Investing

What Is a Discounted Cash Flow? Complete Guide

Table of Contents

- Valuing a Business on Its Own Merits

- What Is a Discounted Cash Flow (DCF)?

- The Time Value of Money: The Foundation of DCF

- The DCF Formula Explained

- The Five Core Components of a DCF Model

- WACC: The Discount Rate That Everything Depends On

- Step-by-Step DCF Worked Example

- Terminal Value: The Most Important and Most Uncertain Number

- DCF vs Other Valuation Methods: When to Use Each

- DCF Limitations: The Honest Assessment

- When to Use DCF: Practical Applications in 2026

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Valuing a Business on Its Own Merits

When Goldman Sachs valued Twitter before Elon Musk's acquisition, when Warren Buffett decides whether to purchase a stake in a business, when a private equity firm decides how much to pay for a company, and when an equity analyst sets a price target for a listed stock, the analysis almost always starts with the same foundational question: what are this business's future cash flows worth in today's money? The answer to that question is a Discounted Cash Flow analysis, universally abbreviated to DCF.The DCF is the most rigorous and most theoretically sound valuation method in corporate finance. It values a business not by what similar companies trade at in the market, not by what acquirers paid for comparable businesses in past deals, and not by accounting earnings that can be distorted by different accounting choices. It values a business by its fundamental economic reality: the cash it is capable of generating for its owners over its remaining life, translated into what that future cash is worth in today's money using a rate that reflects the risk of receiving it.

This guide explains everything about DCF: the time value of money concept that underpins it, the complete formula and its five components, how WACC is calculated and why it matters so much, the critical but often misunderstood role of terminal value, a step-by-step worked example, the comparison to alternative valuation methods, the significant limitations and failure modes of DCF analysis, and when to use it versus when to reach for a different approach. Whether you are an investor, a business owner, a finance student, or simply someone who wants to understand how investment professionals measure value, this guide provides the complete picture.

What Is a Discounted Cash Flow (DCF)?

A discounted cash flow is a valuation method that estimates the present value of an investment — a company, a project, a property, or any other asset — based on the cash flows it is expected to generate in the future. The word 'discounted' is the key: because a pound received in the future is worth less than a pound received today, future cash flows must be reduced — discounted — to their equivalent present value before they can be compared to the price being paid for the investment today.The logic is captured precisely by Harvard Business School Professor Suraj Srinivasan in the online course Strategic Financial Analysis: 'A DCF analysis is useful when investing money now and expecting some rewards in the future. A DCF analysis finds the intrinsic value of a business, which is the present value of the free cash flow the company is expected to pay its shareholders in the future. If the intrinsic value is higher than the current price, it could be a good investment opportunity.'

Warren Buffett — perhaps the world's most celebrated practitioner of value investing — described the DCF concept in his own words: 'Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.' This definition, from one of history's most successful investors, encapsulates precisely what DCF measures: not earnings, not book value, not revenue — the actual cash that can be extracted from the business, translated into its present-day value.

Why DCF matters: intrinsic value vs market price: DCF produces an absolute value independent of market sentiment — the same company may be worth buying at £40 but not at £60 — Dr. Andrew Stotz (March 2026) explains: 'DCF is the most widely used intrinsic valuation method in investment banking, equity research, and corporate finance because it values a business based on its own fundamentals, not what the market says it's worth.' This independence from market sentiment is DCF's most important distinguishing feature — it gives investors a benchmark against which to assess whether a market price represents a bargain, fair value, or overvaluation (Valuation Master Class, March 2026)

The Time Value of Money: The Foundation of DCF

The entire DCF methodology rests on a single foundational principle called the time value of money — the observation that a pound today is worth more than a pound received at some point in the future. This is not a matter of inflation alone (though inflation contributes). It is a matter of opportunity and risk.A pound today is worth more than a pound next year for two reasons. First, opportunity cost: a pound today can be invested and will generate a return — so a pound today can become more than a pound by next year. If you can invest at 10% per year, then £1 today is worth £1.10 in one year. A promise to receive £1 in one year is therefore worth only £0.909 today (£1 ÷ 1.10), because you would need only £0.909 invested today at 10% to have £1 in one year. Second, risk: a pound promised in the future carries the risk that it may not actually arrive — the company may perform worse than expected, go bankrupt, or face circumstances that prevent it from delivering the promised cash flow. Future cash flows are inherently less certain than cash in hand.

Ramp.com's DCF guide (April 2026) states this plainly: 'This is the heart of DCF: a dollar promised in the future isn't worth a dollar today. If someone promises you $100 next year, you wouldn't pay $100 for that promise today — you'd pay less, because you could invest that money elsewhere (opportunity cost) and because there's a chance you don't actually receive the $100 (risk). The discount rate captures both of those forces.'

The discount rate in a DCF model is the mathematical expression of these two forces: it represents the return you could earn on an investment of similar risk (opportunity cost) and the compensation required for the uncertainty of the cash flows. The higher the risk of a business, the higher its discount rate, and the less today's money a given future cash flow is worth.

The apple tree analogy (Harvard Business School): Imagine you are considering buying an apple tree for $200. You estimate it will generate $100 in free cash flow per year and want to know if this is a better investment than alternatives. If your discount rate is 10%, the present value of year one's $100 is $90.91. Year two's $100 is worth $82.64. And so on. If the total present value of all the tree's future cash flows exceeds $200, it is worth buying at that price. If it is less, you would need to pay below $200 to earn your required 10% return. This is the DCF framework applied to the simplest possible real asset — and it scales to the valuation of any business, large or small (Harvard Business School, 'Discounted Cash Flow', 2025).

The DCF Formula Explained

The DCF formula calculates intrinsic value by summing the present value of all projected future free cash flows plus the terminal value that represents all cash flows beyond the explicit forecast period:DCF Value = CF₁/(1+r)¹ + CF₂/(1+r)² + CF₃/(1+r)³ + ... + CFₙ/(1+r)ⁿ + Terminal Value/(1+r)ⁿ

• CF₁, CF₂ … CFₙ = Free Cash Flow in each forecast year

• r = the discount rate (typically WACC — Weighted Average Cost of Capital)

• n = number of forecast years in the explicit period

• t = each individual year (1, 2, 3 … n)

• Terminal Value = the estimated value of all cash flows beyond year n

Each cash flow is divided by (1+r) raised to the power of the year number. This is the discounting operation: it calculates what a future cash flow is worth today given the required return rate r. Year one's cash flow is divided by (1+r)¹; year five's by (1+r)⁵; year ten's by (1+r)¹⁰. Because (1+r)^t grows exponentially with time, cash flows further in the future are worth progressively less in today's money — reflecting the increasing uncertainty and opportunity cost of waiting longer.

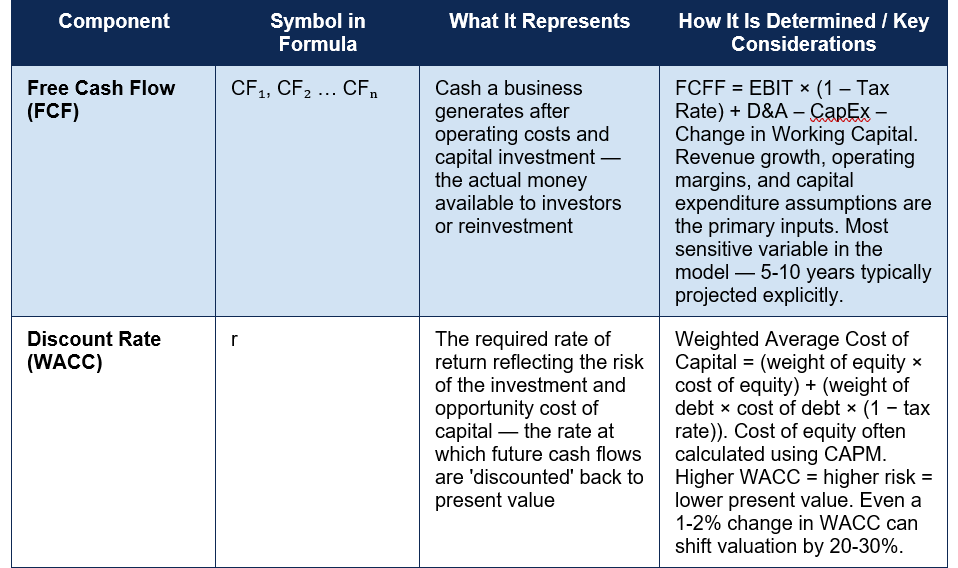

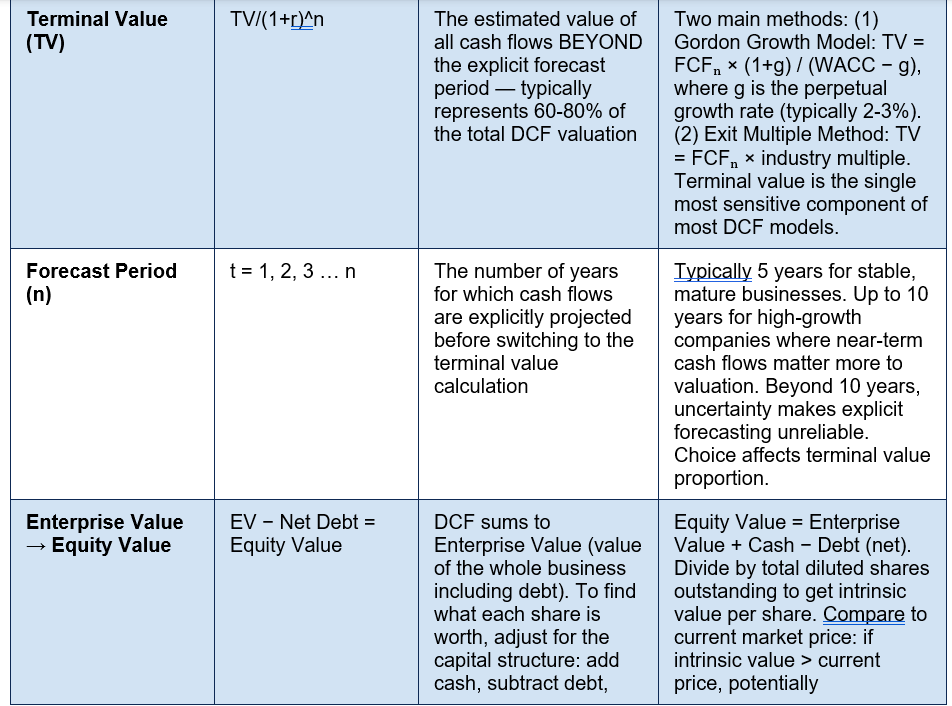

The Five Core Components of a DCF Model

Every DCF analysis, whether a simple napkin calculation or a complex investment banking model, contains five fundamental components. Understanding each is essential for building, reading, or critiquing a DCF:Component Symbol in Formula What It Represents How It Is Determined / Key Considerations

Free Cash Flow (FCF) CF₁, CF₂ … CFₙ Cash a business generates after operating costs and capital investment — the actual money available to investors or reinvestment FCFF = EBIT × (1 – Tax Rate) + D&A – CapEx – Change in Working Capital. Revenue growth, operating margins, and capital expenditure assumptions are the primary inputs. Most sensitive variable in the model — 5-10 years typically projected explicitly.

WACC: The Discount Rate That Everything Depends On

The Weighted Average Cost of Capital (WACC) is the discount rate used in the vast majority of corporate DCF models, and it is the single most consequential input in the analysis. Small changes in WACC produce large changes in the DCF value. Understanding what WACC is and how it is calculated is therefore essential to understanding the reliability and limitations of any DCF model.WACC represents the blended cost of capital for the business — the average return that both equity investors and debt lenders expect to receive for providing capital to the company, weighted by the proportion of each in the capital structure:

WACC = (E/V × Re) + (D/V × Rd × (1 – Tax Rate))

• E = market value of equity; D = market value of debt; V = E + D (total capital)

• Re = cost of equity (typically calculated using the Capital Asset Pricing Model: Re = Risk-Free Rate + Beta × Equity Risk Premium)

• Rd = cost of debt (the interest rate the company pays on its borrowing)

• (1 – Tax Rate) adjusts for the tax deductibility of interest payments

The WACC reflects the riskiness of the business. A large, stable utility company with predictable regulated revenues might have a WACC of 5% to 7%. A high-growth technology startup with no guaranteed revenues might have a WACC of 15% or more. The higher the WACC, the more aggressively future cash flows are discounted — and the lower the resulting intrinsic value for any given set of cash flow projections. This is the formal mathematical expression of the intuition that riskier businesses are worth less than safer ones.

Corporate Finance Institute's formula guide (April 2026) illustrates the sensitivity: a DCF model with a 12% WACC that projects a business at $500 million might produce a value of only $350 million at a 15% WACC, or $750 million at a 9% WACC. The same cash flow projections, three very different values — all from a 3-percentage-point change in the discount rate. This sensitivity is one of the primary reasons DCF models must always be accompanied by sensitivity analysis.

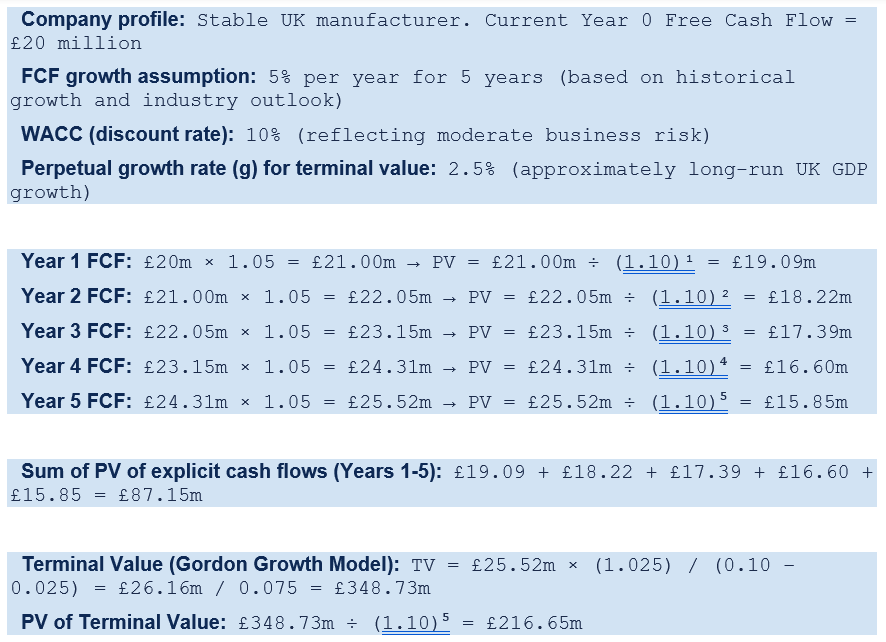

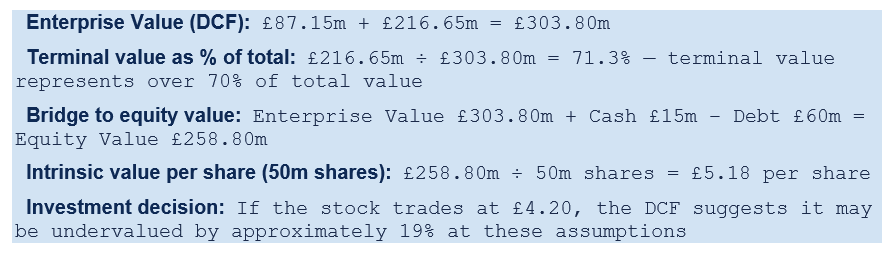

Step-by-Step DCF Worked Example

The following example constructs a simplified 5-year DCF for a hypothetical UK manufacturing company to illustrate the complete calculation process:

Terminal Value: The Most Important and Most Uncertain Number

The worked example above reveals one of the most important and most frequently misunderstood features of DCF analysis: the terminal value typically represents the majority of the total valuation — in the example above, 71.3%. Across a wide range of real-world DCF analyses, the terminal value accounts for 60% to 80% or more of the total enterprise value. This means that the entire analytical effort of projecting five or ten years of detailed free cash flows produces only 20% to 40% of the final number, while the assumptions embedded in a single terminal value calculation drive the majority of the output.The terminal value is calculated using one of two principal methods. The Gordon Growth Model (also called the perpetuity growth method) assumes that cash flows grow at a constant rate g forever from the end of the forecast period: Terminal Value = FCFₙ × (1+g) / (WACC − g). The perpetual growth rate g must be below the long-run economic growth rate of the economy — typically 1.5% to 3% for developed economies. Choosing a g above GDP growth implies the company will eventually be larger than the entire economy, which is arithmetically impossible in the long run. The exit multiple method alternatively uses an industry valuation multiple (typically EV/EBITDA) applied to the final year's EBITDA to estimate the value at which the business could be sold at the end of the forecast period.

THE TERMINAL VALUE WARNING: Because terminal value represents 60-80% of a DCF result, small changes in the perpetual growth rate (g) or WACC produce very large changes in the total valuation. Changing g from 2.5% to 3.0% in the example above (WACC 10%) changes the TV denominator from 7.5% to 7.0%, producing a terminal value of £373.7m versus £348.7m — a £25m increase in terminal value just from a 0.5% change in g. This is why Jainam (4 days ago) notes: 'The model is incredibly sensitive, and slight tweaks to growth or terminal value assumptions can radically alter the final valuation.'

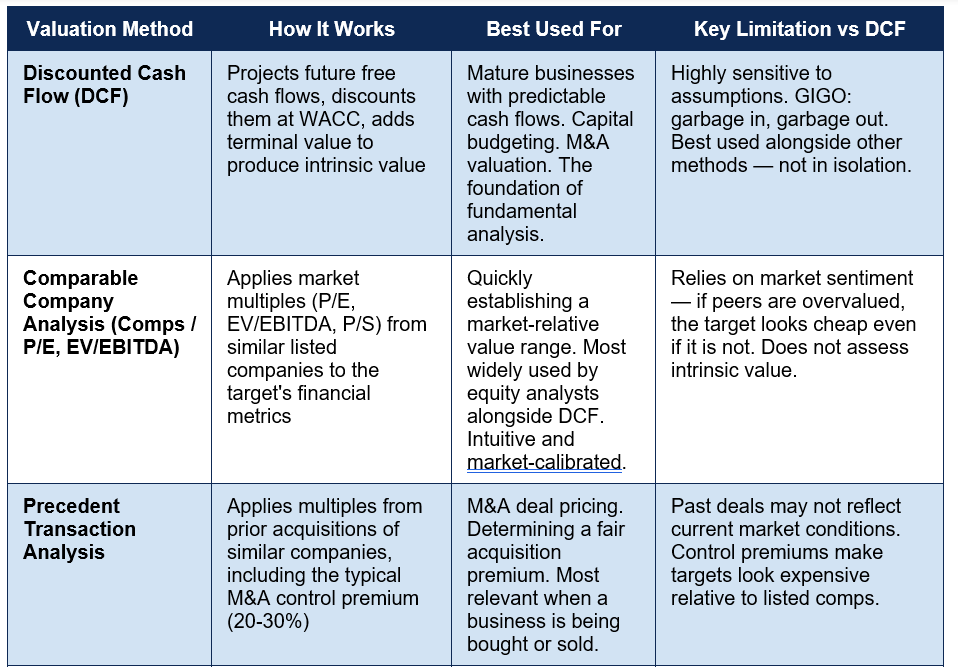

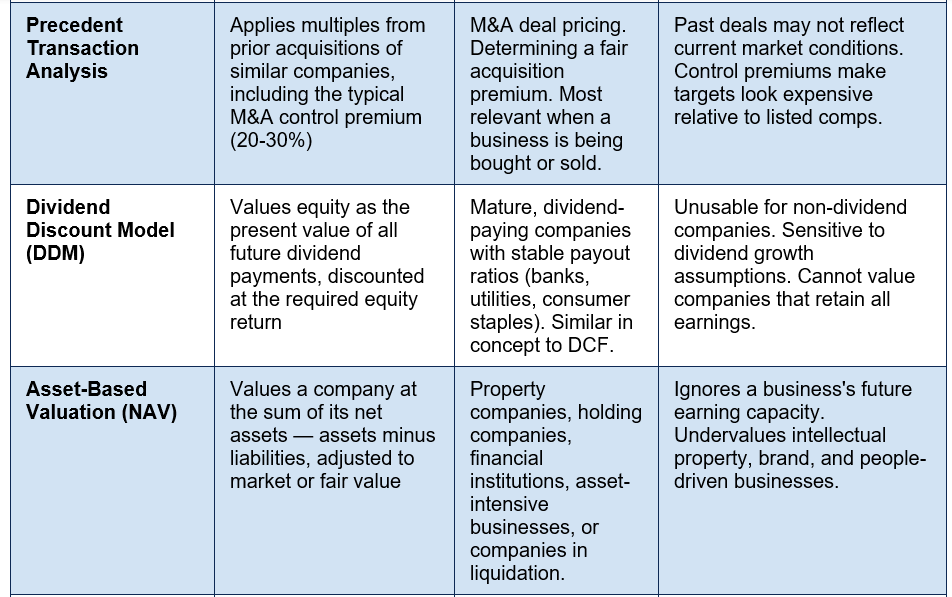

DCF vs Other Valuation Methods: When to Use Each

In practice, professional investors and analysts rarely rely on DCF in isolation. A complete valuation typically uses DCF as the primary intrinsic value anchor and cross-checks it against relative valuation methods to assess whether the DCF output is consistent with what the market charges for comparable businesses. The table below maps the major valuation methods against their applications, strengths, and limitations relative to DCF:

DCF Limitations: The Honest Assessment

DCF is the most rigorous valuation method in corporate finance — and it is also the most sensitive to error, the most dependent on assumptions that cannot be known with certainty, and the most prone to producing a precise-looking number that is highly imprecise in practice. Understanding the limitations is as important as understanding the methodology itself.- Garbage in, garbage out (GIGO): The accuracy of a DCF valuation depends entirely on the accuracy of its inputs — principally the free cash flow projections, the WACC, and the terminal growth rate. If any of these is significantly wrong, the resulting valuation is also wrong — and the model will not tell you that it is wrong. A DCF built with optimistic cash flow projections and a low discount rate can justify almost any price. Valutico (2026) emphasises: 'Just remember, when valuing you are making educated guesses about the future. If you get these educated guesses wildly incorrect, then your valuation will likely also be off.'

- Extreme sensitivity to discount rate: As demonstrated in the WACC section, a 1% to 2% change in the discount rate can shift the DCF value by 20% to 40%. The cost of equity within WACC (calculated using CAPM) itself depends on the risk-free rate, the equity risk premium, and the company's beta — all of which involve significant judgement and change over time. In 2026, with interest rates higher than they were in 2020-2021, the same cash flow projections produce much lower DCF values than they would have at near-zero interest rates.

- Terminal value dominates and is most uncertain: The component that contributes 60-80% of the total DCF value — the terminal value — is also the most uncertain, because it represents cash flows stretching into perpetuity. The perpetual growth rate g and the WACC at which it is discounted are both estimates that will certainly be wrong over infinite time. Small errors in either, compounded over a conceptual infinity, produce large errors in terminal value.

- Unusable for companies without predictable cash flows: Companies with no operating history, loss-making startups, early-stage growth companies, businesses in cyclical industries near a trough, and businesses undergoing major restructuring are all difficult to value using DCF because there is no reliable foundation for projecting the future cash flows on which the entire analysis depends. For these businesses, alternative methods including comparable company analysis, price-to-sales ratios, or scenario-based option pricing models are more appropriate.

- Circularity in WACC: WACC uses the market value of equity as part of its capital structure weighting — but the market value of equity depends on the DCF valuation itself. This creates a circular reference that requires iteration to resolve precisely. In practice, most analysts use the current market value or an iterative approach, accepting some degree of approximation.

DCF IS NOT A SINGLE NUMBER: One of the most dangerous misapplications of DCF analysis is treating the output — the intrinsic value per share — as a precise, reliable answer. Every DCF is a point estimate in a distribution of possible values, each corresponding to a different combination of assumptions. Professional analysts always accompany DCF with sensitivity analysis — a table showing how the intrinsic value changes across a range of WACC and growth rate assumptions. The output should be presented as a value range ('intrinsic value of approximately £4.50 to £6.00 per share') not as a single number ('intrinsic value of £5.18'). A model that produces six significant figures of precision while resting on assumptions that could reasonably vary by ±2% is offering false precision that can mislead as much as it informs.

When to Use DCF: Practical Applications in 2026

DCF is most useful in specific contexts where its strengths outweigh its limitations, and least useful in contexts where its assumptions are fundamentally unworkable:- Mature businesses with stable, predictable cash flows: Established businesses in stable industries — consumer staples, utilities, telecoms, industrials — with several years of operating history and predictable capital expenditure requirements are the natural home of DCF analysis. The cash flows can be projected with reasonable confidence, and the terminal growth rate assumption is grounded in industry dynamics.

- Capital budgeting decisions: Businesses use DCF (in the form of NPV — Net Present Value — which is simply DCF minus the initial investment) to evaluate whether to proceed with major investments: new factories, acquisitions, technology systems, geographic expansions. If the NPV of a project is positive at the company's required rate of return (WACC), the project adds value; if negative, it destroys value relative to the alternative of not investing.

- Mergers and acquisitions: Investment banks use DCF as part of their fairness opinion analysis when advising on acquisitions. Dr. Andrew Stotz (March 2026) notes that Goldman Sachs used DCF methodology in valuing Twitter. The DCF provides an intrinsic value anchor alongside the transaction multiples from comparable acquisitions.

- Portfolio investment decisions: Fundamental long-term investors — value investors in the tradition of Buffett and Graham — use DCF to identify stocks trading below their intrinsic value. StockTitan's DCF guide (June 2026) confirms: 'Warren Buffett relies heavily on DCF principles. He famously said: Intrinsic value can be defined simply: It is the discounted value of the cash that can be taken out of a business during its remaining life.'

- NOT suitable: high-growth startups or loss-making companies: For companies with no operating history, significant losses, or cash flows that are highly uncertain and years away, DCF either produces wildly optimistic values (if growth assumptions are optimistic) or no value at all (if near-term cash flows are deeply negative). Alternative approaches are needed.

Conclusion

The discounted cash flow analysis is the foundation of fundamental investment valuation — the methodology that answers the most important question in finance: what is this business actually worth based on the cash it can generate? Its theoretical basis is the time value of money: future cash flows are worth less than present cash, and the rate at which they are discounted reflects both the opportunity cost of capital and the risk of the business. Sum those discounted cash flows across an explicit forecast period and add a terminal value for all cash flows beyond it, and you arrive at the enterprise value — an intrinsic value independent of market sentiment, comparable multiples, or recent transaction prices.The five components of a DCF — free cash flow, the discount rate (WACC), terminal value, the forecast period, and the enterprise-to-equity value bridge — each carry their own set of assumptions and their own sensitivity to error. Terminal value alone typically represents 60% to 80% of the total DCF result, making the perpetual growth rate and the WACC the two most consequential numbers in any valuation. Even a half-percentage-point change in either can move the intrinsic value per share by 10% or more. This sensitivity is not a reason to avoid DCF — it is a reason to always accompany any DCF with sensitivity analysis that shows the valuation across a range of input assumptions, presenting a value range rather than a false-precision single number.

DCF works best for mature, cash-generative businesses with predictable operations, in capital budgeting decisions with quantifiable cash flows, and in M&A contexts where a rigorous intrinsic value anchor is needed alongside relative valuation. It is less useful for startups, loss-making companies, or businesses with highly uncertain near-term cash flows, where alternative valuation approaches should take precedence. Used correctly — alongside comparable company analysis, with clear assumption documentation, and with sensitivity analysis to define the value range — DCF is the most honest and most intellectually rigorous method for answering the central question of investing.

Frequently Asked Questions (FAQ)

What is a discounted cash flow in simple terms?

A discounted cash flow is a method of calculating what a business or investment is worth today based on the cash it is expected to generate in the future. Because a pound received in the future is worth less than a pound today — due to the opportunity to invest the pound today and earn a return, and the risk that the future cash may not arrive — future cash flows must be 'discounted' to reflect their present-day value. A DCF analysis projects the cash flows a business will generate over the next 5-10 years, discounts each year's cash flow back to its present value using a rate that reflects the risk of the business, adds a terminal value for cash flows beyond the forecast period, and sums all of these to produce the total intrinsic value of the business.What is WACC and why does it matter in a DCF?

WACC (Weighted Average Cost of Capital) is the discount rate used in most DCF models. It represents the blended cost of funding a business — combining what equity investors expect to earn (the cost of equity, typically calculated using the Capital Asset Pricing Model) with what debt lenders charge in interest (the cost of debt, adjusted for tax), weighted by the proportion of each in the capital structure. WACC matters enormously in DCF because it is the rate at which future cash flows are discounted back to present value. A higher WACC (reflecting a riskier business or higher market interest rates) means future cash flows are worth less today, producing a lower intrinsic value. A 1% to 2% change in WACC can shift the DCF output by 20% to 40%, making it the single most consequential input in the model.What is terminal value in a DCF and why is it so important?

Terminal value is the estimate of all the cash flows a business will generate beyond the explicit forecast period (typically after year 5 or year 10). Because businesses are assumed to operate indefinitely, the terminal value captures the value of all future cash flows from the end of the forecast period into perpetuity. It is calculated using either the Gordon Growth Model — which assumes cash flows grow at a constant perpetual rate — or the exit multiple method, which applies an industry valuation multiple to the final year's earnings. Terminal value is critically important because it typically represents 60% to 80% of the total DCF value. This means the assumptions in the terminal value calculation — particularly the perpetual growth rate and the WACC — have more influence on the final answer than all the detailed year-by-year cash flow projections combined.What are the main limitations of DCF analysis?

The primary limitation of DCF is sensitivity to assumptions — small changes in the discount rate, growth assumptions, or terminal value parameters produce large changes in the output. This is the 'garbage in, garbage out' problem: if the cash flow projections or discount rate are materially wrong, the DCF value will also be materially wrong, without the model signalling this. DCF is also not suitable for businesses without predictable cash flows — startups, loss-making companies, and businesses undergoing major restructuring — where the projection foundation is too uncertain to be reliable. Terminal value's dominance of total value (60-80%) means the most uncertain component drives most of the answer. And WACC calculation involves its own layer of assumptions (risk-free rate, equity risk premium, beta) each of which affects the output. These limitations do not make DCF useless — they make it important to always present DCF as a valuation range, always accompany it with sensitivity analysis, and always cross-check it against relative valuation methods.How is DCF different from a P/E ratio?

A P/E ratio (Price-to-Earnings) is a relative valuation metric that compares a company's current stock price to its earnings per share — it tells you how much the market is currently paying for each pound of earnings. DCF is an absolute valuation method that calculates the intrinsic value of a company based on its projected future cash flows, independently of what the market currently charges. The P/E ratio is quick and intuitive but is based on accounting earnings (which can be distorted by accounting choices) and reflects current market sentiment (if the market is broadly overvalued, all P/E ratios will be high even if individual companies are overvalued). DCF is more rigorous — it focuses on actual cash generation, not accounting earnings, and produces a value independent of market mood. Professional analysts typically use both: DCF for intrinsic value and P/E (and other multiples) to cross-check whether the DCF output is consistent with what the market currently values for comparable businesses.External References & Further Reading

1. Valuation Master Class — DCF Valuation: The Complete Guide (Dr. Andrew Stotz, March 30, 2026 — Goldman Sachs Twitter example)https://valuationmasterclass.com/dcf-valuation/

2. StockTitan — DCF Calculator and Formula: Discounted Cash Flow Analysis Guide (Updated June 24, 2026)

https://www.stocktitan.net/articles/dcf-calculator-formula-analysis-guide

3. Valutico — Discounted Cash Flow Analysis: Complete Guide with Examples (1 month ago)

https://valutico.com/discounted-cash-flow-analysis-your-complete-guide-with-examples/

4. Corporate Finance Institute — DCF Formula Guide (Updated April 2026 — WACC and FCF calculation)

https://corporatefinanceinstitute.com/resources/valuation/dcf-formula-guide/

5. Ramp — What Is Discounted Cash Flow? (April 3, 2026 — time value of money and enterprise to equity bridge)

https://ramp.com/blog/business-banking/what-is-discounted-cash-flow

6. Harvard Business School Online — Discounted Cash Flow (DCF) Model (Strategic Financial Analysis course, 2025)

https://online.hbs.edu/blog/post/discounted-cash-flow

7. The Hartford — Discounted Cash Flow: Formula, Examples and Pros and Cons (September 2025)

https://www.thehartford.com/insights-center/finances/discounted-cash-flow

8. Jainam — DCF Valuation Explained: Step-by-Step (4 days ago — sensitivity to discount rate)

https://www.jainam.in/blog/dcf-valuation/

0 Comments Comments