Vehicles & Cars

What Is a Young Driver Car Insurance? Complete Guide

Table of Contents

- Why Young Drivers Pay More — and What to Do About It

- Why Young Driver Insurance Costs So Much: The Statistical Reality

- What Is Young Driver Insurance: The Types of Cover Available

- The Three Levels of Cover

- Telematics (Black Box) Insurance: The Young Driver's Most Powerful Tool

- Young Driver Insurance Costs in 2026: What the Data Shows

- How Black Box Scoring Works: The Seven Monitored Factors

- The Car You Choose Changes Everything: Insurance Groups Explained

- Best Insurance Groups for Young Drivers

- Cars to Avoid as a Young Driver

- Named Drivers, Fronting, and Getting the Policy Right

- Adding a Named Experienced Driver

- Fronting: The Fraud That Invalidates Your Insurance

- Building Your Way to Lower Premiums: The First 3 Years

- Conclusion

- Frequently Asked Questions (FAQ)

- External References

Why Young Drivers Pay More — and What to Do About It

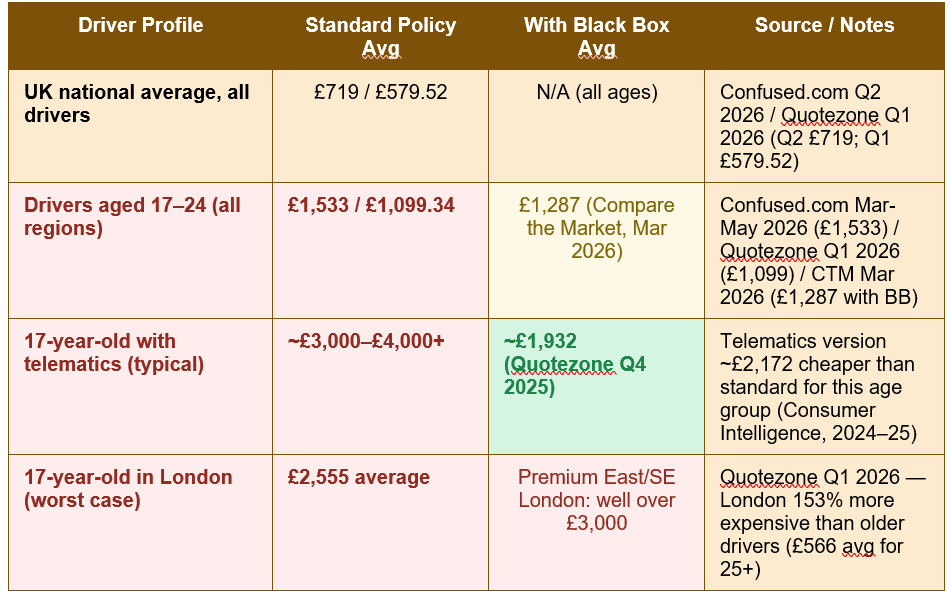

For any driver aged 17 to 24 in the UK, car insurance is very likely the single most expensive part of owning and running a vehicle. In Q2 2026, Confused.com's Price Index — based on more than six million real car insurance quotes — shows the national average annual premium for drivers aged 17 to 24 at £1,533 per year, more than twice the UK national average of £719. In London, 17-year-old drivers face average premiums of £2,555 per year. In some East and South East London postcodes, premiums comfortably exceed £3,000. For a significant number of new drivers, the annual insurance bill genuinely exceeds the purchase price of the car they are insuring.These figures are not arbitrary. They are the direct consequence of a statistical reality that insurers price with precision: Department for Transport data shows that drivers aged 17 to 24 represent just 7% of UK licence holders but are involved in 24% of serious road accidents. Young drivers are six times more likely to be involved in an accident than drivers aged 25 to 35. They are more likely to drive in high-risk conditions — late at night, with passengers of the same age — and less likely to have developed the hazard perception skills that come with years of driving experience. The insurance premium is an accurate actuarial reflection of this risk profile, not a penalty.

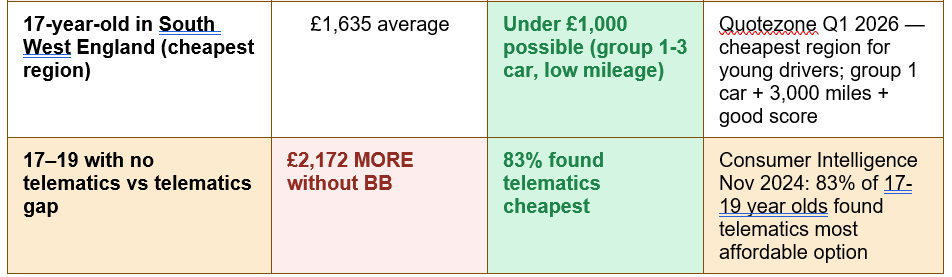

The good news in 2026 is twofold. First, premiums for young drivers are at their lowest level in 10 years — Quotezone's Q1 2026 data from 100,000+ policies shows the 17-24 bracket averaging £1,099.34, down significantly from their 2023-2024 peak. Second, the tools available to reduce that premium have never been more powerful: telematics (black box) insurance can reduce a 17-year-old's premium by an average of £2,172 compared to a standard policy for the same driver, according to Consumer Intelligence research. This guide explains how young driver insurance works, what determines the price, how black box insurance changes the equation, what cars to buy and avoid, and every legitimate strategy for reducing the cost as quickly as possible.

Why Young Driver Insurance Costs So Much: The Statistical Reality

Car insurance pricing is actuarial at its core — premiums are calculated by estimating the probability that a driver will make a claim and the likely cost of that claim. Every factor that correlates with higher accident likelihood or higher claim cost pushes the premium up. For young drivers, multiple high-risk factors cluster simultaneously:- Age and inexperience: The first 12 to 18 months of driving are consistently the highest-risk period. New drivers have not yet developed the hazard perception, situational awareness, and risk assessment skills that experienced drivers apply automatically. This inexperience is the primary driver of the young driver premium.

- Behavioural risk factors: Department for Transport data shows that 'loss of control', 'exceeding the speed limit', and 'careless driving' are significantly more likely to be recorded in collisions involving young drivers compared with other age groups. Driving with passengers of the same age increases risk further — each additional young passenger statistically increases accident likelihood.

- Time of day: Young drivers are more likely to drive late at night and at weekends — periods that carry higher accident rates for all drivers and significantly higher rates for inexperienced ones. Late-night weekend driving represents the highest statistical risk period on UK roads.

- Vehicle choice: Young drivers often gravitate toward modified cars, performance variants, or older premium-badged vehicles that happen to fall into high insurance groups — choices that substantially increase the premium independently of the driver's age.

The risk data that drives the price: 17-24 year olds are 7% of UK licence holders but involved in 24% of serious accidents — Department for Transport data on reported road casualties in Great Britain — this statistical concentration of accident involvement is the direct actuarial basis for young driver premiums and is not expected to change significantly in the medium term (DfT / Brumble, 2026).

What Is Young Driver Insurance: The Types of Cover Available

Young driver insurance is not a legally distinct category of car insurance — it refers to standard UK car insurance (comprehensive, third-party fire and theft, or third-party only) sold to drivers in the highest-premium demographic, typically aged 17 to 25. The product types available are the same as for any UK driver, but the pricing, the availability of specific products, and the strategies that reduce cost differ significantly from the market for experienced drivers.The Three Levels of Cover

- Comprehensive: The highest level of cover — pays for damage to your own vehicle as well as third-party vehicles, property, and persons. Despite being the most protective policy, it is frequently the same price or even cheaper than third-party options for young drivers. Insurers view drivers who choose comprehensive cover as statistically lower risk, which can offset the higher level of cover. Always get a comprehensive quote before assuming TPFT or TPO will be cheaper.

- Third-Party Fire and Theft (TPFT): Covers damage to third parties and your vehicle if stolen or damaged by fire, but not damage to your own vehicle in an accident where you are at fault. Not always cheaper than comprehensive for young drivers.

- Third-Party Only (TPO): The legal minimum — covers damage and injury to others but nothing for your own vehicle or its theft. Despite providing the least protection, TPO is sometimes priced higher than comprehensive for young drivers because the profile of drivers who choose minimum cover is statistically higher risk. Always compare all three levels.

Telematics (Black Box) Insurance: The Young Driver's Most Powerful Tool

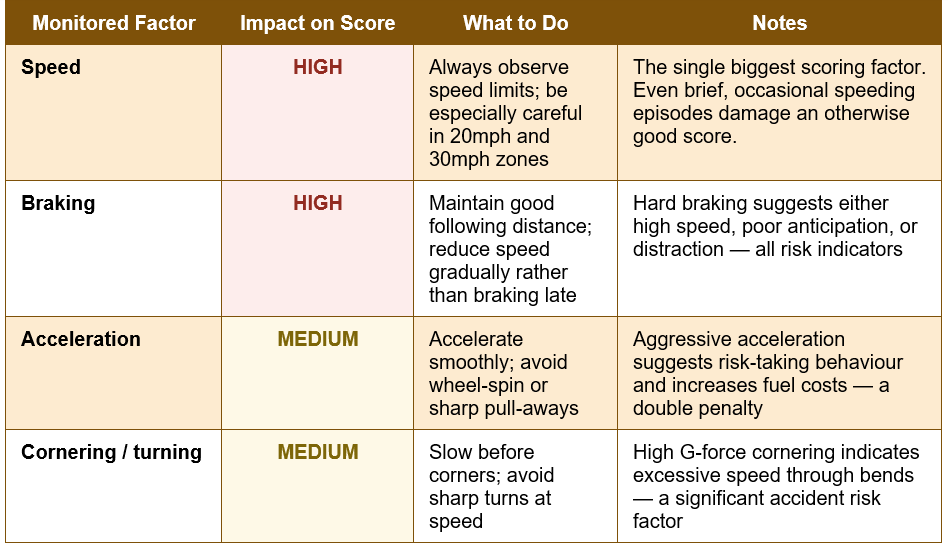

Telematics insurance — commonly called black box insurance — is the most important and most impactful product available to young UK drivers in 2026. Rather than pricing your premium purely on actuarial group statistics (age, postcode, car type), a telematics policy measures how you actually drive and prices you on your individual behaviour. This single innovation has the potential to reduce a young driver's premium by thousands of pounds compared to a standard policy for the same driver and car.The device itself is either a small electronic unit fitted to your car by an engineer, a plug-in OBD dongle that clips into your car's diagnostic port, or — increasingly in 2026 — a smartphone app that uses your phone's GPS and motion sensors to collect the same data without any hardware. The data collected typically includes speed (compared to speed limits on the road you are travelling), braking force and frequency, acceleration patterns, cornering forces, time of day, mileage, and in some app-based policies, phone use while driving.

Young Driver Insurance Costs in 2026: What the Data Shows

The table below consolidates premium data from the UK's major insurance data providers for 2026, comparing standard and telematics premiums across key driver profiles:

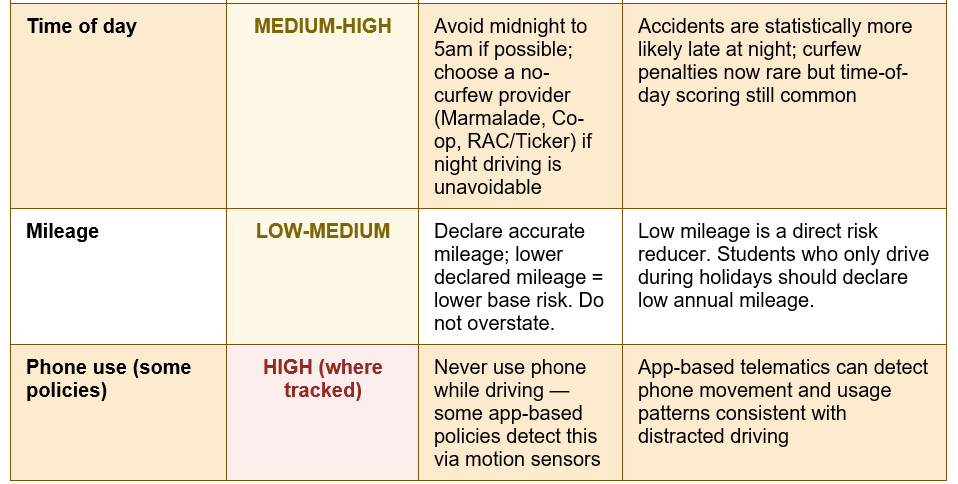

How Black Box Scoring Works: The Seven Monitored Factors

Understanding exactly how your driving score is calculated is the foundation of getting the maximum benefit from a telematics policy. The following table maps each monitored factor to its impact level and what you should do:

The curfew question in 2026: Many older guides describe black box policies as having strict curfews — typically midnight to 6am — with automatic policy cancellation or penalty charges for driving during these hours. In 2026, strict curfews have become much less common. Several providers — including Marmalade, Co-op, and RAC/Ticker — have no night-time curfew at all, though late-night driving still affects the time-of-day component of your driving score. If your job, studies, or lifestyle regularly require driving after midnight, specifically look for a no-curfew provider and verify the current terms before purchasing.

The Car You Choose Changes Everything: Insurance Groups Explained

The decision about which car to buy is the most consequential long-term financial decision any young driver makes — not just because of the purchase price, but because the insurance group of the car is fixed at manufacture and determines a significant portion of the insurance premium for every policy the driver holds for as long as they own that car. The difference between a Group 1 car and a Group 20 car in annual premium for a 19-year-old driver can be £1,000 to £2,000 per year. Over three years — the typical period before a young driver's age-based premium begins to fall materially — this represents a difference that can exceed the total purchase price of either car.UK cars are currently rated under two systems in 2026. Cars registered before August 2024 use the traditional 1-50 scale, where Group 1 is cheapest and Group 50 most expensive. Cars registered from August 2024 onward use the new Vehicle Risk Rating (VRR) system on a 1-99 scale, introduced by Thatcham Research and the Association of British Insurers for greater pricing granularity. As an 18-month transition is still in effect through most of 2026, most insurers use both systems. Check any car's group before buying at the Thatcham Research online checker.

Best Insurance Groups for Young Drivers

- Groups 1-5 — Ideal: City cars and small hatchbacks with 1.0-litre engines. Examples include the Vauxhall Corsa 1.0, Volkswagen Polo 1.0, Hyundai i10, Kia Picanto, and Fiat Panda. Typically under £1,000-£1,500 per year for a careful young driver with telematics.

- Groups 6-10 — Good: Larger superminis and entry-level family hatches. Still affordable for young drivers who shop around and consider telematics.

- Groups 11-20 — Manageable with caution: Premiums increase meaningfully in this range for under-25s. Some vehicles in this range are acceptable with telematics and a very clean location profile.

Cars to Avoid as a Young Driver

Several categories of car are consistently and dramatically expensive to insure for young drivers regardless of telematics discounts or driving history. Performance variants — Fiesta ST, Polo GTI, Corsa VXR, Clio RS — sit in groups 30 or above and attract premiums that frequently exceed £4,000 per year for under-25s. Modified cars of any description must be declared to your insurer and always increase premiums — even cosmetic modifications like alloy wheel upgrades, body kits, or tinted windows. Older premium-badged cars such as older BMW 3 Series, Audi A3, or Mercedes C-Class models may appear affordable to buy but typically sit in groups 20 to 30, where young driver premiums can reach £3,000 to £4,000 per year. Electric vehicles, while cheaper to run, sit in consistently higher insurance groups than equivalent petrol cars due to battery replacement costs and specialist repair requirements.Named Drivers, Fronting, and Getting the Policy Right

Adding a Named Experienced Driver

Adding a parent, older sibling, or other experienced driver with a clean licence as a named driver on your policy can reduce your premium. This works because the insurer views the overall risk pool of the policy — which now includes an experienced low-risk driver — as less concentrated on the highest-risk profile. The savings are typically most pronounced when the named driver has a significant no-claims bonus and an unblemished licence. To qualify, the named driver must genuinely use the car occasionally — they do not need to be the main driver, but they must have real, genuine access to the vehicle.Fronting: The Fraud That Invalidates Your Insurance

Fronting is the practice of listing a parent or more experienced driver as the primary policyholder (the main driver) when the young driver is actually the main user of the vehicle, in order to access the lower premiums associated with the experienced driver's profile. It is insurance fraud. It is illegal. And it is actively detected by insurers through data analysis and the investigation of claims. If you have a claim and the insurer determines that the declared main driver was not the genuine main driver, the claim will be voided — regardless of who caused the accident or how serious the injuries. The young driver is left with no cover, potentially a fraud record, and no no-claims bonus. The short-term premium saving is catastrophically not worth the risk.The correct approach: the young driver who primarily uses the vehicle must be the named policyholder. If a parent also genuinely uses the car, they can be added as a named driver — in the reverse order of fronting, and entirely legitimate.

ACTION POINT: Before buying a car, check its insurance group at check.thatcham.org (free) and get three insurance quotes — including at least one telematics quote — before committing to the purchase. A car that looks affordable to buy may cost £2,000+ more per year to insure than a lower-group alternative.

Building Your Way to Lower Premiums: The First 3 Years

Young driver premiums are not permanent — they improve materially as you accumulate driving experience and build your no-claims discount (NCD). Understanding the timeline helps set realistic expectations and plan the right insurance strategy for each stage:- Year 1 — Maximise telematics, minimise the car: Your first year is the highest-risk period and typically produces the highest premium. Use a telematics policy without exception if you are under 22. Choose the lowest-group car you can afford. Keep mileage low and accurate. Drive during the day whenever possible. Build a clean driving record.

- Year 2 — First renewal, real savings visible: After a full year of telematics data and one year of no-claims bonus, your renewal quote should show meaningful reduction if your driving score was consistently good. Compare the renewal offer against the market — do not auto-renew. Consider whether telematics remains the cheaper option for year two or whether a standard policy has become competitive.

- Years 3 to 5 — NCD compounds, age premium falls: Each additional claim-free year adds to your NCD. Five years of no claims typically delivers 60-70% off the base premium. By age 23-25, the age-based component of the premium begins to fall significantly. Most young drivers who survive their first three years without an at-fault claim find their premiums dropping rapidly toward the national average by age 24-25.

- Beyond year 5 — Protect what you have built: Once you have accumulated 4 or more years of NCD, consider purchasing NCD protection as an add-on. This allows you to make one claim without losing your discount — typically costing £20 to £50 per year and worth every penny after years of careful building.

Conclusion

Young driver car insurance in the UK in 2026 is expensive, structured, and navigable — in that order. It is expensive because the statistical evidence for the higher risk profile of 17 to 24 year old drivers is robust and well-documented: they represent 7% of licence holders but 24% of serious accidents. It is structured because the factors that determine the premium are specific, quantifiable, and addressable: the car's insurance group, the policy type, the presence or absence of telematics, the mileage declared, the security of overnight parking, and the accumulated no-claims discount. And it is navigable because drivers who understand these factors and make deliberate decisions around them can achieve premiums far below what the raw age bracket would otherwise suggest.The single most impactful decision for a young driver in 2026 is choosing a telematics policy. Consumer Intelligence research confirms that 83% of 17 to 19 year olds found telematics their most affordable option, with an average saving of £2,172 compared to a standard policy for the same driver. In London, where young driver premiums are highest, the saving can be even greater. The second most impactful decision is the car: checking the insurance group before purchase, at the Thatcham Research online tool, and choosing a Group 1 to 5 vehicle over any performance, modified, or older premium-badged alternative is the highest-return five-minute action available to any young driver before they buy.

The combination of a telematics policy, a low-group car, a realistic mileage declaration, an experienced named driver who genuinely uses the vehicle, and consistent safe driving behaviour can bring a young driver's premium down to under £1,000 per year in lower-cost regions — and produces a driving record that feeds directly into lower standard-policy premiums as the driver ages through the risk bracket and builds their no-claims discount. Every year of safe driving is an investment, and it compounds.

Frequently Asked Questions (FAQ)

How much does car insurance cost for a 17-year-old in the UK in 2026?

Average premiums for 17-year-old drivers vary significantly by location and policy type. Quotezone's Q1 2026 data (100,000+ real policies) shows the 17-24 bracket averaging £1,099.34 overall. Confused.com's March-May 2026 data shows the same bracket at £1,533. 17-year-olds specifically typically pay between £1,800 and £3,000 on a standard policy, with London averages reaching £2,555. With a telematics policy, a 17-year-old in a Group 1-3 car outside London can achieve premiums under £1,000 — and Compare the Market's March 2026 data shows 17-24 year olds with black box paying £1,287 on average versus £1,533 without. The exact figure depends on your postcode, car, declared mileage, and driving score.What is black box insurance and how does it work?

Black box insurance (also called telematics insurance) is a type of UK car insurance that monitors how you drive using a device fitted to your car, a plug-in OBD dongle, or a smartphone app. The device or app tracks your speed, braking, acceleration, cornering, time of day, and mileage. Your insurer uses this data to assess your risk profile individually rather than relying purely on age and postcode statistics. Safe, careful drivers receive lower premiums at renewal or mid-policy discounts. Consistently poor scores result in higher renewal quotes. Consumer Intelligence research from late 2024 found that 83% of drivers aged 17-19 found telematics their most affordable option, with a median saving of £2,172 compared to standard policies for the same profile.What is fronting and why is it illegal?

Fronting is the practice of listing a more experienced driver (typically a parent) as the main policyholder when the young driver is actually the primary user of the vehicle, in order to access the lower premiums associated with the experienced driver's profile. It is a form of insurance fraud under UK law. If a claim is made and the insurer's investigation reveals that the declared main driver was not the genuine main driver, the claim can be voided entirely, leaving the young driver with no cover and potentially criminal liability. The legitimate version — adding an experienced driver as a named driver who genuinely uses the car occasionally, with the young driver correctly listed as the main driver — is entirely legal and can legitimately reduce premiums.Which cars are cheapest to insure for young drivers?

Cars in insurance Groups 1-5 are the cheapest to insure for young drivers in 2026. These are typically small city cars and hatchbacks with 1.0-litre engines — examples include the Vauxhall Corsa 1.0, Volkswagen Polo 1.0, Hyundai i10, Kia Picanto, and Fiat Panda. The difference in annual premium between a Group 1 and a Group 20 car for a 19-year-old can be £1,000 to £2,000 per year. Cars to avoid include performance variants (Fiesta ST, Polo GTI), modified cars of any description, older premium-badged cars (BMW 3 Series, Audi A3), and electric vehicles (consistently in higher groups due to battery costs). Check any car's insurance group free at check.thatcham.org before buying.Does comprehensive insurance cost more than third-party for young drivers?

Not necessarily — and this surprises many young drivers. Comprehensive car insurance is frequently the same price or even cheaper than third-party only (TPO) or third-party fire and theft (TPFT) for young drivers. The reason is that insurers statistically view drivers who choose comprehensive cover as lower risk than those who choose minimum cover — the type of driver who opts for comprehensive tends to be more responsible and safety-conscious overall. Always request quotes for all three levels of cover when comparing. Never assume that less cover means a lower cost — for young drivers, the assumption is often wrong, and choosing TPO or TPFT to save money can leave you paying the same or more for significantly worse protection.External References

The following authoritative sources were used in researching this article and are recommended for further reading:1. Confused.com — Q2 2026 Car Insurance Price Index including 17–24 age group data

https://www.confused.com/compare-car-insurance/average-car-insurance-cost-uk

2. Quotezone — Average UK Car Insurance by Age and Region (Q1 2026, 100k+ policies)

https://www.quotezone.co.uk/car-insurance/average-car-insurance-premium-by-region

3. Brumble — Young Drivers Car Insurance UK: How to Get Cheaper Cover in 2026 (May 2026)

https://brumble.co.uk/guides/young-drivers-insurance

4. Brumble — Black Box Car Insurance: How Telematics Works and Is It Worth It? (May 2026)

https://brumble.co.uk/guides/black-box-car-insurance

5. Carsa — Cheapest Cars to Insure for New Drivers UK 2026 (July 2026)

https://www.carsa.co.uk/blog/cheapest-cars-insure-new-drivers-uk-2026

6. TrustMyPolicy — Black Box Insurance Young Drivers UK: 5 Best Picks 2026 (April 2026)

https://trustmypolicy.com/best-black-box-insurance-for-young-drivers-uk/

7. Thatcham Research — Vehicle Insurance Group Check (Official ABI/Thatcham Tool)

https://www.thatcham.org/abi-group-rating-check/

8. Department for Transport — Reported Road Casualties Great Britain (Young Driver Statistics)

https://www.gov.uk/government/collections/road-accidents-and-safety-statistics

0 Comments Comments