Vehicles & Cars

Why Cars Are Now a Huge Financial Risk for Drivers

Table of Contents

- Introduction

- The Scale of the Problem: Car Finance Statistics (2024)

- The True Cost of Owning a New Car: What Dealers Never Show You

- The 5 Financial Mistakes Drivers Keep Making With Cars

- Mistake 1: Buying More Car Than They Can Afford

- Mistake 2: Rolling Negative Equity Into a New Loan

- Mistake 3: Fixating on Monthly Payment Instead of Total Cost

- Mistake 4: Ignoring the Full Cost of Insurance

- Mistake 5: Treating a Car as an Investment or Status Asset

- The UK Picture: PCP Finance and the Hidden Balloon Payment Trap

- A Smarter Car Strategy: How to Avoid the Financial Trap

- Conclusion

- Frequently Asked Questions (FAQ)

- External References & Further Reading

Introduction

There is a financial mistake so widespread, so normalised, and so relentlessly encouraged by advertising, social pressure, and easy credit that most people who make it never even realise they have done so. That mistake is the modern approach to car ownership — and it is quietly draining the financial futures of millions of households across the United States, the United Kingdom, and beyond.Cars have always been expensive to own. But the combination of soaring vehicle prices, ultra-long loan terms, high insurance premiums, and a cultural obsession with driving new or near-new vehicles has transformed the humble car from a useful asset into one of the most destructive forces in personal finance. The average American now spends more on car-related costs than on food. The average monthly car payment in the US has crossed $738 — a figure that, for many households, exceeds their rent contribution or monthly savings.

This blog post confronts the car financing crisis head-on. It presents the statistics that reveal just how significant the problem has become, exposes the five most common and costly mistakes drivers make when buying and financing vehicles, breaks down the true total cost of car ownership that dealerships never show you, and provides a practical framework for making smarter vehicle decisions that protect rather than undermine your long-term financial health. Whether you are about to buy a car, already locked into a problematic loan, or simply wondering why your money disappears despite a decent income, this guide is for you.

The Scale of the Problem: Car Finance Statistics (2024)

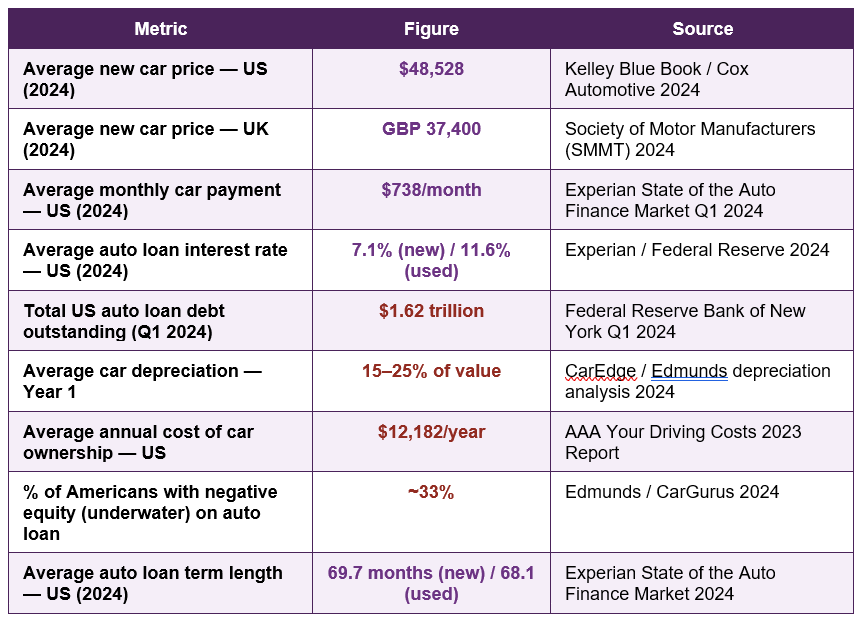

The numbers surrounding car ownership and auto finance in 2024 paint a striking picture of how dramatically the financial landscape of vehicle ownership has shifted. The table below provides the key data:

Total US auto loan debt: $1.62 trillion — surpassing student loan debt in its rate of growth and now the third-largest category of consumer debt (Federal Reserve Bank of NY, Q1 2024)

Average monthly car payment: $738/month — in the US for a new vehicle in 2024 — more than many household utility bills combined (Experian, 2024)

These figures reveal a consumer auto market in structural stress. Prices have risen sharply since 2020, pushed by supply chain disruptions, semiconductor shortages, and post-pandemic demand spikes that permanently reset transaction prices upward. Interest rates have simultaneously climbed to multi-year highs. The result is a generation of car buyers making record monthly payments on vehicles financed over record loan terms — a financially toxic combination that the industry has largely normalised.

The True Cost of Owning a New Car: What Dealers Never Show You

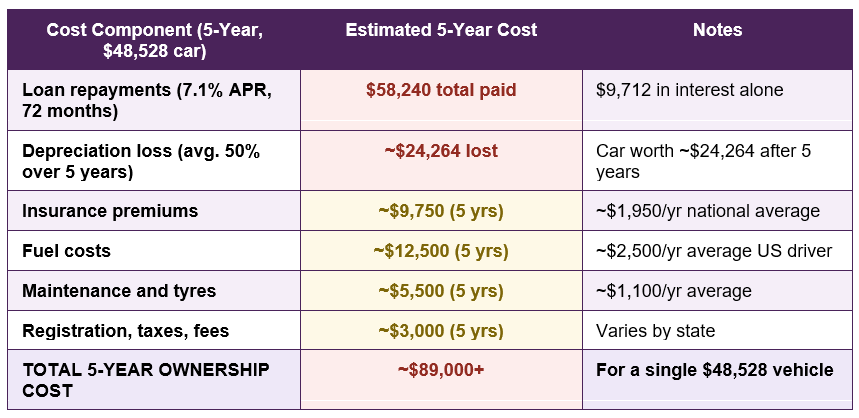

Dealerships and finance companies focus on one number: the monthly payment. If they can fit the vehicle into your monthly budget, the sale is made — regardless of what the total cost of ownership actually looks like. The monthly payment framing is one of the most effective wealth-extraction strategies in consumer finance, because it systematically obscures the true financial burden of the purchase.The table below builds the complete five-year ownership picture for an average-priced new car in the United States:

The monthly payment game: A $48,528 car financed over 72 months at 7.1% APR carries a payment of approximately $810/month. This feels like a manageable $27 per day. But the true five-year cost — including depreciation loss, interest, insurance, fuel, and maintenance — approaches $89,000. The car costs nearly twice its sticker price when all costs are totalled over the ownership period.

Depreciation is the largest single cost in this picture — and the most invisible. A new car loses between 15% and 25% of its value in its first year alone, and approximately 50% of its value over five years. For a $48,528 vehicle, that represents $24,264 in value that simply evaporates — not through use or damage, but through the simple passage of time and the market's preference for newer models. This depreciation is a guaranteed, irreversible loss from the moment the vehicle is driven off the forecourt.

Year-1 depreciation on average US new car: ~$7,279–$12,132 — a loss that occurs regardless of mileage, condition, or care — simply by owning a new vehicle for 12 months (CarEdge / Edmunds 2024)

The 5 Financial Mistakes Drivers Keep Making With Cars

Understanding the cost landscape is one thing. Understanding the specific behavioural patterns that lead drivers into financial difficulty is another. The following five mistakes are consistently identified by financial advisers as the most damaging and most common errors in car purchasing and financing.Mistake 1: Buying More Car Than They Can Afford

The classic rule of thumb in personal finance is that your total car expenses — loan repayment, insurance, and fuel — should not exceed 15-20% of your take-home monthly income. By that measure, a person earning $4,000 per month take-home should spend no more than $600-800 per month on all car-related costs. Yet the average US car payment alone is $738 per month — before insurance, fuel, or maintenance. Millions of drivers are already at or beyond their recommended limit on the loan payment alone.The driver of this behaviour is aspirational purchasing enabled by easy credit. The question asked is not 'What car can I afford?' but 'What monthly payment can I stretch to?' Dealer financing offices are expert at expanding the perception of affordability by extending loan terms — from 48 months to 60, 72, or even 84 months — to bring the monthly number into a range that feels manageable, regardless of the total cost it represents.

84-month car loans: Growing rapidly — loans of 7 years or more now represent over 30% of new car financing in the US — locking buyers into negative equity for the majority of the loan term (Experian 2024)

Mistake 2: Rolling Negative Equity Into a New Loan

Approximately one in three US auto loan holders is currently underwater — meaning they owe more on their car than it is worth. This negative equity position is a direct result of high prices, long loan terms, and rapid early depreciation. The problem compounds dramatically when the underwater buyer wants a new car: many dealers offer to roll the outstanding negative equity from the old loan into the new loan, burying the deficit in a fresh, larger debt.A driver who is $5,000 underwater on their current vehicle and rolls that into a new $45,000 purchase is immediately financing a $50,000 obligation against a $45,000 asset. Depreciation then erodes the new vehicle's value faster than the extended loan pays down the principal, creating a cycle of perpetual negative equity that can persist across multiple vehicle purchases — trapping the driver in car debt for years or decades.

The negative equity spiral: $5,000 rolled into a new loan at 8% APR over 72 months adds $1,270 in pure interest to the existing loss. The driver pays $6,270 in total for a car they no longer own, on top of the payments for the new vehicle. This cycle, repeated across two or three car purchases, represents tens of thousands of dollars in compounding financial damage.

Mistake 3: Fixating on Monthly Payment Instead of Total Cost

The monthly payment is the car industry's most powerful sales tool — and the consumer's worst guide to affordability. Extending a loan from 48 to 72 months on a $40,000 vehicle at 7% APR reduces the monthly payment from $954 to $668 — a saving that feels significant. But the total interest paid over the loan term increases from $5,789 to $8,089 — a difference of $2,300 for the privilege of a lower monthly bill.More critically, the 72-month loan keeps the buyer in negative equity for much longer — the vehicle's value depreciates faster than the loan pays down in the first several years of an extended term, meaning the buyer cannot sell or trade the car without crystallising a loss throughout most of the loan's life. The perceived affordability of the lower monthly payment masks the true cost and locks the buyer into a longer period of financial exposure.

Mistake 4: Ignoring the Full Cost of Insurance

Insurance is the cost category most consistently underestimated by car buyers. The average annual car insurance premium in the United States has surged to over $2,300 in 2024 — a 26% increase in just two years driven by rising repair costs, higher vehicle values, and increased claims frequency. For younger drivers, urban dwellers, or those with imperfect driving records, annual premiums of $3,000-$5,000 or more are not uncommon.New and near-new vehicles financed through a lender require comprehensive and collision coverage — the most expensive tiers of insurance — for the life of the loan. Buyers who calculate affordability based on loan payment alone, without factoring in the mandatory insurance premium, frequently find their total monthly car cost exceeds 30-40% of take-home pay after the purchase is made.

Average US car insurance premium (2024): $2,314/year — a 26% increase in two years driven by surging repair costs, higher vehicle values, and more expensive claim settlements (Bankrate / Insurance.com 2024)

Mistake 5: Treating a Car as an Investment or Status Asset

Perhaps the most psychologically entrenched mistake is the framing of a car as something more than a depreciating transportation asset. Marketing campaigns, social media culture, and dealership psychology consistently encourage drivers to view their vehicle as an expression of identity, success, and social status — a frame that systematically overrides rational financial decision-making.A car is a rapidly depreciating liability. It loses value from the moment it is purchased, costs money to maintain and insure, and generates no income or return. The capital tied up in an expensive new vehicle — or worse, borrowed and paying interest — is capital that could be building wealth in an investment account. A driver who chooses a $35,000 used vehicle instead of a $55,000 new one and invests the $20,000 difference in an S&P 500 index fund at a 10% average return will accumulate over $32,000 in five years from that single decision alone.

The UK Picture: PCP Finance and the Hidden Balloon Payment Trap

In the United Kingdom, the dominant form of car finance is the Personal Contract Purchase (PCP) — a product that has been described by the Financial Conduct Authority as presenting significant risk of consumer harm. PCP agreements involve lower monthly payments than a standard hire purchase loan, achieved by deferring a large 'balloon payment' to the end of the contract — representing the car's residual value after the agreed term.The FCA's 2024 review of motor finance found widespread evidence that commission arrangements between lenders and dealers had led to millions of UK consumers being charged more for car finance than they should have been — a finding that triggered the largest consumer redress investigation in UK financial services history, with potential compensation running to GBP 16-44 billion according to analyst estimates.

The structural risk of PCP is that drivers can become permanently trapped in a cycle of part-exchanging at the end of each contract, never owning the vehicle and repeatedly resetting into new finance agreements — paying interest continuously without ever building equity in the asset. Analysis by the FCA found that a significant proportion of PCP customers do not understand the balloon payment structure of their agreements, increasing the risk of financial shock at contract end.

UK FCA motor finance investigation: GBP 16–44 billion — estimated potential consumer compensation following the FCA's 2024 review of discretionary commission arrangements in motor finance — one of the largest redress exercises in UK financial history

A Smarter Car Strategy: How to Avoid the Financial Trap

Understanding the problem is the first step. The following principles form the foundation of a car purchasing strategy that does not undermine your financial future:- Apply the 20/4/10 rule: Put down at least 20% as a deposit, finance for no more than 4 years, and ensure total car costs do not exceed 10% of gross monthly income. This rule, endorsed by many financial planners, significantly limits the financial exposure of any vehicle purchase.

- Buy a two-to-four-year-old used vehicle: A vehicle that is two to four years old has already absorbed the steepest depreciation curve, yet typically retains modern safety features, fuel efficiency, and reliability. Buying in this window provides substantially more value per pound or dollar than buying new.

- Pay cash or minimise loan term: If financing is unavoidable, minimise the loan term and maximise the deposit. A shorter term means less interest paid and less time in negative equity. Never extend a loan term simply to reduce the monthly payment.

- Calculate the true monthly cost before committing: Add loan repayment + insurance + average monthly fuel + monthly maintenance provision before deciding if you can afford the vehicle. The number that matters is the total, not the loan payment in isolation.

- Resist lifestyle inflation in vehicles: Each time your income rises, resist the impulse to upgrade your vehicle. The car you can afford to buy is not necessarily the car that will best serve your long-term financial health. The difference between an adequate car and an aspirational one, invested over a decade, can represent hundreds of thousands of dollars in wealth.

Conclusion

Cars have never been more financially dangerous than they are in 2024. Record vehicle prices, high interest rates, extended loan terms, surging insurance premiums, and a cultural pressure to drive aspirationally have combined to create a perfect storm of financial risk for drivers who approach vehicle ownership without clear-eyed awareness of the true costs involved.The five mistakes — buying more than you can afford, rolling negative equity, fixating on monthly payments, ignoring insurance costs, and treating cars as status assets — are not unique to any income level or demographic. They are structural behaviours encouraged by an industry that profits from consumer financial confusion. Recognising them is the first act of financial self-defence.

The smarter path is not about deprivation — it is about intentionality. A reliable, efficient, two-year-old used car purchased below the 20/4/10 threshold, with a short loan term and a comprehensive understanding of total ownership costs, serves every functional purpose of a new vehicle at a fraction of the financial damage. The wealth not spent on depreciating metal is the wealth available to build a financially secure future. In the battle between cars and wealth, the drivers who win are the ones who stop letting their vehicle choice make the decision for them.

Frequently Asked Questions (FAQ)

How much of my income should I spend on a car?

The most commonly cited guideline is the 20/4/10 rule: 20% deposit minimum, no more than 4 years of financing, and total car costs (loan, insurance, fuel) no more than 10% of gross monthly income. More conservative planners suggest keeping all car-related expenses below 15% of take-home pay. At the current average monthly payment of $738 plus insurance and fuel, total car costs for many Americans now exceed 20-25% of take-home income — significantly above what financial health supports.Is it ever worth buying a new car?

A new car can be worth buying in specific circumstances: when manufacturer incentives, cashback offers, or 0% finance deals significantly reduce the effective purchase price; when your budget stretches far enough that the depreciation is not a proportionally large share of your net worth; or when specific reliability concerns about used vehicles in your market make new warranties worth their premium. For most buyers, however, a two-to-four-year-old used vehicle provides the most financial value — absorbing the steepest depreciation curve while retaining most of the practical benefits of a newer car.What is negative equity in a car loan, and how do I avoid it?

Negative equity — sometimes called being 'underwater' — means you owe more on your car loan than the vehicle is currently worth. It is caused by the combination of rapid early depreciation and slow initial loan paydown on extended-term loans. To avoid it: make a significant deposit (20% or more) to start with equity; choose a shorter loan term so principal reduces faster than the vehicle depreciates; and avoid rolling previous negative equity into a new loan, which starts the new agreement in an immediate deficit position.What is the PCP mis-selling scandal in the UK?

The FCA's 2024 investigation into Personal Contract Purchase (PCP) motor finance found widespread evidence that discretionary commission arrangements allowed car dealers to increase the interest rate charged to customers — and earn a higher commission — without the customer's knowledge or informed consent. The regulator found this practice was likely unlawful and triggered a redress review potentially worth GBP 16-44 billion. UK consumers who took out PCP or HP motor finance between 2007 and 2021 through a broker or dealer may be entitled to compensation. The FCA's motor finance review page provides current guidance.What is the opportunity cost of a car purchase?

Opportunity cost is the wealth you forgo by spending money on a depreciating asset instead of an appreciating one. The $20,000 extra spent on a new car instead of a used one, invested in a diversified index fund at a 10% average annual return, would grow to approximately $32,000 in five years, $52,000 in ten years, and $134,000 in twenty years. Applied across the multiple vehicle purchases most drivers make in a lifetime, the cumulative opportunity cost of consistent over-spending on cars can amount to hundreds of thousands of dollars in foregone investment wealth — often representing the difference between a comfortable retirement and a financially constrained one.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Experian — State of the Auto Finance Market Q1 2024

https://www.experian.com/blogs/ask-experian/state-of-the-automotive-finance-market/

2. Kelley Blue Book / Cox Automotive — New Vehicle Price Analysis 2024

https://www.coxautoinc.com/market-insights/

3. Federal Reserve Bank of New York — Household Debt and Credit Q1 2024

https://www.newyorkfed.org/microeconomics/hhdc

4. AAA — Your Driving Costs 2023 Report

https://newsroom.aaa.com/auto/your-driving-costs/

5. Financial Conduct Authority (UK) — Motor Finance Review 2024

https://www.fca.org.uk/consumers/motor-finance

6. Edmunds — True Cost to Own and Depreciation Calculator

https://www.edmunds.com/tco.html

7. Bankrate — Average Car Insurance Rates 2024

https://www.bankrate.com/insurance/car/average-cost-of-car-insurance/

8. Investopedia — The Real Cost of Owning a Car

https://www.investopedia.com/articles/pf/08/cost-of-owning-car.asp

0 Comments Comments