approach

Bringing the schemes and numbers together, the following sequence provides a practical framework for building your own plan to get on the property ladder:- Check and improve your credit file: Lenders assess credit history closely, and even minor improvements — registering on the electoral roll, paying down small existing debts, avoiding new credit applications in the months before applying — can improve the mortgage rates and amounts you are offered.

- Open a Lifetime ISA as early as possible if eligible: The earlier you start, the more years of the 25% bonus you capture. Even modest monthly contributions compound meaningfully over several years, and there is no minimum monthly contribution required to keep the account active.

- Get a realistic affordability assessment from a mortgage broker: A whole-of-market mortgage broker, ideally one regulated by the Financial Conduct Authority and experienced specifically with first-time buyers, can model your actual borrowing capacity across multiple scheme combinations and lenders, often identifying options a buyer would not find independently.

- Research scheme availability in your target area: First Homes and Shared Ownership availability vary considerably by location. Contact local housing associations and check Help to Buy agent websites (now repurposed to support the remaining live schemes) for current listings in the areas you are considering.

- Budget for costs beyond the deposit: Stamp duty (where applicable above the nil-rate threshold), solicitor and conveyancing fees, surveys, mortgage arrangement fees, and removal costs typically add £3,000 to £6,000 or more on top of the deposit itself — a figure first-time buyers frequently underestimate.

- Get a mortgage in principle before house hunting seriously: This confirms your realistic budget, strengthens your position when making offers, and avoids the disappointment of falling in love with a property outside your actual affordability range.

Conclusion

Getting on the property ladder in 2026 is genuinely more achievable than the headline affordability statistics might initially suggest — provided prospective buyers understand and actively use the support available to them. Stamp duty relief, the Lifetime ISA's 25% savings bonus, the Mortgage Guarantee Scheme's 5% deposit mortgages, Shared Ownership, and the First Homes Scheme each address a different part of the affordability challenge, and the most successful buyers typically combine several of these tools rather than relying on a single route.Falling interest rates, with the Bank of England base rate now at 3.75% and further cuts anticipated, have also begun to ease the mortgage affordability pressure that made the 2023-2024 period particularly difficult for new buyers. Combined with the home buying and selling reforms the Government has separately committed to rolling out over this Parliament — designed to make the purchase process itself faster, cheaper, and less likely to collapse partway through — the overall environment for first-time buyers is showing genuine signs of improvement after several challenging years.

The path onto the property ladder is rarely a single decision but a sequence of deliberate steps: building genuine savings momentum as early as possible, understanding which schemes you qualify for and where they are available, getting expert mortgage advice early enough to shape your strategy rather than simply react to what a single lender offers, and budgeting honestly for the full cost of a purchase beyond the deposit alone. Approached this way, the property ladder — while still a genuine financial stretch for most first-time buyers — is a realistic and achievable goal rather than an indefinitely distant one.

Frequently Asked Questions (FAQ)

What is the minimum deposit I need to buy my first home in 2026?

With the Mortgage Guarantee Scheme, the minimum deposit is 5% of the purchase price. Through Shared Ownership, the effective deposit can be even lower in pound terms, since it is calculated against the share you are purchasing rather than the full property value. Standard mortgages without scheme support typically require a minimum of 10%, with the most competitive interest rates generally reserved for deposits of 15-20% or more.Can I use a Lifetime ISA alongside the Mortgage Guarantee Scheme?

Yes. The Lifetime ISA is a savings vehicle used to help you build your deposit, while the Mortgage Guarantee Scheme affects what loan-to-value mortgage your lender is willing to offer once you have that deposit. The two are entirely complementary: a buyer might use a LISA over several years to build a 5% deposit (boosted by the 25% government bonus), then use that deposit to access a 95% LTV mortgage backed by the Mortgage Guarantee Scheme.Do I have to pay stamp duty as a first-time buyer?

Not on the first £300,000 of the purchase price in England and Northern Ireland. If the property costs between £300,001 and £500,000, you pay the standard 5% rate only on the portion above £300,000. Properties above £500,000 do not qualify for first-time buyer relief, and standard stamp duty rates apply to the full price. Scotland and Wales have their own separate property transaction taxes with different thresholds and rates.Is Shared Ownership a good idea, or is it better to save for a full deposit?

This depends on your individual circumstances, particularly your local property prices relative to your income and savings rate. Shared Ownership makes sense for buyers who want to stop renting and start building equity sooner, particularly in high-cost areas where saving a full deposit could otherwise take a decade or more. The trade-off is that you continue paying rent on the unowned share, and increasing your ownership share later (staircasing) involves additional costs and, in some cases, a fresh property valuation. A mortgage broker experienced with Shared Ownership can model both scenarios against your specific numbers.How has the recent home buying and selling reform announcement affected first-time buyers?

The UK Government's home buying and selling reforms, announced in June 2026, are separate from the deposit and affordability schemes covered in this guide, but are designed to be complementary. The reforms target the purchase process itself — introducing mandatory upfront sales packs, earlier binding agreements, and digital tools intended to cut typical transaction times by around four weeks and save first-time buyers an average of £650 per transaction in reduced costs and fewer collapsed sales. These reforms are being rolled out in phases over the rest of this Parliament rather than taking effect immediately, but they are expected to make the process of actually completing a purchase faster and less risky once buyers have secured their deposit and mortgage.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. GOV.UK — Mortgage Guarantee Scheme Quarterly Statistics

https://www.gov.uk/government/statistics/mortgage-guarantee-scheme-quarterly-statistics

2. GOV.UK — Lifetime ISA Overview and Rules

https://www.gov.uk/lifetime-isa

3. GOV.UK — First Homes Scheme

https://www.gov.uk/affordable-home-ownership-schemes/first-homes

4. GOV.UK — Shared Ownership Homes

https://www.gov.uk/affordable-home-ownership-schemes/shared-ownership-homes

5. HM Revenue & Customs — Stamp Duty Land Tax: Relief for First-Time Buyers

https://www.gov.uk/stamp-duty-land-tax/relief-for-first-time-buyers

6. Bank of England — Official Bank Rate History and Monetary Policy Decisions

https://www.bankofengland.co.uk/monetary-policy/the-interest-rate-bank-rate

7. HomeOwners Alliance — Government House Buying Schemes Guide

https://hoa.org.uk/advice/guides-for-homeowners/i-am-buying/government-schemes-help-buy-home/

8. Office for National Statistics (ONS) — UK House Price Index

https://www.ons.gov.uk/economy/inflationandpriceindices/bulletins/housepriceindex/latest

0 Comments Comments